Fillable Printable 2011 Form W-2

Fillable Printable 2011 Form W-2

2011 Form W-2

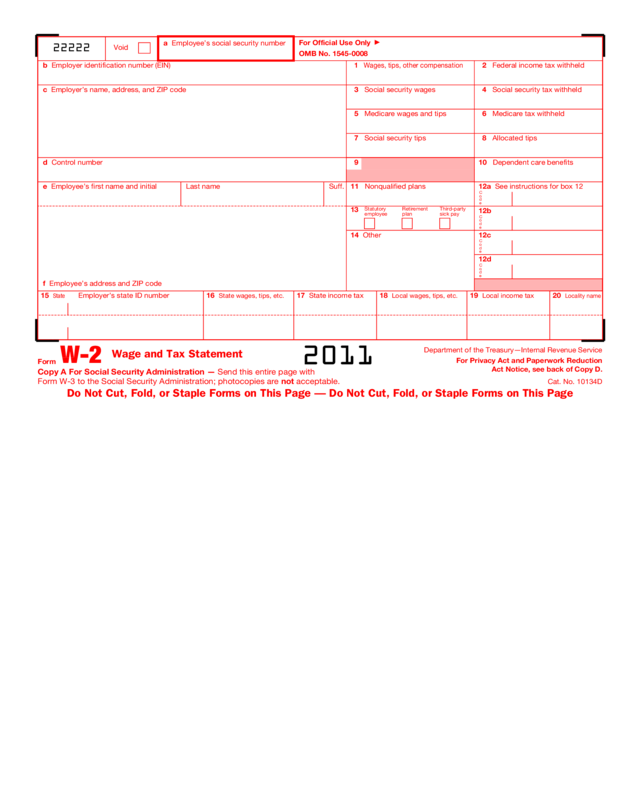

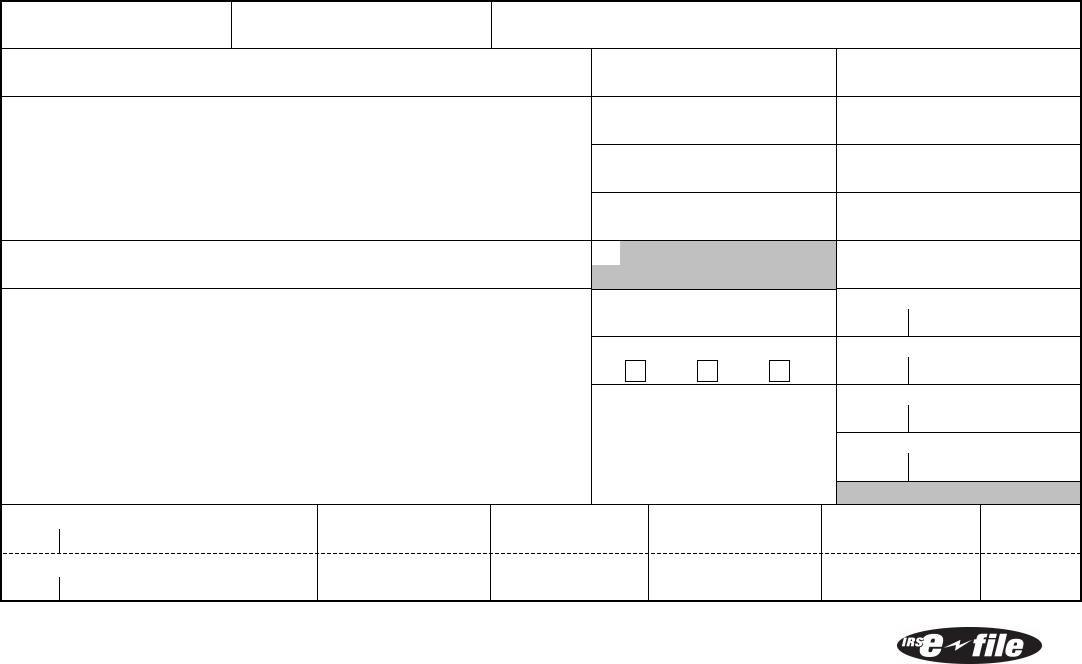

22222

Void

a Employee’s social security number

For Official Use Only

▶

OMB No. 1545-0008

b Employer identification number (EIN)

c Employer’s name, address, and ZIP code

d Control number

e Employee’s first name and initial Last name Suff.

