Form 5305-SEP

2

I.R.S. SPECIFICATIONS

TO BE REMOVED BEFORE PRINTING

DO NOT PRINT — DO NOT PRINT — DO NOT PRINT — DO NOT PRINT

TLS, have you

transmitted all R

text files for this

cycle update?

Date

Action

Revised proofs

requested

Date Signature

O.K. to print

INSTRUCTIONS TO PRINTERS

FORM 5305-SEP, PAGE 1 OF 2

MARGINS; TOP 13mm (1/2"), CENTER SIDES. PRINTS: HEAD TO HEAD

PAPER: WHITE WRITING, SUB. 20. INK: BLACK

FLAT SIZE: 216mm (8-1/2") x 279mm (11")

PERFORATE: None

OMB No. 1545-0499

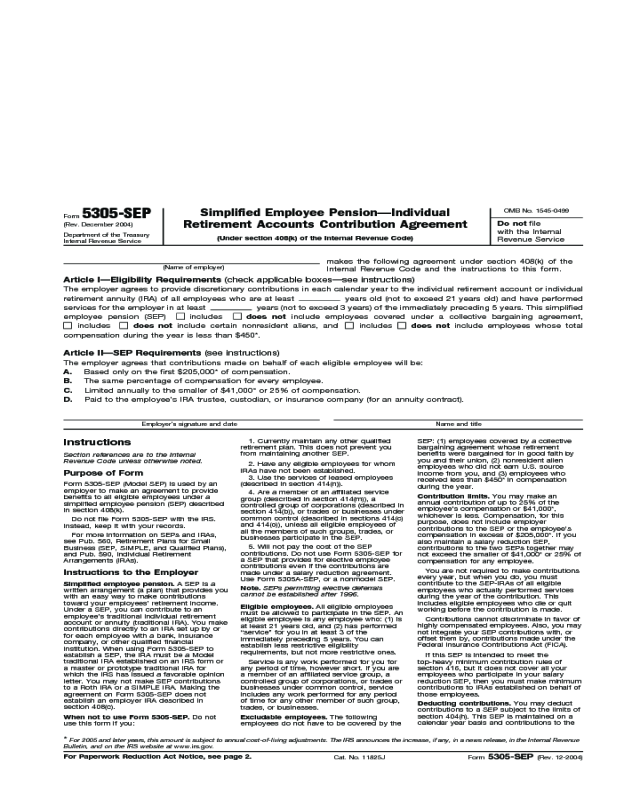

Simplified Employee Pension—Individual

Retirement Accounts Contribution Agreement

Form

5305-SEP

(Rev. December 2004)

Do not file

with the Internal

Revenue Service

Department of the Treasury

Internal Revenue Service

(Under section 408(k) of the Internal Revenue Code)

makes the following agreement under section 408(k) of the

Internal Revenue Code and the instructions to this form.

(Name of employer)

The employer agrees to provide discretionary contributions in each calendar year to the individual retirement account or individual

retirement annuity (IRA) of all employees who are at least

years old (not to exceed 21 years old) and have performed

services for the employer in at least

years (not to exceed 3 years) of the immediately preceding 5 years. This simplified

employee pension (SEP) includes does not include employees covered under a collective bargaining agreement,

includes does not include certain nonresident aliens, and includes does not include employees whose total

compensation during the year is less than $450*.

The employer agrees that contributions made on behalf of each eligible employee will be:

A. Based only on the first $205,000* of compensation.

B. The same percentage of compensation for every employee.

C. Limited annually to the smaller of $41,000* or 25% of compensation.

D. Paid to the employee’s IRA trustee, custodian, or insurance company (for an annuity contract).

Name and title

Employer’s signature and date

Section references are to the Internal

Revenue Code unless otherwise noted.

When not to use Form 5305-SEP. Do not

use this form if you:

1. Currently maintain any other qualified

retirement plan. This does not prevent you

from maintaining another SEP.

