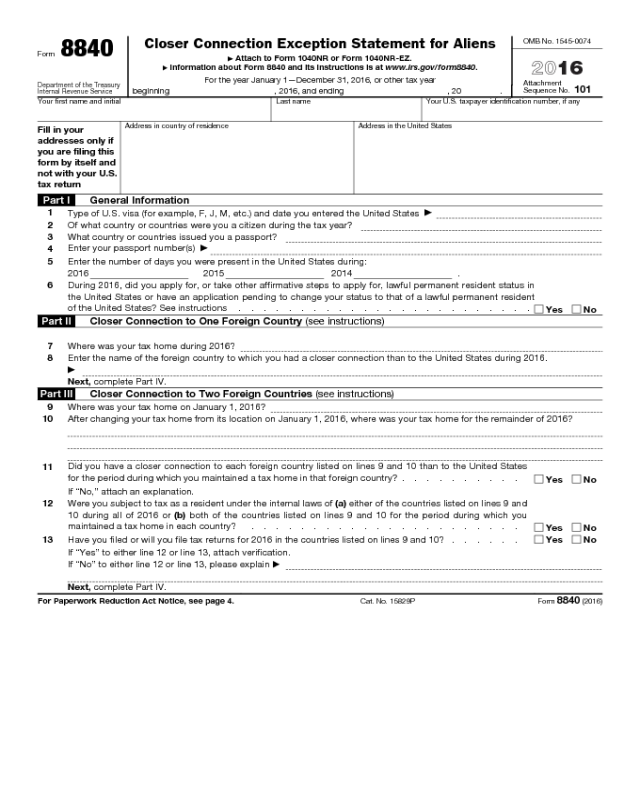

Form 8840

Form 8840

Department of the Treasury

Internal Revenue Service

Closer Connection Exception Statement for Aliens

▶

Attach to Form 1040NR or Form 1040NR-EZ.

▶

Information about Form 8840 and its instructions is at www.irs.gov/form8840.

For the year January 1—December 31, 2016, or other tax year

beginning

, 2016, and ending

, 20 .

OMB No. 1545-0074

2016

Attachment

Sequence No.

101

Your first name and initial Last name Your U.S. taxpayer identification number, if any

Fill in your

addresses only if

you are filing this

form by itself and

not with your U.S.

tax return

Address in country of residence Address in the United States

Part I General Information

1

Type of U.S. visa (for example, F, J, M, etc.) and date you entered the United States

▶

2 Of what country or countries were you a citizen during the tax year?

3

What country or countries issued you a passport?

4

Enter your passport number(s)

▶

5 Enter the number of days you were present in the United States during:

2016 2015 2014 .

6

During 2016, did you apply for, or take other affirmative steps to apply for, lawful permanent resident status in

the United States or have an application pending to change your status to that of a lawful permanent resident

of the United States? See instructions . . . . . . . . . . . . . . . . . . . . . . . .

Yes No

Part II Closer Connection to One Foreign Country (see instructions)

7 Where was your tax home during 2016?

8 Enter the name of the foreign country to which you had a closer connection than to the United States during 2016.

▶

Next, complete Part IV.

Part III Closer Connection to Two Foreign Countries (see instructions)

9 Where was your tax home on January 1, 2016?

10 After changing your tax home from its location on January 1, 2016, where was your tax home for the remainder of 2016?

11

Did you have a closer connection to each foreign country listed on lines 9 and 10 than to the United States

for the period during which you maintained a tax home in that foreign country? . . . . . . . . . .

Yes No

If “No,” attach an explanation.

12

Were you subject to tax as a resident under the internal laws of (a) either of the countries listed on lines 9 and

10 during all of 2016 or (b) both of the countries listed on lines 9 and 10 for the period during which you

maintained a tax home in each country? . . . . . . . . . . . . . . . . . . . . . .

Yes No

13 Have you filed or will you file tax returns for 2016 in the countries listed on lines 9 and 10? . . . . . .

Yes No

If “Yes” to either line 12 or line 13, attach verification.

If “No” to either line 12 or line 13, please explain

▶

Next, complete Part IV.

For Paperwork Reduction Act Notice, see page 4.