f Employee’s address and ZIP code

1 Wages, tips, other compensation

2 Federal income tax withheld

3 Social security wages 4 Social security tax withheld

5 Medicare wages and tips 6 Medicare tax withheld

7 Social security tips 8 Allocated tips

9 10 Dependent care benefits

11 Nonqualified plans 12a See instructions for box 12

C

o

d

e

12b

C

o

d

e

12c

C

o

d

e

12d

C

o

d

e

13

Statutory

employee

Retirement

plan

Third-party

sick pay

14 Other

15 State Employer’s state ID number 16 State wages, tips, etc. 17 State income tax 18 Local wages, tips, etc. 19 Local income tax 20

Locality name

Form

W-2

Wage and Tax Statement

2011

Copy A For Social Security Administration — Send this entire page with

Form W-3 to the Social Security Administration; photocopies are not acceptable.

Department of the Treasury—Internal Revenue Service

For Privacy Act and Paperwork Reduction

Act Notice, see back of Copy D.

Cat. No. 10134D

Do Not Cut, Fold, or Staple Forms on This Page — Do Not Cut, Fold, or Staple Forms on This Page

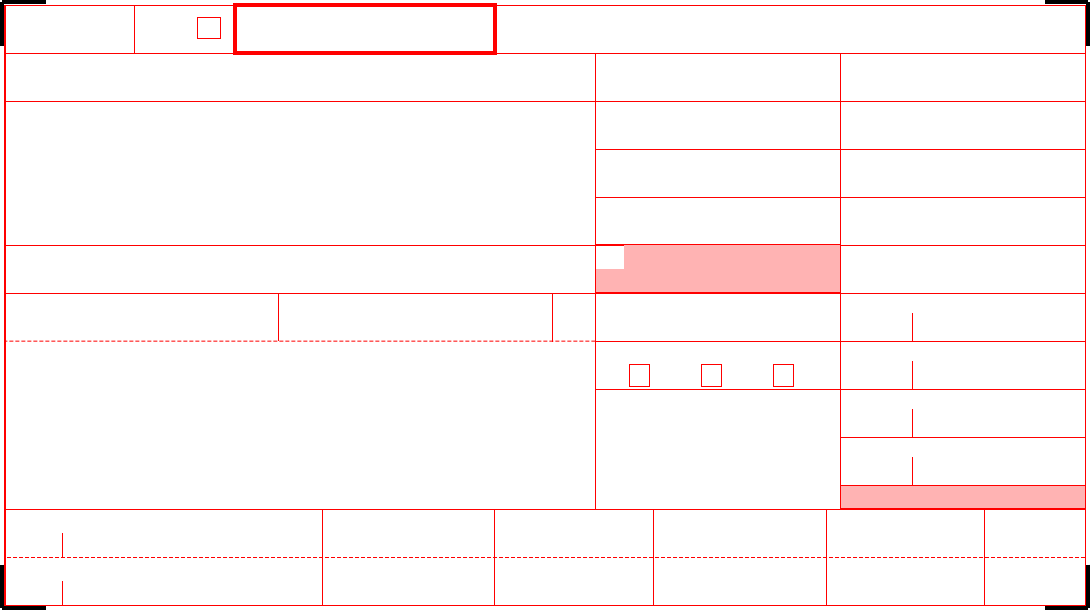

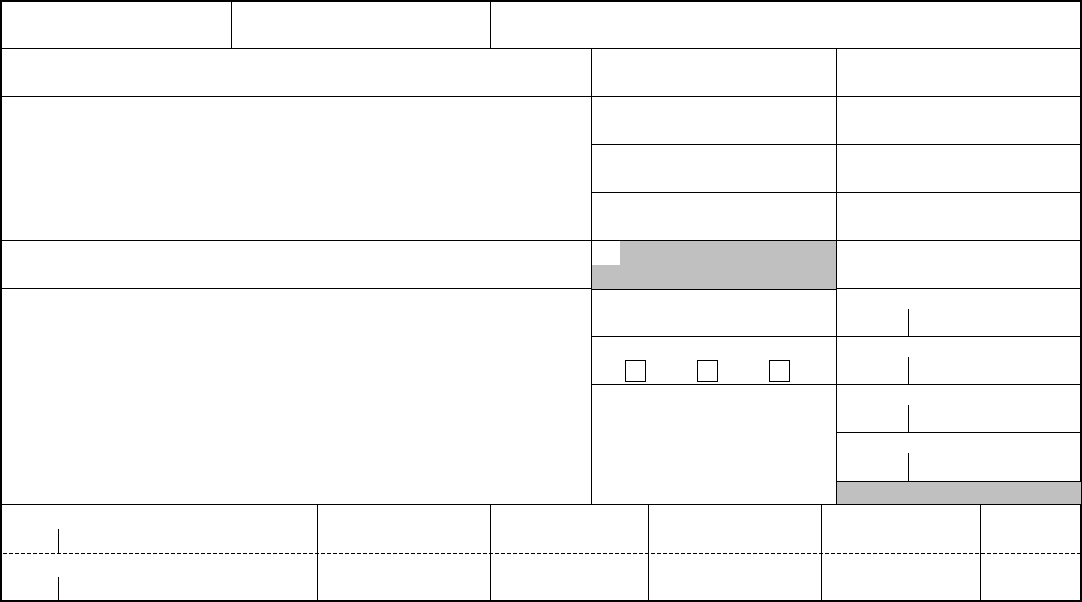

22222

a Employee’s social security number

OMB No. 1545-0008

b Employer identification number (EIN)

c Employer’s name, address, and ZIP code

d Control number

e Employee’s first name and initial Last name Suff.

f Employee’s address and ZIP code

1 Wages, tips, other compensation

2 Federal income tax withheld

3 Social security wages 4 Social security tax withheld

5 Medicare wages and tips 6 Medicare tax withheld

7 Social security tips 8 Allocated tips

9

10 Dependent care benefits

11 Nonqualified plans 12a

C

o

d

e

12b

C

o

d

e

12c

C

o

d

e

12d

C

o

d

e

13

Statutory

employee

Retirement

plan

Third-party

sick pay

14 Other

15 State Employer’s state ID number 16 State wages, tips, etc. 17 State income tax 18 Local wages, tips, etc. 19 Local income tax 20

