Fillable Printable Eligibility Information Required For Sbaexpress Submission

Fillable Printable Eligibility Information Required For Sbaexpress Submission

Eligibility Information Required For Sbaexpress Submission

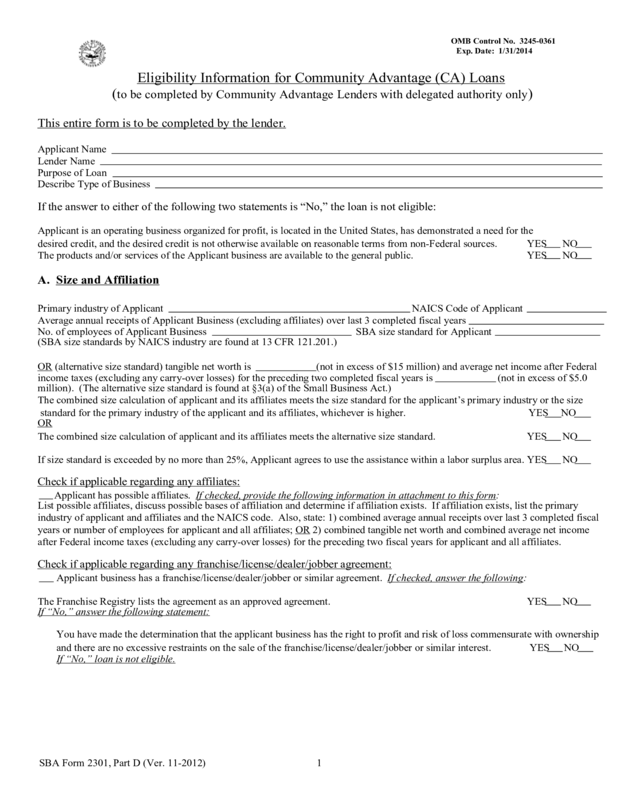

OMB Control No. 3245-0361

Exp. Date: 1/31/2014

Eligibility Information for Community Advantage (CA) Loans

(to be completed by Community Advantage Lenders with delegated authority only)

This entire form is to be completed by the lender.

Applicant Name

Lender Name

Purpose of Loan

Describe Type of Business

If the answer to either of the following two statements is “No,” the loan is not eligible:

Applicant is an operating business organized for profit, is located in the United States, has demonstrated a need for the

desired credit, and the desired credit is not otherwise available on reasonable terms from non-Federal sources.YESNO

The products and/or services of the Applicant business are available to the general public.YESNO

A. Size and Affiliation

Primary industry of ApplicantNAICS Code of Applicant

Average annual receipts of Applicant Business (excluding affiliates) over last 3 completed fiscal years

No. of employees of Applicant Business SBA size standard for Applicant

(SBA size standards by NAICS industry are found at 13 CFR 121.201.)

OR (alternative size standard) tangible net worth is (not in excess of $15 million) and average net income after Federal

income taxes (excluding any carry-over losses) for the preceding two completed fiscal years is (not in excess of $5.0

million). (The alternative size standard is found at §3(a) of the Small Business Act.)

The combined size calculation of applicant and its affiliates meets the size standard for the applicant’s primary industry or the size

standard for the primary industry of the applicant and its affiliates, whichever is higher. YESNO

OR

The combined size calculation of applicant and its affiliates meets the alternative size standard.YESNO

If size standard is exceeded by no more than 25%, Applicant agrees to use the assistance within a labor surplus area. YESNO

Check if applicable regarding any affiliates:

Applicant has possible affiliates. If checked, provide the following information in attachment to this form:

List possible affiliates, discuss possible bases of affiliation and determine if affiliation exists. If affiliation exists, list the primary

industry of applicant and affiliates and the NAICS code. Also, state: 1) combined average annual receipts over last 3 completed fiscal

years or number of employees for applicant and all affiliates; OR 2) combined tangible net worth and combined average net income

after Federal income taxes (excluding any carry-over losses) for the preceding two fiscal years for applicant and all affiliates.

