Fillable Printable Notice of Income from Donated Intellectual Property

Fillable Printable Notice of Income from Donated Intellectual Property

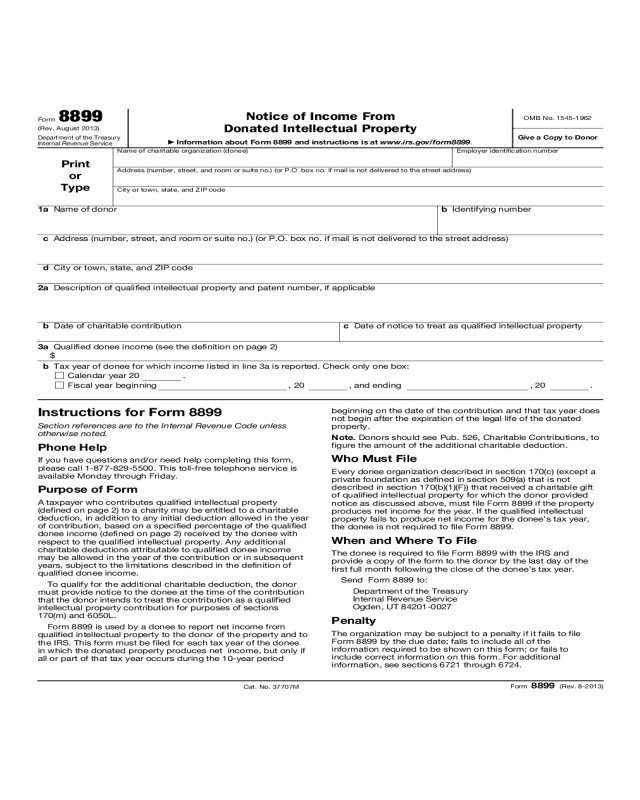

Notice of Income from Donated Intellectual Property

Form 8899

(Rev. August 2013)

Department of the Treasury

Internal Revenue Service

Notice of Income From

Donated Intellectual Property

▶

Information about Form 8899 and instructions is at www.irs.gov/form8899.

OMB No. 1545-1962

Give a Copy to Donor

Print

or

Type

Name of charitable organization (donee) Employer identification number

Address (number, street, and room or suite no.) (or P.O. box no. if mail is not delivered to the street address)

City or town, state, and ZIP code

1a Name of donor b Identifying number

c Address (number, street, and room or suite no.) (or P.O. box no. if mail is not delivered to the street address)

d City or town, state, and ZIP code

2a Description of qualified intellectual property and patent number, if applicable

b Date of charitable contribution c Date of notice to treat as qualified intellectual property

3a Qualified donee income (see the definition on page 2)

$

b Tax year of donee for which income listed in line 3a is reported. Check only one box:

Calendar year 20 .

Fiscal year beginning , 20 , and ending , 20 .

Instructions for Form 8899

Section references are to the Internal Revenue Code unless

otherwise noted.

Phone Help

If you have questions and/or need help completing this form,

please call 1-877-829-5500. This toll-free telephone service is

available Monday through Friday.

Purpose of Form

A taxpayer who contributes qualified intellectual property

(defined on page 2) to a charity may be entitled to a charitable

deduction, in addition to any initial deduction allowed in the year

of contribution, based on a specified percentage of the qualified

donee income (defined on page 2) received by the donee with

respect to the qualified intellectual property. Any additional

charitable deductions attributable to qualified donee income

may be allowed in the year of the contribution or in subsequent

years, subject to the limitations described in the definition of

qualified donee income.

To qualify for the additional charitable deduction, the donor

must provide notice to the donee at the time of the contribution

that the donor intends to treat the contribution as a qualified

intellectual property contribution for purposes of sections

170(m) and 6050L.

Form 8899 is used by a donee to report net income from

qualified intellectual property to the donor of the property and to

the IRS. This form must be filed for each tax year of the donee

in which the donated property produces net income, but only if

all or part of that tax year occurs during the 10-year period

beginning on the date of the contribution and that tax year does

not begin after the expiration of the legal life of the donated

property.