Contribution limits. You may make an

annual contribution of up to 25% of the

employee’s compensation or $41,000*,

whichever is less. Compensation, for this

purpose, does not include employer

contributions to the SEP or the employee’s

compensation in excess of $205,000*. If you

also maintain a salary reduction SEP,

contributions to the two SEPs together may

not exceed the smaller of $41,000* or 25% of

compensation for any employee.

2. Have any eligible employees for whom

IRAs have not been established.

3. Use the services of leased employees

(described in section 414(n)).

4. Are a member of an affiliated service

group (described in section 414(m)), a

controlled group of corporations (described in

section 414(b)), or trades or businesses under

common control (described in sections 414(c)

and 414(o)), unless all eligible employees of

all the members of such groups, trades, or

businesses participate in the SEP.

Purpose of Form

Eligible employees. All eligible employees

must be allowed to participate in the SEP. An

eligible employee is any employee who: (1) is

at least 21 years old, and (2) has performed

“service” for you in at least 3 of the

immediately preceding 5 years. You can

establish less restrictive eligibility

requirements, but not more restrictive ones.

Simplified employee pension. A SEP is a

written arrangement (a plan) that provides you

with an easy way to make contributions

toward your employees’ retirement income.

Under a SEP, you can contribute to an

employee’s traditional individual retirement

account or annuity (traditional IRA). You make

contributions directly to an IRA set up by or

for each employee with a bank, insurance

company, or other qualified financial

institution. When using Form 5305-SEP to

establish a SEP, the IRA must be a Model

traditional IRA established on an IRS form or

a master or prototype traditional IRA for

which the IRS has issued a favorable opinion

letter. You may not make SEP contributions

to a Roth IRA or a SIMPLE IRA. Making the

agreement on Form 5305-SEP does not

establish an employer IRA described in

section 408(c).

* For 2005 and later years, this amount is subject to annual cost-of-living adjustments. The IRS announces the increase, if any, in a news release, in the Internal Revenue

Bulletin, and on the IRS website at www.irs.gov.

Cat. No. 11825J

Form

5305-SEP (Rev. 12-2004)

Article I—Eligibility Requirements (check applicable boxes—see instructions)

Article II—SEP Requirements (see instructions)

Instructions

Instructions to the Employer

Service is any work performed for you for

any period of time, however short. If you are

a member of an affiliated service group, a

controlled group of corporations, or trades or

businesses under common control, service

includes any work performed for any period

of time for any other member of such group,

trades, or businesses.

Excludable employees. The following

employees do not have to be covered by the

Form 5305-SEP (Model SEP) is used by an

employer to make an agreement to provide

benefits to all eligible employees under a

simplified employee pension (SEP) described

in section 408(k).

5. Will not pay the cost of the SEP

contributions. Do not use Form 5305-SEP for

a SEP that provides for elective employee

contributions even if the contributions are

made under a salary reduction agreement.

Use Form 5305A-SEP, or a nonmodel SEP.

Note. SEPs permitting elective deferrals

cannot be established after 1996.

If this SEP is intended to meet the

top-heavy minimum contribution rules of

section 416, but it does not cover all your

employees who participate in your salary

reduction SEP, then you must make minimum

contributions to IRAs established on behalf of

those employees.

Deducting contributions. You may deduct

contributions to a SEP subject to the limits of

section 404(h). This SEP is maintained on a

calendar year basis and contributions to the

Contributions cannot discriminate in favor of

highly compensated employees. Also, you may

not integrate your SEP contributions with, or

offset them by, contributions made under the

Federal Insurance Contributions Act (FICA).

You are not required to make contributions

every year, but when you do, you must

contribute to the SEP-IRAs of all eligible

employees who actually performed services

during the year of the contribution. This

includes eligible employees who die or quit

working before the contribution is made.

For more information on SEPs and IRAs,

see Pub. 560, Retirement Plans for Small

Business (SEP, SIMPLE, and Qualified Plans),

and Pub. 590, Individual Retirement

Arrangements (IRAs).

Do not file Form 5305-SEP with the IRS.

Instead, keep it with your records.

For Paperwork Reduction Act Notice, see page 2.

SEP: (1) employees covered by a collective

bargaining agreement whose retirement

benefits were bargained for in good faith by

you and their union, (2) nonresident alien

employees who did not earn U.S. source

income from you, and (3) employees who

received less than $450* in compensation

during the year.