Check if applicable regarding any franchise/license/dealer/jobber agreement:

Applicant business has a franchise/license/dealer/jobber or similar agreement. If checked, answer the following:

The Franchise Registry lists the agreement as an approved agreement. YESNO

If “No,” answer the following statement:

You have made the determination that the applicant business has the right to profit and risk of loss commensurate with ownership

and there are no excessive restraints on the sale of the franchise/license/dealer/jobber or similar interest. YESNO

If “No,” loan is not eligible.

SBA Form 2301, Part D (Ver. 11-2012) 1

B. Principals of the Applicant

Lender has assessed the liquid assets of the immediate family (including spouse and dependent children) of each owner of 20% or

more of the equity of the Applicant (and of the Operating Company, if the Applicant is an Eligible Passive Company) and determined

that they do not exceed:

•for a financing package of $250,000 or less, two times the total financing package or $100,000, whichever is greater;

•for a financing package between $250,001 and $500,000, one and one-half times the total financing package or $500,000,

whichever is greater;

•for a financing package of more than $500,000, one times the total financing package or $750,000, whichever

is greater. YESNO

No Associate (an officer, director, owner of more than 20 percent of the equity, or key employee) of the Applicant is

incarcerated, on probation, on parole, or under indictment for a felony or a crime of moral turpitude.YESNO

All owners of 20 percent or more of the Applicant (including a spouse owning 5 percent or more when the combined ownership of

both spouses is 20 percent or more) will guarantee the loan (except for ESOPs or eligible 401(k) Trusts).

YESNO

All Associates of the business are either U.S. citizens or non-U.S. citizens whose status is being verified with USCIS or SBA. For

non-U.S. citizens, the lender has obtained a copy of the individual’s USCIS documentation and submitted a USCIS Form G-845,

“Document Verification Request” with supporting information to USCIS or SBA. In addition, the lender will not close and disburse

the loan prior to receiving confirmation from USCIS or SBA that the alien status of all Associates

meets SBA’s policies. YESNO

If “Yes,” CHOOSE the ONE that applies (If neither applies, the loan is not eligible):

The business is at least 51 percent owned by individuals who are U.S. citizens and/or who have Lawful

Permanent Resident (LPR) status, which lender will verify with the USCIS or SBA prior to first disbursement,

and control the management and daily operations of the business; OR

The business is at least 51 percent owned by aliens with an alien status other than LPR, which lender will

verify with the USCIS or SBA prior to first disbursement, the lender has determined that continual and consistent

management of the business has been provided by a U.S. citizen or by an LPR (which lender will verify with the

USCIS or SBA prior to first disbursement) for at least one year and will continue indefinitely AND U.S. collateral

is pledged sufficient to pay the loan in full at any time. (Businesses less than one year old do not meet these

requirements.)

C. Terms of the Loan

Loan request is for a 7(a) term loan of $250,000 or less. YESNO

The maturity of the loan does not exceed the maximum allowable by SBA for the use of proceeds and is the

shortest appropriate term commensurate with repayment ability of the Applicant. YESNO

SBA guaranty percentage for this loan does not exceed 85% for loans of $150,000 or less and does not exceed 75% for loans greater

than $150,000.

YESNO

The aggregate SBA guaranteed portions for this application and all outstanding 7(a) and 504 loans to Applicant and its affiliates does

not exceed $3.75 million.

YESNO

NOYESThe interest rate of the loan does not exceed the maximum amount allowable by SBA.

Applicant does not have a non-SBA-guaranteed loan made by any lender at or about the same time for a similar

purpose as this CA loan, with a lien position on collateral senior to this CA loan (“Preference”). YESNO

D. Type of Business

Applicant is or does one of the following: If checked, loan is not eligible.

•primarily engaged in the business of lending

•a passive business owned by developers or landlords that do not actively use or occupy the assets acquired or improved

with the loan proceeds and that is not an Eligible Passive Company discussed below

•bail bond company

SBA Form 2301, Part D (Ver. 11-2012) 2

•life insurance company

•located in a foreign country or owned by undocumented (illegal) aliens

•pyramid sale distribution plan

•any illegal activity

•principally engaged in teaching, instructing, counseling or indoctrinating religion or religious beliefs, whether in a

religious or secular setting.

