- Employee's Withholding Exemption Certificate - Arkansas

- Employee's Withholding Certificate - Connecticut

- Employee's Withholding Exemption Certificate - Virginia

- Income Certification - Texas

- Employee's Withholding Exemption Certificate - Massachusetts

- Employee's Withholding Allowance Certificate - New Jersey

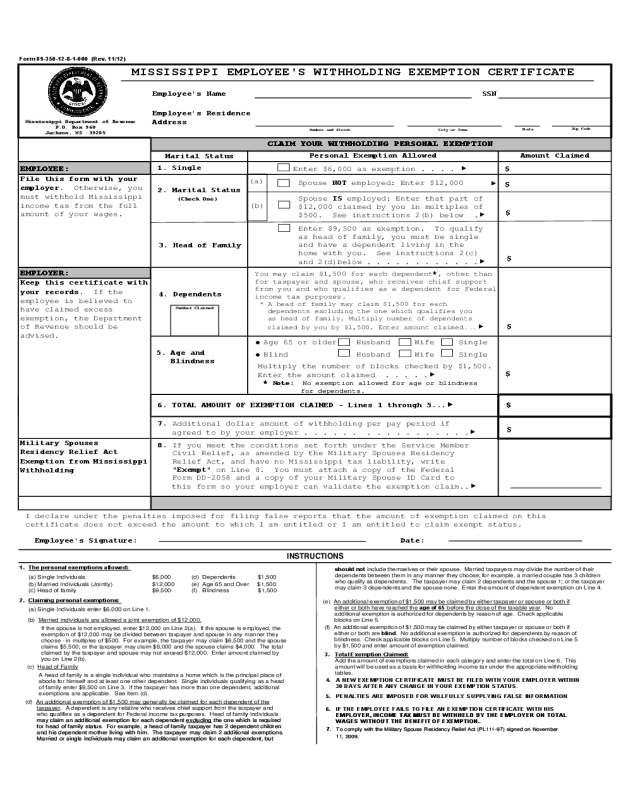

Fillable Printable Employee's Withholding Exemption Certificate - Mississippi

Fillable Printable Employee's Withholding Exemption Certificate - Mississippi

Employee's Withholding Exemption Certificate - Mississippi

Form 89-350-12-8-1-000 (Rev. 11/12)

MISSISSIPPI EMPLOYEE'S WITHHOLDING EXEMPTION CERTIFICATE

Employee's Name SSN

Employee's Residence

Address

Marital Status

EMPLOYEE:

1. Single

File this form with your

employer. Otherwise, you

must withhold Mississippi

income tax from the full

amount of your wages.

EMPLOYER:

Keep this certificate with

your records. If the

employee is believed to

have claimed excess

exemption, the Department

of Revenue should be

advised.

Personal Exemption Allowed

CLAIM YOUR WITHHOLDING PERSONAL EXEMPTION

Amount Claimed

Enter $6,000 as exemption . . . .

$

Mississippi Department of Revenue

P.O. Box 960

Jackson, MS 39205

Number and Street City or Town

State

Zip Code

(Check One)

(a)

(b)

Spouse NOT employed: Enter $12,000

$

Spouse IS employed: Enter that part of

$12,000 claimed by you in multiples of

$500. See instructions 2(b) below .

$

2. Marital Status

3. Head of Family

Enter $9,500 as exemption. To qualify

as head of family, you must be single

and have a dependent living in the

home with you. See instructions 2(c)

and 2(d)below . . . . . . . . . . . .

$

You may claim $1,500 for each dependent*, other than

for taxpayer and spouse, who receives chief support

from you and who qualifies as a dependent for Federal

income tax purposes.

* A head of family may claim $1,500 for each

dependents excluding the one which qualifies you

as head of family. Multiply number of dependents

claimed by you by $1,500. Enter amount claimed ...

4. Dependents

Number Claimed

$

5. Age and

Blindness

● Age 65 or older Husband Wife Single

● Blind Husband Wife Single

Multiply the number of blocks checked by $1,500.

Enter the amount claimed . . . . .

*

Note: No exemption allowed for age or blindness

for dependents.

$

$

1. The personal exemptions allowed:

(a) Single Individuals $6,000 (d) Dependents $1,500

(b) Married Individuals (Jointly) $12,000 (e) Age 65 and Over $1,500

(c) Head of family $9,500 (f) Blindness $1,500

2. Claiming personal exemptions:

(a) Single Individuals enter $6,000 on Line 1.

Military Spouses

Residency Relief Act

Exemption from Mississippi

Withholding

INSTRUCTIONS

6. TOTAL AMOUNT OF EXEMPTION CLAIMED - Lines 1 through 5...

* Note: No exemption allowed for age or blindness

for dependents.