Locality name

Form

W-2

Wage and Tax

Statement

2011

Department of the Treasury—Internal Revenue Service

Copy 1—For State, City, or Local Tax Department

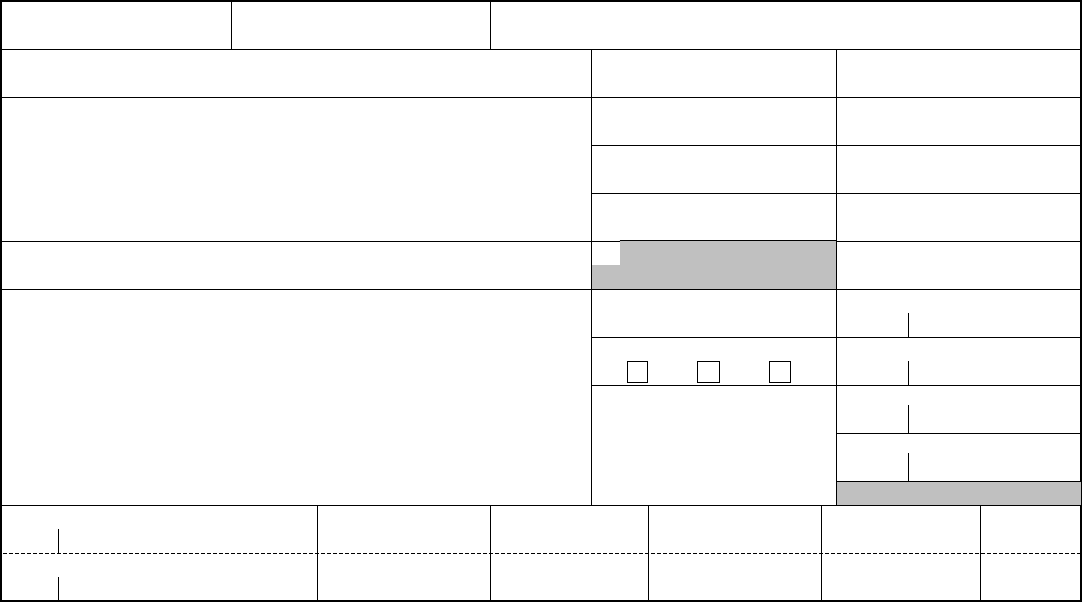

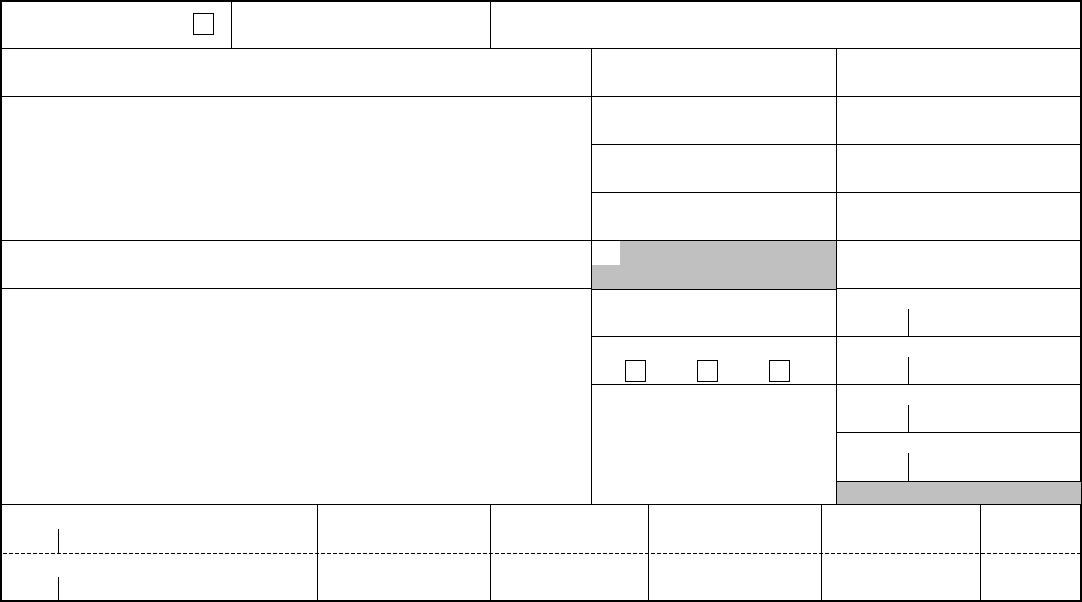

a Employee’s social security number

OMB No. 1545-0008

Safe, accurate,

FAST! Use

Visit the IRS website at

www.irs.gov/efile

b Employer identification number (EIN)

c Employer’s name, address, and ZIP code

d Control number

e Employee’s first name and initial Last name Suff.

f Employee’s address and ZIP code

1 Wages, tips, other compensation

2 Federal income tax withheld

3 Social security wages

4 Social security tax withheld

5 Medicare wages and tips 6 Medicare tax withheld

7 Social security tips 8 Allocated tips

9 10 Dependent care benefits

11 Nonqualified plans 12a See instructions for box 12

C

o

d

e

12b

C

o

d

e

12c

C

o

d

e

12d

C

o

d

e

13

Statutory

employee

Retirement

plan

Third-party

sick pay

14 Other

15 State Employer’s state ID number 16 State wages, tips, etc. 17 State income tax 18 Local wages, tips, etc. 19 Local income tax 20

Locality name

Form

W-2

Wage and Tax

Statement

2011

Department of the Treasury—Internal Revenue Service

Copy B—To Be Filed With Employee’s FEDERAL Tax Return.

This information is being furnished to the Internal Revenue Service.

Notice to Employee

Refund. Even if you do not have to file a tax return, you

should file to get a refund if box 2 shows federal income

tax withheld or if you can take the earned income credit.

Earned income credit (EIC). You may be able to take the

EIC for 2011 if (a) you do not have a qualifying child and

you earned less than $13,660 ($18,740 if married filing

jointly), (b) you have one qualifying child and you earned

less than $36,052 ($41,132 if married filing jointly), (c) you

have two qualifying children and you earned less than

$40,964 ($46,044 if married filing jointly), or (d) you have

three or more qualifying children and you earned less

than $43,998 ($49,078 if married filing jointly). You and

any qualifying children must have valid social security

numbers (SSNs). You cannot take the EIC if your

investment income is more than $3,150. Any EIC that is

more than your tax liability is refunded to you, but only

if you file a tax return.