Cat. No. 15829P

Form 8840 (2016)

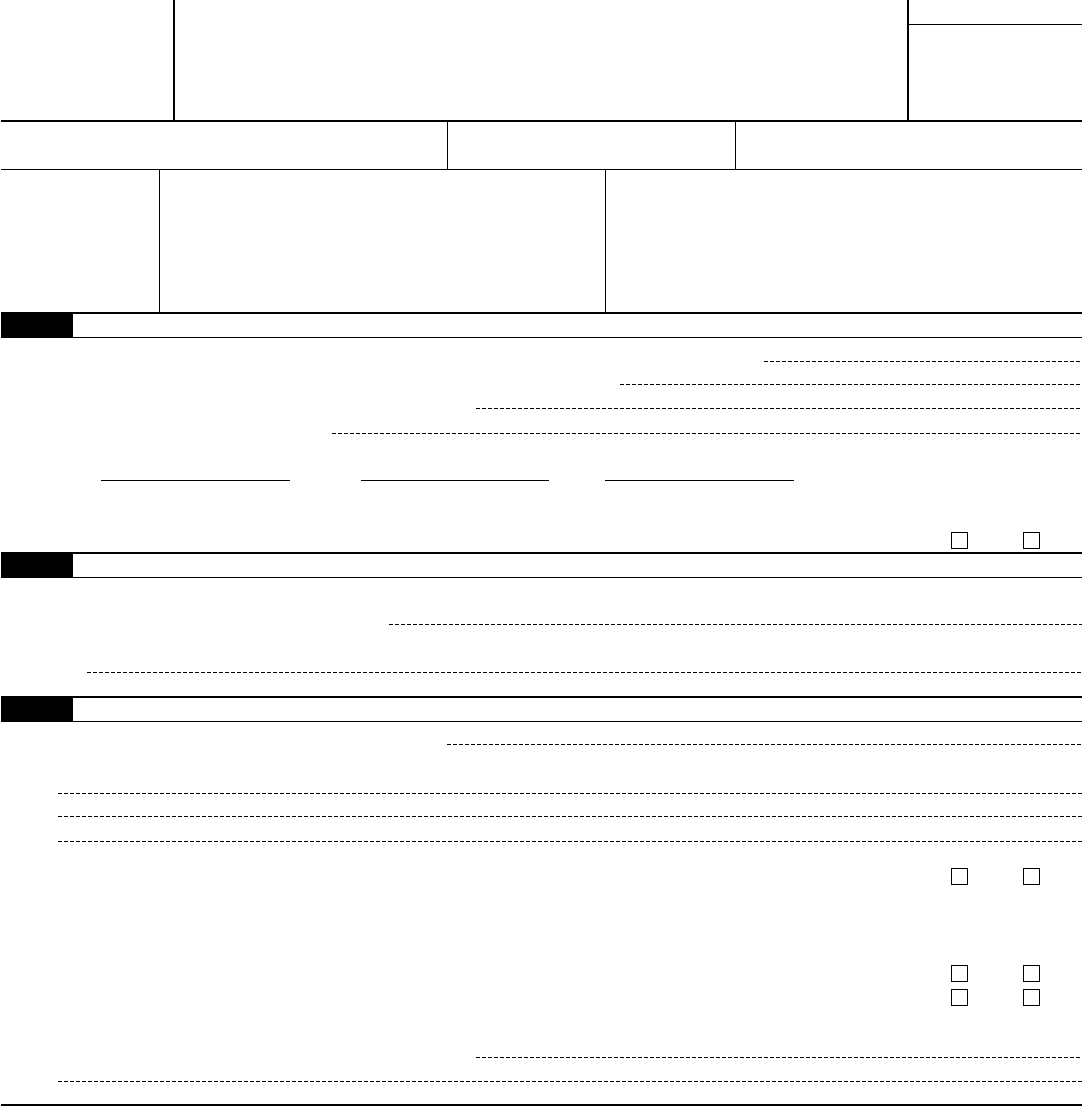

Form 8840 (2016)

Page 2

Part IV Significant Contacts With Foreign Country or Countries in 2016

14 Where was your regular or principal permanent home located during 2016? See instructions.

15

If you had more than one permanent home available to you at all times during 2016, list the location of each and

explain

▶

16 Where was your family located?

17

Where was your automobile(s) located?

18

Where was your automobile(s) registered?

19 Where were your personal belongings, furniture, etc., located?

20 Where was the bank(s) with which you conducted your routine personal banking activities located?

a

b

c

d

21 Did you conduct business activities in a location other than your tax home? . . . . . . . . . . . Yes No

If “Yes,” where?