$

7. Additional dollar amount of withholding per pay period if

agreed to by your employer . . . . . . . . . . . . . . . . .

$

8. If you meet the conditions set forth under the Service Member

Civil Relief, as amended by the Military Spouses Residency

Relief Act, and have no Mississippi tax liability, write

"Exempt" on Li ne 8. You must attach a copy of the Federal

Form DD-2058 and a copy of your Military Spouse ID Card to

this form so your employer can validate the exemption claim..

I declare under the penalties imposed for filing false reports that the amount of exemption claimed on this

certificate does not exceed the amount to which I am entitled or I am entitled to claim exempt status.

Employee's Signature: Date:

(e) An additional exemption of $1,500 may be c laim ed by either taxpay er or spouse or both i f

eit her or both have r eached t he age of 65 before the close of t he taxable y ear. No

addit ional exempt ion is authori zed for dependent s by reason of age. Check appli cable

blocks on Li ne 5.

(d) An additional exemption of $1,500 may generally be claimed for each dependent of the

taxpayer. A dependent is any relative who receives chief support from the taxpayer and

who qualifies as a dependent for Federal income tax purposes. Head of family individuals

may claim an additional exemption for each dependent excluding

the one which is required

for head of fami ly stat us . For example, a head of family taxpayer has 2 dependent c hildren

and his dependent mother living with him. The taxpayer may claim 2 additional exemptions.

Married or single indiv iduals may claim an additional exemption for each dependent, but

(c) Head of F ami ly

A head of family is a single individual who maintains a home which is the principal place of

abode for himsel f and at least one other dependent. Single individuals quali f yi ng as a head

of family enter $9,500 on Line 3. If the taxpayer has more than one dependent, additional

exemptions are applicable. See item (d).

(b) Married individuals are allowed a joint exemption of $12,000.

If the spouse is not employed, enter $12,000 on Line 2(a). If the spouse is employed, the

exemption of $12,000 may be divided between taxpayer and spouse in any manner they

choose - in multiples of $500. For example, the taxpayer may claim $6,500 and the spouse

claims $5,500; or the taxpayer may claim $8,000 and the spouse claims $4,000. The total

claimed by the taxpayer and spouse may not exceed $12,000. Enter amount claimed by

you on Line 2(b).

(f) An addi ti onal ex empti on of $1, 500 may be clai med by ei ther t axpay er or spouse or both i f

eit her or both are blind. No additional exemption is authorized for dependents by reason of

bli ndness. Check applicable bl ocks on Li ne 5. Multi pl y number of blocks checked on Li ne 5

by $1,500 and ent er amount of exempti on cl aimed.

should not incl ude thems elves or t heir spouse. Marri ed taxpayer s may divide the number of t heir

dependents between them in any m anner t hey choose; for example, a marri ed coupl e has 3 chi ldren

who qualify as dependents. T he taxpayer may claim 2 dependents and t he s pous e 1; or the taxpayer

may cl ai m 3 dependents and t he spouse none. E nter t he amount of dependent exempt i on on Line 4.

3. Total Exemption Claimed:

Add the amount of ex emptions c laimed in each cat egor y and enter the t otal on Line 6. This

amount will be used as a basis for withhol ding income tax under t he appr opr iate w ithholding

tables.

4. A NEW EXEMPTION CERTIFICATE MUST BE FILED WITH YOUR EMPLOYER WITHIN

30 DAYS AFTER ANY CHANGE IN YOUR EXEMPTION STATUS.

5. PENALTIES ARE IMPOSED FOR WILLFULLY SUPPLYING FALSE INFORMATION

6. IF THE EMPLOYEE FAILS TO FILE AN EXEMPTION CERTIFICATE WITH HIS

EMPLOYER, INCOME TAX MUST BE WITHHELD BY THE EMPLOYER ON TOTAL

WAGES WITHOUT THE BENEFIT OF EXEMPTION..

7

. To com ply with the Military Spouse Residency Relief Act (PL111-97) signed on November

11, 2009.

qp pp y

may claim an additional exemption for each dependent excluding

the one which is required

for head of fami ly stat us . For example, a head of family taxpayer has 2 dependent c hildren

and his dependent mother living with him. The taxpayer may claim 2 additional exemptions.

Married or single indiv iduals may claim an additional exemption for each dependent, but

EMPLOYER, INCOME TAX MUST BE WITHHELD BY THE EMPLOYER ON TOTAL

W

A

G

ES

W

I

T

H

OUT THE BENEFIT OF EXEMPTION..

7

. To com ply with the Military Spouse Residency Relief Act (PL111-97) signed on November

11, 2009.