•consumer or marketing cooperative

•earns 1/3 or more of its gross annual revenue from packaging SBA loans

•derives directly or indirectly more than 5% of its gross revenue through the sale of products or services, or the presentation

of any depiction or displays, of a prurient sexual nature or that presents any live performances of a prurient nature

•primarily engaged in political or lobbying activities

•a speculative business (such as oil wildcatting, mining and research & development)

Applicant is a pawn shop. If checked, answer the following question. If “No” loan is not eligible.

More than 50% of Applicant’s income for the previous year was from the sale of merchandise

rather than from interest on loans. YESNO

Applicant is a mortgage service company. If checked, answer the following question. If “No” loan is not eligible.

Any mortgage loans funded are sold within 14 days of loan closing. YESNO

Applicant is a business that is primarily engaged in subdividing real property into lots and developing it for resale on its own

account or in owning or purchasing real estate and leasing it for any purpose. If checked, loan is not eligible.

Applicant is a hotel, motel, recreational vehicle park, campground, marina or similar type of business. If checked, answer the

following question.

If “No” loan is not eligible.

Applicant derives 50 percent or more of its gross annual income from transients who stay for periods of

time not exceeding 30 days.YESNO

Any of gross annual revenue of Applicant business is derived from gambling. If checked, answer the

following question. If “No” loan is not eligible.

The revenue is from legal gambling activities and comprises 1/3 or less of gross annual revenue of

Applicant business and the business is not a racetrack, casino or otherwise have gambling as its

reason for being.YESNO

Applicant is a private club or business. If checked, answer the following question. If “No” loan is not eligible.

Business does not limit the number of memberships for reasons other than capacity.YESNO

Applicant is a government-owned entity. If checked, answer the following question. If “No” loan is not eligible.

Applicant is business owned or controlled by a Native American tribe, but is a separate legal

entity from the tribe.YESNO

Applicant is an Eligible Passive Company (EPC). If checked, fill in the blanks and answer the following questions. If “No” loan

is not eligible. Attach additional sheet with Names and Legal Forms if more than one OC. References below to OC mean each

OC.

Name of Operating Company (OC):

Legal Form of Entity of OC:

•The EPC will use the loan proceeds to acquire or lease, and /or improve or renovate real or personal

property (including eligible refinancing) that it leases 100% to one or more OCs.YESNO

•The OC is an eligible small business and the proposed use of proceeds would be an eligible use if the OC

were obtaining the financing directly.YESNO

•The EPC (with the exception of a trust) and the OC each are small under SBA's size standards.

YESNO

•The EPC is eligible as to type of business, other than being passive.

YESNO

•The lease between the Eligible Passive Company and the Operating Company will be in writing,

will have a remaining term at least equal to the term of the loan (including options to renew exercisable solely by the

Operating Company), will be subordinated to SBA’s lien on the property and the rents will be assigned as

collateral for the loan.YESNO

SBA Form 2301, Part D (Ver. 11-2012) 3

•The OC will be a guarantor or co-borrower. If loan proceeds include working capital or assets

to be owned by the OC, it will be a co-borrower.YESNO

•Each 20% or more owner of the EPC and each 20% or more owner of the OC will guarantee the loan.

YESNO

•The aggregate amount of the SBA portions for this application and for all outstanding loans to

the EPC, the OC, and their affiliates does not exceed $3.75 million.YESNO

•Neither the EPC nor the OC is a trust or SBA requirements regarding trusts are met.

YESNO

E. Use of Proceeds

To provide or refinance funds used for payments, distributions, or loans to Associates of the Applicant.

If checked, loan is not eligible.

For a purpose that will not benefit the small business. If checked, loan is not eligible.

To provide funds for floor plan financing. If checked, loan is not eligible

For debt refinancing. If checked, ATTACH A DEBT SCHEDULE TO THE CHECKLIST SHOWING THE TERMS OF THE

DEBT TO BE REFINANCED AND THE JUSTIFICATION FOR THE REFINANCING AND INCLUDE IN THE LOAN FILE.

Also, answer the following questions. If the answer is “No,” loan is not eligible.

•SBA loan proceeds will not be used to refinance debt originally used to finance a loan purpose that would have been

ineligible for SBA financing at the time it was originally made.YESNO

•Refinancing will provide a substantial benefit to Applicant of at least 10% needed improvement to cash flow.