Note. Donors should see Pub. 526, Charitable Contributions, to

figure the amount of the additional charitable deduction.

Who Must File

Every donee organization described in section 170(c) (except a

private foundation as defined in section 509(a) that is not

described in section 170(b)(1)(F)) that received a charitable gift

of qualified intellectual property for which the donor provided

notice as discussed above, must file Form 8899 if the property

produces net income for the year. If the qualified intellectual

property fails to produce net income for the donee’s tax year,

the donee is not required to file Form 8899.

When and Where To File

The donee is required to file Form 8899 with the IRS and

provide a copy of the form to the donor by the last day of the

first full month following the close of the donee’s tax year.

Send Form 8899 to:

Department of the Treasury

Internal Revenue Service

Ogden, UT 84201-0027

Penalty

The organization may be subject to a penalty if it fails to file

Form 8899 by the due date; fails to include all of the

information required to be shown on this form; or fails to

include correct information on this form. For additional

information, see sections 6721 through 6724.

Cat. No. 37707M

Form 8899 (Rev. 8-2013)

Form 8899 (Rev. 8-2013)

Page 2

Definitions

Identifying number. The identifying number for individual

donors is the social security number. For other donors,

including corporations, partnerships, and estates, the

identifying number is the employer identification number. To

obtain the donor’s identifying number, you may request that the

donor complete Form W-9, Request for Taxpayer Identification

Number and Certification.

Qualified intellectual property. Qualified intellectual property

is generally any patent, copyright, trademark, trade name, trade

secret, know-how, software or similar property, or applications

or registrations of such property (other than property

contributed to or for the use of a private foundation as defined

in section 509(a) that is not described in section 170(b)(1)(F)).

See Exceptions below.

Exceptions. The following property is not considered

qualified intellectual property for purposes of the additional

charitable deduction.

1. Computer software that is readily available for purchase by

the general public, is subject to a nonexclusive license, and

has not been substantially modified.

2. A copyright held by a taxpayer:

a. Whose personal efforts created the property, or

b. In whose hands the basis of the property is determined, for

purposes of determining gain from a sale or exchange, in

whole or in part by reference to the basis of the property in

the hands of a taxpayer whose personal efforts created the

property.

Qualified donee income. Qualified donee income is any net

income received or accrued by the donee that is properly

allocable to the qualified intellectual property for the tax year of

the donee which ends within or with the tax year of the donor.

Income is not treated as allocated to qualified intellectual

property if it is received or accrued after the earlier of the

expiration of the legal life of the qualified intellectual property, or

the 10-year period beginning with the date of the contribution.

Paperwork Reduction Act Notice. We ask for the information

on this form to carry out the Internal Revenue laws of the United

States. You are required to give us the information. We need it

to ensure that you are complying with these laws and to allow

us to figure and collect the right amount of tax.

You are not required to provide the information requested on

a form that is subject to the Paperwork Reduction Act unless

the form displays a valid OMB control number. Books or

records relating to a form or its instructions must be retained as

long as their contents may become material in the

administration of any Internal Revenue law. Generally, tax

returns and return information are confidential, as required by

section 6103.

The time needed to complete and file this form will vary

depending on individual circumstances. The estimated average

time is:

Recordkeeping . . . . . . . . . . . 3 hr., 20 min.

Learning about the law . . . . . . . . . 1 hr., 0 min.

Preparing and sending

the form to the IRS . . . . . . . . . . 1 hr., 5 min.

If you have comments concerning the accuracy of this time

estimate or suggestions for making this form simpler, we would

be happy to hear from you. You can send your comments to:

Tax Forms and Publications Division

Internal Revenue Service

1111 Constitution Ave. NW, IR-6526

Washington, DC 20224

Do not send this form to this address. Instead, see When and

Where To File.