2

I.R.S. SPECIFICATIONS

TO BE REMOVED BEFORE PRINTING

DO NOT PRINT — DO NOT PRINT — DO NOT PRINT — DO NOT PRINT

INSTRUCTIONS TO PRINTERS

FORM 5305-SEP, PAGE 2 OF 2

MARGINS; TOP 13mm (1/2"), CENTER SIDES. PRINTS: HEAD TO HEAD

PAPER: WHITE WRITING, SUB. 20. INK: BLACK

FLAT SIZE: 216mm (8-1/2") x 279mm (11")

PERFORATE: None

Page 2Form 5305-SEP (Rev. 12-2004)

Tax treatment of contributions. Employer

contributions to your SEP-IRA are excluded

from your income unless there are

contributions in excess of the applicable limit.

Employer contributions within these limits will

not be included on your Form W-2.

Completing the agreement. This agreement

is considered adopted when:

Employee contributions. You may make

regular IRA contributions to an IRA. However,

the amount you can deduct may be reduced

or eliminated because, as a participant in a

SEP, you are covered by an employer

retirement plan.

Information for the Employee

The information below explains what a SEP is,

how contributions are made, and how to treat

your employer’s contributions for tax

purposes. For more information, see Pub. 590.

SEP participation. If your employer does not

require you to participate in a SEP as a

condition of employment, and you elect not to

participate, all other employees of your

employer may be prohibited from participating.

If one or more eligible employees do not

participate and the employer tries to establish

a SEP for the remaining employees, it could

cause adverse tax consequences for the

participating employees.

1. The law that relates to your IRA.

2. The tax consequences of various options

concerning your IRA.

3. Participation eligibility rules, and rules on

the deductibility of retirement savings.

Simplified employee pension. A SEP is a

written arrangement (a plan) that allows an

employer to make contributions toward your

retirement. Contributions are made to a

traditional individual retirement

account/annuity (traditional IRA).

Contributions must be made to either a

Model traditional IRA executed on an IRS

form or a master or prototype traditional IRA

for which the IRS has issued a favorable

opinion letter.

4. Situations and procedures for revoking

your IRA, including the name, address, and

telephone number of the person designated

to receive notice of revocation. This

information must be clearly displayed at the

beginning of the disclosure statement.

Your employer will provide you with a copy of

the agreement containing participation rules and

a description of how employer contributions

may be made to your IRA. Your employer must

also provide you with a copy of the completed

Form 5305-SEP and a yearly statement showing

any contributions to your IRA.

SEP-IRA amounts—rollover or transfer to

another IRA. You can withdraw or receive

funds from your SEP-IRA if, within 60 days of

receipt, you place those funds in the same or

another IRA. This is called a “rollover” and

can be done without penalty only once in any

1-year period. However, there are no

restrictions on the number of times you may

make “transfers” if you arrange to have these

funds transferred between the trustees or the

custodians so that you never have

possession of the funds.

5. A discussion of the penalties that may

be assessed because of prohibited activities

concerning your IRA.

All amounts contributed to your IRA by your

employer belong to you even after you stop

working for that employer.

6. Financial disclosure that provides the

following information:

a. Projects value growth rates of your IRA

under various contribution and retirement

schedules, or describes the method of

determining annual earnings and charges that

may be assessed.

An employer is not required to make SEP

contributions. If a contribution is made,

however, it must be allocated to all eligible

employees according to the SEP agreement.

The Model SEP (Form 5305-SEP) specifies

that the contribution for each eligible

employee will be the same percentage of

compensation (excluding compensation

greater than $205,000*) for all employees.

b. Describes whether, and for when, the

growth projections are guaranteed, or a

statement of the earnings rate and the terms

on which the projections are based.

Withdrawals. You may withdraw your

employer’s contribution at any time, but any

amount withdrawn is includible in your

income unless rolled over. Also, if withdrawals

c. States the sales commission for each

year expressed as a percentage of $1,000.