If more than one debt is refinanced, the new debt will have at least a 10% cash flow improvement over the combined cash

flow of the debt being refinanced. (This does not apply if the refinanced debt is a demand note,

involves a balloon payment, credit card obligation used for business related purposes, or revolving line of credit [short

term or long term] .) YESNO

•Existing debt is one of the types of debt that may be refinanced with an SBA loan.

YESNO

•Existing debt no longer meets the needs of the Applicant.

YESNO

•Debt to be refinanced is NOT a same institution debt between the Applicant and the

requesting SBA lender.YESNO

•Debt to be refinanced is either 1) a non-SBA-guaranteed loan or 2) an SBA-guaranteed loan with another lender and

meets the requirements for refinancing an SBA-guaranteed debt through delegated processing set forth in SOP 50 10 5,

Subpart B, Chapter 2.YESNO

•Proceeds will not pay a creditor in a position to sustain a loss causing a shift to SBA of all or part of a potential loss from

an existing debt.YESNO

•Loan will not refund debt to an SBIC.

YESNO

•Loan will not repay third party financing for any existing 504 project.

YESNO

•Loan will not repay delinquent IRS withholding taxes, sales taxes or similar funds held in trust.

YESNO

To refinance seller take-back financing. If checked, answer the following questions. If “No,” loan is not eligible.

•The seller take-back financing is not less than 24 months following a change of ownership and the seller take-back

financing is and has been current for the past 24 months.

•A new business valuation has been obtained OR the existing business valuation meets the requirements of SOP 50 10 5,

Subpart B, Chapter 4.YESNO

To fund or refinance a change of ownership. If checked, answer the following questions. If “No,” loan is not eligible.

•The change will promote the sound development or preserve the existence of the Applicant business.

YESNO

•Change is 100% of ownership or a business repurchasing 100% of one or more of its owners'

interests.YESNO

•The loan proceeds will not pay off an SBA-guaranteed loan of the seller with the same lender

YESNO

CHOOSE ONE – Business Valuation Requirements

The amount being financed (including any 7(a), 504, seller, or other financing) minus the appraised value of real estate

and/or equipment being financed is $250,000 or less. The valuation of the business is supported by at least a lender's valuation.

If the valuation analysis is performed by the lender's loan officer, a synopsis is attached.

NOYES

SBA Form 2301, Part D (Ver. 11-2012) 4

The amount being financed (including any 7(a), 504, seller or other financing) minus the appraised value of real estate

and/or equipment is more than $250,000 OR there is a close relationship between the buyer and the seller. The lender has

obtained an independent business valuation from a qualified source.

The Community Advantage lender is an SBA Microlender and the SBA Microlender is using its SBA intermediary loan to fund

the Community Advantage loan. If checked, loan is not eligible.

The Community Advantage loan will refinance a loan made by or guaranteed by the Department of Agriculture. If checked, loan

is not eligible.

F. Special Program Requirements

Loan is a Community Advantage loan and the small business applicant falls into one of the following categories

(at leastone category must be checked):

Located in a Low-to-Moderate Income (LMI) Community

Located in an Empowerment Zone or Enterprise Community

Located in a HUBZone

Ownership of the business meets the Patriot Express requirements including Veteran-owned businesses

More than 50 percent of the business's workforce is low-income or resides in an LMI census tract

Business is two years old or less

None of the above

CHOOSE ONE – Financing intangible assets:

•The purchase price of the business does not include intangible assets (including, but not limited to, goodwill,

client/customer lists, patents, copyrights, trademarks and agreements not to compete) in excess

of $500,000 YESNO

•The purchase price of the business includes intangible assets (including, but not limited to, goodwill, client/customer

lists, patents, copyrights, trademarks and agreements not to compete), in excess of $500,000 and the borrower and/or

seller are contributing at least 25% equity. (If “no”, loan is not eligible for delegated processing.)

YESNO

For construction of (or the refinancing of the construction for) a new building.

If checked, answer the following questions. If “No” loan is not eligible.