22a

Where was your driver’s license issued?

b

If you hold a second driver’s license, where was it issued?

23 Where were you registered to vote?

24

When completing official documents, forms, etc., what country do you list as your residence?

25 Have you ever completed:

a Form W-8BEN or any other W-8 form (relating to foreign status)? . . . . . . . . . . . . . .

Yes No

b Form W-9, Request for Taxpayer Identification Number and Certification? . . . . . . . . . . .

Yes No

c Form 1078, Certificate of Alien Claiming Residence in the United States? . . . . . . . . . . . .

Yes No

d

Any other U.S. official forms? If “Yes,” indicate the form(s)

▶

Yes No

26

In what country or countries did you keep your personal, financial, and legal documents?

27 From what country or countries did you derive the majority of your 2016 income?

28 Did you have any income from U.S. sources? . . . . . . . . . . . . . . . . . . . . . Yes No

If “Yes,” what type?

29 In what country or countries were your investments located? See instructions.

30 Did you qualify for any type of “national” health plan sponsored by a foreign government? . . . . . . Yes No

If “Yes,” in what country?

If “No,” please explain

▶

If you have any other information to substantiate your closer connection to a country other than the United States or you wish

to explain in more detail any of your responses to lines 14 through 30, attach a statement to this form.

Sign here

only if you

are filing

this form by

itself and

not with

your U.S.

tax return

Under penalties of perjury, I declare that I have examined this form and the accompanying attachments, and to the best of my knowledge and belief, they

are true, correct, and complete.

▲

Your signature

▲

Date

Form 8840 (2016)