Clergy and religious workers. If you are not subject to

social security and Medicare taxes, see Pub. 517, Social

Security and Other Information for Members of the Clergy

and Religious Workers.

Corrections. If your name, SSN, or address is incorrect,

correct Copies B, C, and 2 and ask your employer to

correct your employment record. Be sure to ask the

employer to file Form W-2c, Corrected Wage and Tax

Statement, with the Social Security Administration (SSA)

to correct any name, SSN, or money amount error

reported to the SSA on Form W-2. If your name and SSN

are correct but are not the same as shown on your social

security card, you should ask for a new card that displays

your correct name at any SSA office or by calling

1-800-772-1213. You also may visit the SSA at

www.socialsecurity.gov.

Cost of employer-sponsored health coverage (if such

cost is provided by the employer). The reporting in Box

12, using Code DD, of the cost of employer-sponsored

health coverage is for your information only. The amount

reported with Code DD is not taxable.

Credit for excess taxes. If you had more than one

employer in 2011 and more than $4,485.60 in social

security and/or Tier I railroad retirement (RRTA) taxes

were withheld, you may be able to claim a credit for the

excess against your federal income tax. If you had more

than one railroad employer and more than $3,088.80 in

Tier II RRTA tax was withheld, you also may be able to

claim a credit. See your Form 1040 or Form 1040A

instructions and Pub. 505, Tax Withholding and

Estimated Tax.

(Also see Instructions for Employee on the back of Copy C.)

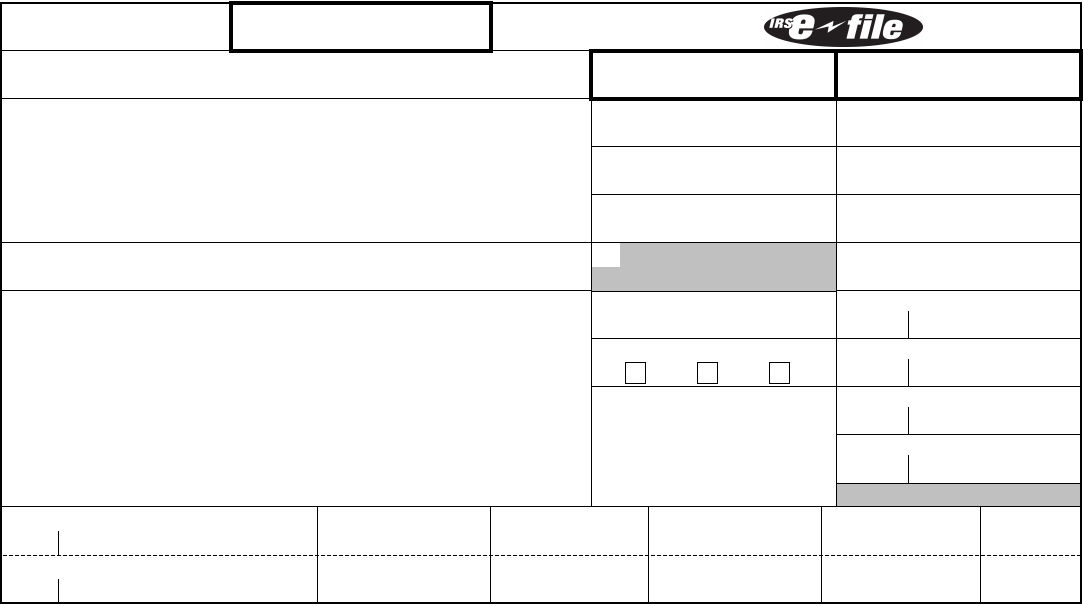

a Employee’s social security number

OMB No. 1545-0008

This information is being furnished to the Internal Revenue Service. If you

are required to file a tax return, a negligence penalty or other sanction

may be imposed on you if this income is taxable and you fail to report it.

b Employer identification number (EIN)

c Employer’s name, address, and ZIP code

d Control number

e Employee’s first name and initial Last name Suff.