•If building will contain rental space, Applicant (or Operating Companies) will continue to occupy

at least 60% of the rentable property for the term of the loan; lease long term no more than 20% of the

rentable property to one or more tenants; plans to occupy within three years some of the remaining

rentable property not immediately occupied or leased long term; and plans to occupy within ten years

all of the rentable property not leased long term.YESNO

•Community improvements do not exceed 5 percent of the loan amount.

YESNO

•If refinancing a construction loan, the construction loan is not with the same lender.

YESNO

To provide funds for the acquisition of land or existing building or for renovation or reconstruction of an existing building.

If checked, answer the following questions. If “No” loan is not eligible.

•Applicant (or Operating Companies) will occupy at least 51% of the rentable property.

YESNO

•Loan proceeds will not be used to remodel or convert any rental space in the property.

YESNO

To provide funds for or refinance leasehold improvements. If checked, answer the following question.

If “No” loan is not eligible.

Loan proceeds will be used to improve space occupied 100% by Applicant.YESNO

To provide funds to guarantee or fund a letter of credit. If checked, loan is not eligible.

Loan is a revolving credit. If checked, loan is not eligible.

SBA Form 2301, Part D (Ver. 11-2012) 5

serving the territory where the business applicant is located.

The charge resulting in a “yes” answer was a single misdemeanor that was subsequently dropped without

prosecution and Lender has documentation from the appropriate court or prosecutor’s office showing that the charge

was dropped.

Lender is aware that the application was previously submitted to SBA under any SBA program, including SBA Express,

Community Express, PLP, CLP, Patriot Express or regular 7(a). (If checked, loan is not eligible for delegated processing.)

Loan will be collateralized by commercial property that will not meet SBA’s environmental requirements or that will require

use of a non-standard indemnification agreement. (If checked, loan is not eligible for delegated processing.)

Business or any of its principals has been involved in a federal loan or federally assisted financing that defaulted

and caused a loss to the Federal government or any of its Departments or agencies. (If checked, loan is not eligible for delegated

processing.)

G. Conflict of Interest (13 CFR Part 105)

SBA will not provide financial assistance under delegated processing authority to an applicant when granting such

financial assistance could result in the appearance of a conflict of interest between the Federal Government and the

Applicant. Please answer the following questions. If any of the answers to the following statements cannot be answered

“True,” then the application may not be submitted under delegated processing.

SBA Form 2301, Part D (Ver. 11-2012)

Lender has received written clearance of the character issue(s) from the district or branch SBA office

Lender has made a personal loan to an individual for the purpose of providing an equity injection into the business.

(If checked, loan is not eligible for delegated processing.)

YESNO

Applicant or Affiliates(s) has/have existing SBA loan(s). If checked, answer the following question. If “No” loan is not eligible.

The existing SBA loan(s) is/are current. YESNO

Question 7 on any required SBA Form 912, Statement of Personal History, for this application is

answered “Yes.” (If checked, loan is not eligible.)

Question 8 or 9 on any required SBA Form 912, Statement of Personal History, for this application is

answered “Yes.” If checked, answer the following:

The application meets one of the following criteria below (which is checked): YESNO

(If “no,” loan is not eligible for delegated processing.)

•No SBA employee, or the household member* of an SBA employee, is a sole proprietor, partner, officer, director, or stockholder

with a 10 percent or more interest, of the Applicant. [13 CFR 105.204] True

Loan is one of the following special purpose loans (If checked, loan is not eligible.):

•Disabled Assistance Loan Program (DAL) (not currently receiving appropriations)

•Pollution Control Program (not currently receiving appropriations)

•Qualified Employee Trusts (ESOP) (Loans made to an ESOP under 13 CFR 120.350 through 120.354)

•CAPLines Program (including Builders Loan Program)

•No Member of Congress, or an appointed official or employee of the legislative or judicial branch of the Federal Government, is a

sole proprietor, general partner, officer, director, or stockholder with a 10 percent or more interest, or household member of such

individual, of the Applicant. [13 CFR 105.301(c)] True

•No former SBA employee, who has been separated from the SBA for less than one year prior to the request for financial assistance, is

an employee, owner, partner, attorney, agent, owners of stock, officer, director, creditor or debtor of the Applicant. [13 CFR

105.203] True

6

•Neither the Applicant, an Associate of Applicant, close relative nor household member of an Associate of Applicant is required to

invest in Lender. True

•None of the proceeds of the loan will be used to acquire space in project for which lender has issued a real estate forward

commitment. True

(**Associate of a Lender is an officer, director, key employee, or holder of 20 percent or more of the value of the Lender’s stock or

debt instruments. An Associate of a small business is an officer, director, owner of more than 20 percent of the equity, or key

employee.)