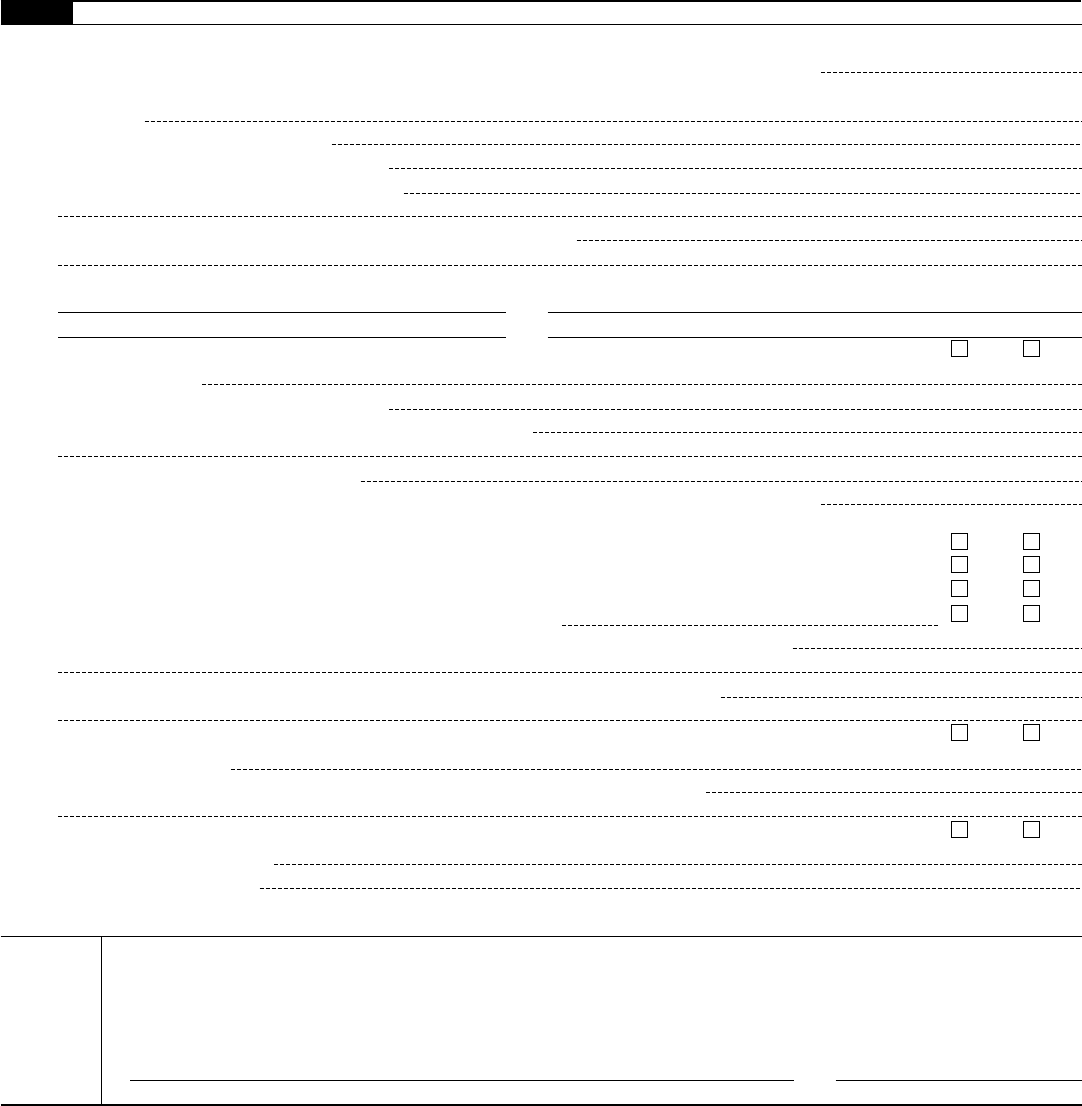

Form 8840 (2016)

Page 3

Section references are to the U.S.

Internal Revenue Code, unless otherwise

specified.

Future Developments

For the latest information about

developments related to Form 8840 and

its instructions, such as legislation

enacted after they were published, go to

www.irs.gov/form8840.

General Instructions

Purpose of Form

Use Form 8840 to claim the closer

connection to a foreign country(ies)

exception to the substantial presence

test. The exception is described later

and in Regulations section

301.7701(b)-2.

Note: You are not eligible for the closer

connection exception if any of the

following apply.

• You were present in the United States

183 days or more in calendar year 2016.

• You are a lawful permanent resident of

the United States (that is, you are a

green card holder).

• You have applied for, or taken other

affirmative steps to apply for, a green

card; or have an application pending to

change your status to that of a lawful

permanent resident of the United States.

Even if you are not eligible for the

closer connection exception, you may

qualify for nonresident status by reason

of a treaty. See the instructions for line 6

for more details.

Who Must File

If you are an alien individual and you

meet the closer connection exception to

the substantial presence test, you must

file Form 8840 with the IRS to establish

your claim that you are a nonresident of

the United States by reason of that

exception. Each alien individual must file

a separate Form 8840 to claim the closer

connection exception.

For more details on the substantial

presence test and the closer connection

exception, see Pub. 519, U.S. Tax Guide

for Aliens.

Note: You can download forms and

publications at IRS.gov.

Substantial Presence Test

You are considered a U.S. resident if you

meet the substantial presence test for

2016. You meet this test if you were

physically present in the United States

for at least:

• 31 days during 2016 and

• 183 days during the period 2016, 2015,

and 2014, counting all the days of

physical presence in 2016 but only 1/3

the number of days of presence in 2015

and only 1/6 the number of days in 2014.

Days of presence in the United States.

Generally, you are treated as being

present in the United States on any day

that you are physically present in the

country at any time during the day.

However, you do not count the

following days of presence in the United

States for purposes of the substantial

presence test.

1. Days you regularly commuted to

work in the United States from a

residence in Canada or Mexico.

2. Days you were in the United States

for less than 24 hours when you were

traveling between two places outside the

United States.

3. Days you were temporarily in the

United States as a regular crew member

of a foreign vessel engaged in

transportation between the United

States and a foreign country or a

possession of the United States unless

you otherwise engaged in trade or

business on such a day.

4. Days you were unable to leave the

United States because of a medical

condition or medical problem that arose

while you were in the United States.

5. Days you were an exempt

individual.

In general, an exempt individual is a

(a) foreign government-related individual

(b) teacher or trainee, (c) student, or

(d) professional athlete competing in a

charitable sports event. For more details,

see Pub. 519.

Note: If you qualify to exclude days of

presence in the United States because

you were an exempt individual (other

than a foreign government-related

individual) or because of a medical

condition or medical problem (see item 4

above), you must file Form 8843,

Statement for Exempt Individuals and

Individuals With a Medical Condition.

Closer Connection Exception

Even though you would otherwise meet

the substantial presence test, you will

not be treated as a U.S. resident for

2016 if:

• You were present in the United States

for fewer than 183 days during 2016,

• You establish that during 2016, you

had a tax home in a foreign country, and

• You establish that during 2016, you

had a closer connection to one foreign

country in which you had a tax home

than to the United States, unless you

had a closer connection to two foreign

countries.