f Employee’s address and ZIP code

1 Wages, tips, other compensation

2 Federal income tax withheld

3 Social security wages 4 Social security tax withheld

5 Medicare wages and tips 6 Medicare tax withheld

7 Social security tips 8 Allocated tips

9

10 Dependent care benefits

11 Nonqualified plans 12a See instructions for box 12

C

o

d

e

12b

C

o

d

e

12c

C

o

d

e

12d

C

o

d

e

13

Statutory

employee

Retirement

plan

Third-party

sick pay

14 Other

15 State Employer’s state ID number 16 State wages, tips, etc. 17 State income tax 18 Local wages, tips, etc. 19 Local income tax 20

Locality name

Form

W-2

Wage and Tax

Statement

2011

Department of the Treasury—Internal Revenue Service

Safe, accurate

FAST! Use

Copy C—For EMPLOYEE’S RECORDS (See Notice to

Employee on the back of Copy B.)

Instructions for Employee (Also see Notice to

Employee, on the back of Copy B.)

Box 1. Enter this amount on the wages line of your tax return.

Box 2. Enter this amount on the federal income tax withheld line of

your tax return.

Box 8. This amount is not included in boxes 1, 3, 5, or 7. For

information on how to report tips on your tax return, see your Form

1040 instructions.

Unless you have records that show you did not receive the

amount reported in box 8 as allocated tips, you must file Form

4137, Social Security and Medicare Tax on Unreported Tip Income,

with your income tax return to report the allocated tip amount. On

Form 4137 you will figure the social security and Medicare tax owed

on the allocated tips shown on your Form(s) W-2 that you must

report as income and on other tips you did not report to your

employer. By filing Form 4137, your social security tips will be

credited to your social security record (used to figure your benefits).

Box 10. This amount is the total dependent care benefits that your

employer paid to you or incurred on your behalf (including amounts

from a section 125 (cafeteria) plan). Any amount over $5,000 is also

included in box 1. Complete Form 2441, Child and Dependent Care

Expenses, to compute any taxable and nontaxable amounts.

Box 11. This amount is (a) reported in box 1 if it is a distribution

made to you from a nonqualified deferred compensation or

nongovernmental section 457(b) plan or (b) included in box 3 and/or

5 if it is a prior year deferral under a nonqualified or section 457(b)

plan that became taxable for social security and Medicare taxes this

year because there is no longer a substantial risk of forfeiture of

your right to the deferred amount.

Box 12. The following list explains the codes shown in box 12. You

may need this information to complete your tax return. Elective

deferrals (codes D, E, F, and S) and designated Roth

contributions (codes AA, BB, and EE) under all plans are generally

limited to a total of $16,500 ($11,500 if you only have SIMPLE plans;

$19,500 for section 403(b) plans if you qualify for the 15-year rule

explained in Pub. 571). Deferrals under code G are limited to

$16,500. Deferrals under code H are limited to $7,000.

However, if you were at least age 50 in 2011, your employer may

have allowed an additional deferral of up to $5,500 ($2,500 for

section 401(k)(11) and 408(p) SIMPLE plans). This additional deferral

amount is not subject to the overall limit on elective deferrals. For

code G, the limit on elective deferrals may be higher for the last 3

years before you reach retirement age. Contact your plan

administrator for more information. Amounts in excess of the overall

elective deferral limit must be included in income. See the “Wages,

Salaries, Tips, etc.” line instructions for Form 1040.

Note. If a year follows code D through H, S, Y, AA, BB, or EE, you

made a make-up pension contribution for a prior year(s) when you

were in military service. To figure whether you made excess

deferrals, consider these amounts for the year shown, not the

current year. If no year is shown, the contributions are for the

current year.

A—Uncollected social security or RRTA tax on tips. Include this tax

on Form 1040. See “Total Tax” in the Form 1040 instructions.

B—Uncollected Medicare tax on tips. Include this tax on Form

1040. See “Total Tax” in the Form 1040 instructions.

C—Taxable cost of group-term life insurance over $50,000 (included

in boxes 1, 3 (up to social security wage base), and 5)

D—Elective deferrals to a section 401(k) cash or deferred

arrangement. Also includes deferrals under a SIMPLE retirement

account that is part of a section 401(k) arrangement.