NOTE: When there have been revisions to SBA policy regarding SBA loans that may be submitted under delegated

authority, there may be a short period of time between the issuance of the policy, regulation or statutory change (including

revisions to SOP 50 10) and a change to the form.

If that is the case for this loan application:

1. write “see attached” next to the particular statement on this form where the policy has changed; and

2. attach an explanation for each notation that identifies the current specific SBA policy since the issuance of

this edition of the form that now permits the submission of the loan under delegated authority. This must

include the specific SOP citation, SBA notice, regulation change or change in the statute.

Do not complete the statement on the form itself if the statement indicates that the loan is not eligible to be submitted

under delegated authority but the revised policy as identified by the attachment provided does.

SBA Form 2301, Part D (Ver. 11-2012)

•None of the Loan proceeds will directly or indirectly finance purchase of real estate, personal property or services from Lender or an

Associate of Lender. True

H. Ethical Requirements of Lenders (13 CFR 120.140)

• No Lender or Associate** of Lender has a real or apparent conflict of interest with Applicant, any of Applicant's Associates, or any

of the close relatives of Applicant's Associates. True

•No Lender or Associate or close relative of an associate of the lender has a significant direct or indirect financial or other interest in

the applicant, or has had such an interest within 6 months prior to the date of the application. True

•No Associate of a Lender is incarcerated, on parole, or on probation or is a convicted felon or has an adverse final civil judgment (in

a case involving fraud, breach of trust, or other conduct) that would cause the public to question the Lender's business integrity.

True

•No Lender or any Associate of Lender has accepted funding from a source that restricts, prioritizes, or conditions the types of small

businesses that Lender may assist under an SBA program or that imposes any conditions or requirements upon recipients of SBA

assistance inconsistent with SBA's loan programs or regulations. True

•No Government employee having a grade of at least GS-13 or higher is a sole proprietor, general partner, officer, director, or

stockholder with a 10 percent or more interest, or household member of such individual, of the Applicant. [13 CFR 105.301(a)]

True

•No member or employee of a Small Business Advisory Council or a SCORE volunteer is a sole proprietor, general partner, officer,

director, or stockholder with a 10 percent or more interest, or a household member of such individual, of the Applicant. [13 CFR

105.302(a)]True

(*A “household member” of an SBA employee includes: a) the spouse of the SBA employee; b) the minor children of said individual;

and c) the blood relatives of the employee, and the blood relatives of the employee’s spouse, who reside in the same place of abode as

the employee. [13 CFR § 105.201(d)])

7

Lender’s Certification:

I certify that I have accurately and correctly completed the Eligibility Checklist on behalf of the Lender, that the

above information is true and correct, to the best of my knowledge, and that I have exercised due diligence to obtain

the true and correct information. I am aware and acknowledge that SBA will not review eligibility prior to issuing an

SBA loan number and that if an SBA loan number is assigned and SBA later learns that the loan is not eligible, SBA

may deny liability on its guarantee.

Lender Signature: Date:

Name and Title:

NOTE: According to the Paperwork Reduction Act, you are not required to respond to this collection of information unless it displays a currently

valid OMB Control Number. The estimated burden for completing this form, including time for reviewing instructions, gathering data needed, and

completing and reviewing the form is 10 minutes per response. Comments or questions on the burden estimates should be sent to the SBA Desk

Officer, Office of Management and Budget, New Executive Bldg., Room 10202, Washington, DC 20503 and or to U.S. Small Business

Administration, Chief, AIB, 409 3rd St., SW, Washington DC 20416. PLEASE DO NOT SEND FORMS TO THIS ADDRESS.

SBA Form 2301, Part D (Ver. 11-2012) 8