Closer Connection to Two Foreign

Countries

You can demonstrate that you have a

closer connection to two foreign

countries (but not more than two) if all

five of the following apply.

1. You maintained a tax home as of

January 1, 2016, in one foreign country.

2. You changed your tax home during

2016 to a second foreign country.

3. You continued to maintain your tax

home in the second foreign country for

the rest of 2016.

4. You had a closer connection to

each foreign country than to the United

States for the period during which you

maintained a tax home in that foreign

country.

5. You are subject to tax as a resident

under the tax laws of either foreign

country for all of 2016 or subject to tax

as a resident in both foreign countries for

the period during which you maintained

a tax home in each foreign country.

Tax Home

Your tax home is your main place of

business, employment, or post of duty

regardless of where you maintain your

family home. If you do not have a regular

or main place of business because of the

nature of your work, then your tax home

is the place where you regularly live. If

you do not fit either of these categories,

you are considered an itinerant and your

tax home is wherever you work.

Establishing a Closer Connection

You will be considered to have a closer

connection to a foreign country than to

the United States if you or the IRS

establishes that you have maintained

more significant contacts with the

foreign country than with the United

States.

Your answers to the questions in Part

IV will help establish the jurisdiction to

which you have a closer connection.

When and Where To File

If you are filing a 2016 Form 1040NR or

Form 1040NR-EZ, attach Form 8840 to

it. Mail your tax return by the due date

(including extensions) to the address

shown in your tax return instructions.

If you do not have to file a 2016 tax

return, mail Form 8840 to the

Department of the Treasury, Internal

Revenue Service Center, Austin, TX

73301-0215 by the due date (including

extensions) for filing Form 1040NR or

Form 1040NR-EZ.

Form 8840 (2016)

Page 4

Penalty for Not Filing Form

8840

If you do not timely file Form 8840, you

will not be eligible to claim the closer

connection exception and may be

treated as a U.S. resident.

You will not be penalized if you can

show by clear and convincing evidence

that you took reasonable actions to

become aware of the filing requirements

and significant steps to comply with

those requirements.

Specific Instructions

Part I

Line 1

If you had a visa on the last day of the

tax year, enter your visa type and the

date you entered the United States. If

you do not have a visa, enter your U.S.

immigration status on the last day of the

tax year and the date you entered the

United States. For example, if you

entered under the visa waiver program,

enter “VWP”, the name of the Visa

Waiver Program country and the date

you entered the United States.

Line 6

If you checked the “Yes” box on line 6,

do not file Form 8840. You are not

eligible for the closer connection

exception. However, you may qualify for

nonresident status by reason of a treaty.

See Pub. 519 for details. If so, file Form

8833, Treaty-Based Return Position

Disclosure Under Section 6114 or

7701(b), with your Form 1040NR or Form

1040NR-EZ.

Parts II and III

Complete Part II or Part III (but not both)

depending on the number of countries to

which you are claiming a closer

connection. If you are claiming a closer

connection to one country, complete

Part II. If you are claiming a closer

connection to two or more countries,

complete Part III. After completing Part

II or Part III, complete Part IV.

Part IV

Line 14

A “permanent home” is a dwelling unit

(whether owned or rented, and whether

a house, an apartment, or a furnished

room) that is available at all times,

continuously and not solely for short

stays.

Line 29

For stocks and bonds, indicate the

country of origin of the stock company

or debtor. For example, if you own

shares of a U.S. publicly traded

corporation, the investment is

considered located in the United States,

even though the shares of stock are

stored in a safe deposit box in a foreign

country.

Paperwork Reduction Act Notice. We

ask for the information on this form to

carry out the Internal Revenue laws of

the United States. Section 7701(b) and

its regulations require that you give us

the information. We need it to determine

if you meet the closer connection

exception to the substantial presence

test.

You are not required to provide the

information requested on a form that is

subject to the Paperwork Reduction Act

unless the form displays a valid OMB

control number. Books or records

relating to a form or its instructions must

be retained as long as their contents

may become material in the

administration of any Internal Revenue

law. Generally, tax returns and return

information are confidential, as required

by section 6103.

The average time and expenses

required to complete and file this form

will vary depending on individual

circumstances. For the estimated

averages, see the instructions for your

income tax return.

If you have suggestions for making

this form simpler, we would be happy to

hear from you. See the instructions for

your income tax return.