E—Elective deferrals under a section 403(b) salary reduction

agreement

(continued on back of Copy 2)

a Employee’s social security number

OMB No. 1545-0008

b Employer identification number (EIN)

c Employer’s name, address, and ZIP code

d Control number

e Employee’s first name and initial Last name Suff.

f Employee’s address and ZIP code

1 Wages, tips, other compensation

2 Federal income tax withheld

3 Social security wages 4 Social security tax withheld

5 Medicare wages and tips 6 Medicare tax withheld

7 Social security tips 8 Allocated tips

9

10 Dependent care benefits

11 Nonqualified plans 12a

C

o

d

e

12b

C

o

d

e

12c

C

o

d

e

12d

C

o

d

e

13

Statutory

employee

Retirement

plan

Third-party

sick pay

14 Other

15 State Employer’s state ID number 16 State wages, tips, etc. 17 State income tax 18 Local wages, tips, etc. 19 Local income tax 20

Locality name

Form

W-2

Wage and Tax

Statement

2011

Department of the Treasury—Internal Revenue Service

Copy 2—To Be Filed With Employee’s State, City, or Local

Income Tax Return.

Instructions for Employee (continued from back of

Copy C)

F—Elective deferrals under a section 408(k)(6) salary reduction SEP

G—Elective deferrals and employer contributions (including nonelective

deferrals) to a section 457(b) deferred compensation plan

H—Elective deferrals to a section 501(c)(18)(D) tax-exempt organization

plan. See “Adjusted Gross Income” in the Form 1040 instructions for

how to deduct.

J—Nontaxable sick pay (information only, not included in boxes 1, 3, or

5)

K—20% excise tax on excess golden parachute payments. See “Total

Tax” in the Form 1040 instructions.

L—Substantiated employee business expense reimbursements

(nontaxable)

M—Uncollected social security or RRTA tax on taxable cost of group-

term life insurance over $50,000 (former employees only). See “Total

Tax” in the Form 1040 instructions.

N—Uncollected Medicare tax on taxable cost of group-term life

insurance over $50,000 (former employees only). See “Total Tax” in the

Form 1040 instructions.

P—Excludable moving expense reimbursements paid directly to

employee (not included in boxes 1, 3, or 5)

Q—Nontaxable combat pay. See the instructions for Form 1040 or Form

1040A for details on reporting this amount.

R—Employer contributions to your Archer MSA. Report on Form 8853,

Archer MSAs and Long-Term Care Insurance Contracts.

S—Employee salary reduction contributions under a section 408(p)

SIMPLE (not included in box 1)

T—Adoption benefits (not included in box 1). Complete Form 8839,

Qualified Adoption Expenses, to compute any taxable and nontaxable

amounts.

V—Income from exercise of nonstatutory stock option(s) (included in

boxes 1, 3 (up to social security wage base), and 5). See Pub. 525 and

instructions for Schedule D (Form 1040) for reporting requirements.

W—Employer contributions (including amounts the employee elected to

contribute using a section 125 (cafeteria) plan) to your health savings

account. Report on Form 8889, Health Savings Accounts (HSAs).

Y—Deferrals under a section 409A nonqualified deferred compensation

plan

Z—Income under section 409A on a nonqualified deferred

compensation plan. This amount is also included in box 1. It is subject

to an additional 20% tax plus interest. See “Total Tax” in the Form 1040

instructions.

AA—Designated Roth contributions under a section 401(k) plan

BB—Designated Roth contributions under a section 403(b) plan

DD—Cost of employer-sponsored health coverage. The amount

reported with Code DD is not taxable.

EE—Designated Roth contributions under a governmental section

457(b) plan. This amount does not apply to contributions under a tax-

exempt organization section 457(b) plan.

Box 13. If the “Retirement plan” box is checked, special limits may

apply to the amount of traditional IRA contributions you may deduct.

Note. Keep Copy C of Form W-2 for at least 3 years after the due date

for filing your income tax return. However, to help protect your social

security benefits, keep Copy C until you begin receiving social security

benefits, just in case there is a question about your work record and/or

earnings in a particular year. Compare the Social Security wages and

the Medicare wages to the information shown on your annual (for

workers over 25) Social Security Statement.