Contribution limits. Your employer will

determine the amount to be contributed to

your IRA each year. However, the amount for

any year is limited to the smaller of $41,000*

or 25% of your compensation for that year.

Compensation does not include any amount

that is contributed by your employer to your

IRA under the SEP. Your employer is not

required to make contributions every year or

to maintain a particular level of contributions.

An employer may not adopt this IRS Model

SEP if the employer maintains another

qualified retirement plan. This does not

prevent your employer from adopting this IRS

Model SEP and also maintaining an IRS

Model Salary Reduction SEP or other SEP.

However, if you work for several employers,

you may be covered by a SEP of one

employer and a different SEP or pension or

profit-sharing plan of another employer.

● IRAs have been established for all your

eligible employees;

● You have completed all blanks on the

agreement form without modification; and

● You have given all your eligible employees

the following information:

Employers who have established a SEP

using Form 5305-SEP and have furnished

each eligible employee with a copy of the

completed Form 5305-SEP and provided the

other documents and disclosures described in

Instructions to the Employer and Information

for the Employee, are not required to file the

annual information returns, Forms 5500 or

5500-EZ for the SEP. However, under Title I of

the Employee Retirement Income Security Act

of 1974 (ERISA), this relief from the annual

reporting requirements may not be available to

an employer who selects, recommends, or

influences its employees to choose IRAs into

which contributions will be made under the

SEP, if those IRAs are subject to provisions

that impose any limits on a participant’s ability

to withdraw funds (other than restrictions

imposed by the Code that apply to all IRAs).

For additional information on Title I

requirements, see the Department of Labor

regulation at 29 CFR 2520.104-48.

In addition, the financial institution must

provide you with a financial statement each

year. You may want to keep these statements

to evaluate your IRA’s investment performance.

Excess SEP contributions. Contributions

exceeding the yearly limitations may be

withdrawn without penalty by the due date

(plus extensions) for filing your tax return

(normally April 15), but are includible in your

gross income. Excess contributions left in

your SEP-IRA after that time may have

adverse tax consequences. Withdrawals of

those contributions may be taxed as

premature withdrawals.

1. A copy of Form 5305-SEP.

2. A statement that traditional IRAs other

than the traditional IRAs into which employer

SEP contributions will be made may provide

different rates of return and different terms

concerning, among other things, transfers and

withdrawals of funds from the IRAs.

3. A statement that, in addition to the

information provided to an employee at the

time the employee becomes eligible to

participate, the administrator of the SEP must

furnish each participant within 30 days of the

effective date of any amendment to the SEP,

a copy of the amendment and a written

explanation of its effects.

4. A statement that the administrator will

give written notification to each participant of

any employer contributions made under the

SEP to that participant’s IRA by the later of

January 31 of the year following the year for

which a contribution is made or 30 days after

the contribution is made.

Financial institution requirements. The

financial institution where your IRA is

maintained must provide you with a disclosure

statement that contains the following

information in plain, nontechnical language:

SEP are deductible for your tax year with or

within which the calendar year ends.

Contributions made for a particular tax year

must be made by the due date of your

income tax return (including extensions) for

that tax year.

Paperwork Reduction Act Notice. You are

not required to provide the information

requested on a form that is subject to the

Paperwork Reduction Act unless the form

displays a valid OMB control number. Books

or records relating to a form or its instructions

must be retained as long as their contents

may become material in the administration of

any Internal Revenue law. Generally, tax

returns and return information are confidential,

as required by section 6103.

Recordkeeping

1 hr., 40 min.

If you have comments concerning the

accuracy of these time estimates or suggestions

for making this form simpler, we would be

happy to hear from you. You can write to the

Internal Revenue Service, Tax Products

Coordinating Committee, SE:W:CAR:MP:T:T:SP,

1111 Constitution Ave. NW, Washington, DC

20224. Do not send this form to this address.

Instead, keep it with your records.

Learning about the

law or the form

1 hr., 35 min.

Preparing the form

1 hr., 41 min.

The time needed to complete this form will

vary depending on individual circumstances.

The estimated average time is:

occur before you reach age 59

1

⁄2, you may be

subject to a tax on early withdrawal.