Void

a Employee’s social security number

OMB No. 1545-0008

b Employer identification number (EIN)

c Employer’s name, address, and ZIP code

d Control number

e Employee’s first name and initial Last name Suff.

f Employee’s address and ZIP code

1 Wages, tips, other compensation

2 Federal income tax withheld

3 Social security wages 4 Social security tax withheld

5 Medicare wages and tips 6 Medicare tax withheld

7 Social security tips 8 Allocated tips

9

10 Dependent care benefits

11 Nonqualified plans 12a See instructions for box 12

C

o

d

e

12b

C

o

d

e

12c

C

o

d

e

12d

C

o

d

e

13

Statutory

employee

Retirement

plan

Third-party

sick pay

14 Other

15 State Employer’s state ID number 16 State wages, tips, etc. 17 State income tax 18 Local wages, tips, etc. 19 Local income tax 20

Locality name

Form

W-2

Wage and Tax

Statement

2011

Department of the Treasury—Internal Revenue Service

For Privacy Act and Paperwork Reduction

Act Notice, see back of Copy D.

Copy D — For Employer.

Employers, Please Note—

Specific information needed to complete Form W-2 is available

in a separate booklet titled 2011 Instructions for Forms W-2 and

W-3. You can order those instructions and additional forms by

calling 1-800-TAX-FORM (1-800-829-3676). You also can get

forms and instructions at IRS.gov.

Caution. You cannot file Forms W-2/W-2c and W-3/W-3c that

you print from IRS.gov with SSA. The SSA's equipment is not

able to process these forms. Instead, you can use online fill-in

forms to create and submit Forms W-2/W-2c and W-3/W-3c to

the SSA electronically. For more information, visit the SSA's

Employer W-2 Filing Instructions & Information page at

www.socialsecurity.gov/employer and click on "How to File

W-2s."

Due dates. Furnish Copies B, C, and 2 to the employee

generally by January 31, 2012.

File Copy A with the SSA by February 29, 2012. Send all

Copies A with Form W-3, Transmittal of Wage and Tax

Statements. If you file electronically (required if submitting 250

or more Forms W-2), the due date is April 2, 2012.

Need help? If you have questions about reporting on Form W-2,

call the information reporting customer service site toll free at

1-866-455-7438 or 304-263-8700 (not toll free). For TTY/TDD

equipment, call 304-579-4827 (not toll free). The hours of

operation are 8:30 a.m. to 4:30 p.m., Eastern time.

Privacy Act and Paperwork Reduction Act Notice. We ask for

the information on Forms W-2 and W-3 to carry out the Internal

Revenue laws of the United States. We need it to figure and

collect the right amount of tax. Section 6051 and its regulations

require you to furnish wage and tax statements to employees,

the Social Security Administration, and the Internal Revenue

Service. Section 6109 requires you to provide your employer

identification number (EIN). If you fail to provide this information

in a timely manner, you may be subject to penalties. Failure to

provide this information, or providing false or fraudulent

information, may subject you to penalties.

You are not required to provide the information requested on

a form that is subject to the Paperwork Reduction Act unless

the form displays a valid OMB control number. Books or

records relating to a form or its instructions must be retained as

long as their contents may become material in the

administration of any Internal Revenue law.

Generally, tax returns and return information are confidential,

as required by section 6103. However, section 6103 allows or

requires the Internal Revenue Service to disclose or give the

information shown on your return to others as described in the

Code. For example, we may disclose your tax information to the

Department of Justice for civil and/or criminal litigation, and to

cities, states, the District of Columbia, and U.S. commonwealths

and possessions for use in administering their tax laws. We may

also disclose this information to other countries under a tax

treaty, to federal and state agencies to enforce federal nontax

criminal laws, or to federal law enforcement and intelligence

agencies to combat terrorism.

The time needed to complete and file these forms will vary

depending on individual circumstances. The estimated average

times are: Form W-2—30 minutes, and Form W-3—28 minutes.

If you have comments concerning the accuracy of these time

estimates or suggestions for making these forms simpler, we

would be happy to hear from you. You can write to the Internal

Revenue Service, Tax Products Coordinating Committee,

SE:W:CAR:MP:T:T:SP, 1111 Constitution Ave. NW, IR-6526,

Washington, DC 20224. Do not send Forms W-2 and W-3 to

this address. Instead, see Where to file paper forms in the

Instructions for Forms W-2 and W-3.