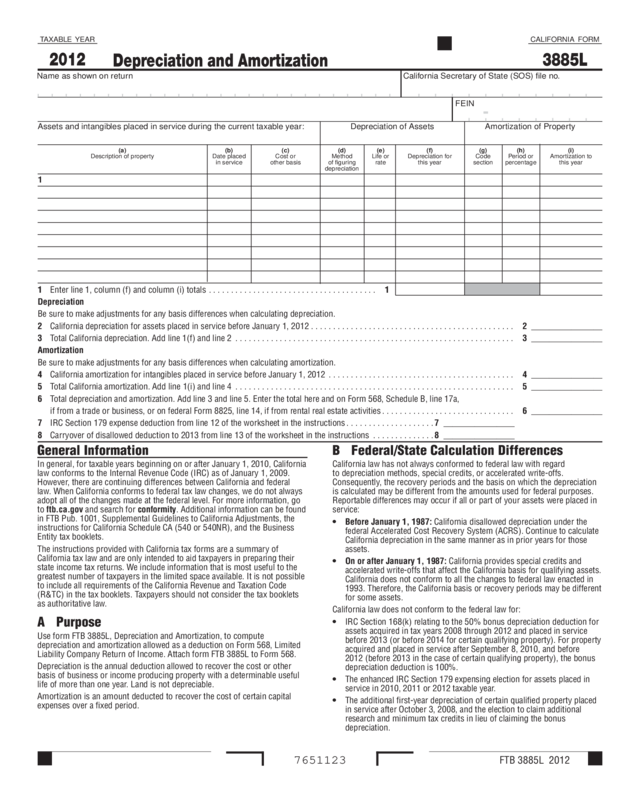

Fillable Printable 2012 Form 3885L - Depreciation And Amortization

Fillable Printable 2012 Form 3885L - Depreciation And Amortization

2012 Form 3885L - Depreciation And Amortization

FTB 3885L 2012

Depreciation and Amortization

TAXABLE YEAR

2012

7651123

CALIFORNIA FORM

3885L

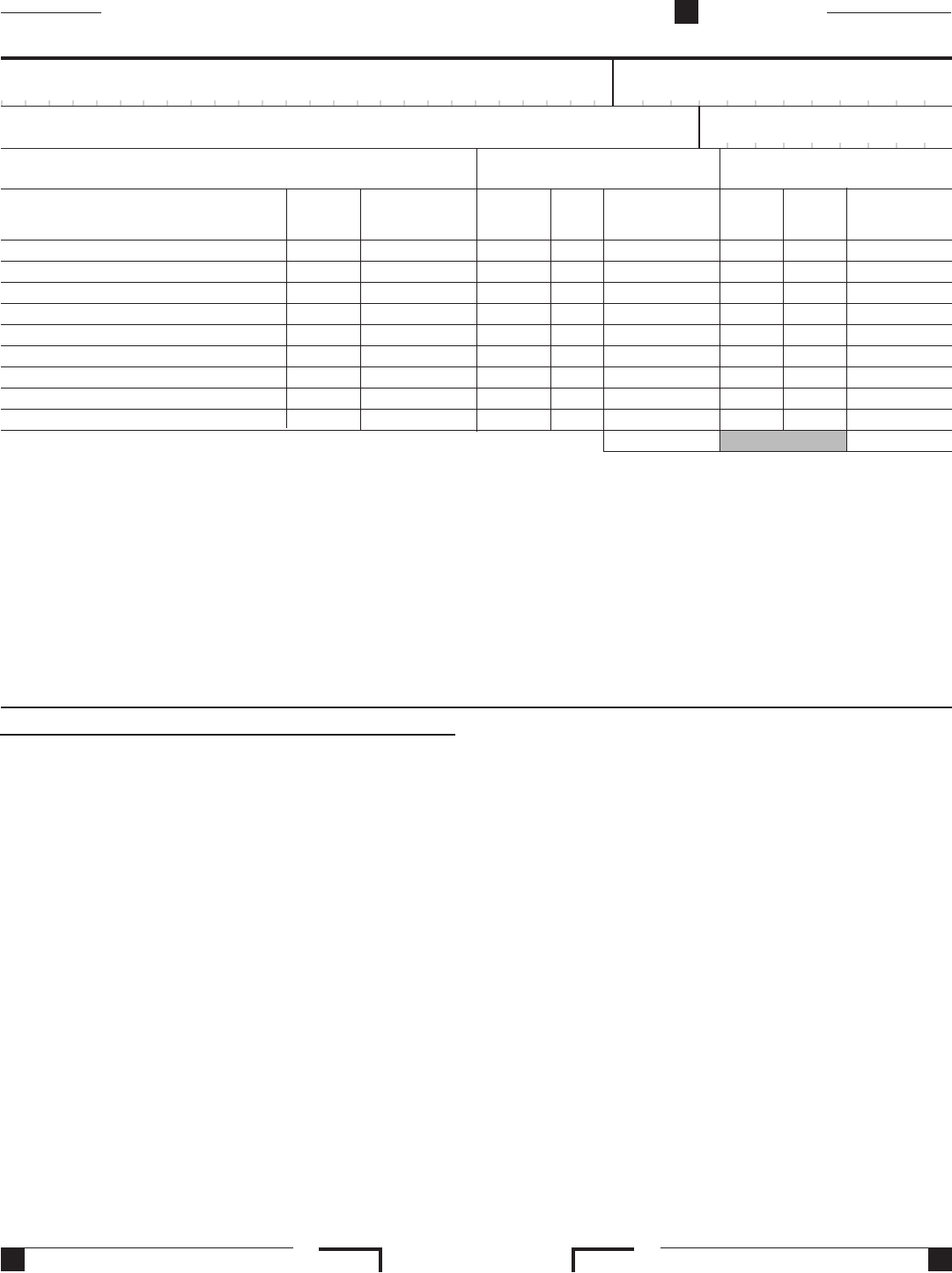

Assets and intangibles placed in service during the current taxable year: Depreciation of Assets Amortization of Property

(a) (b) (c) (d) (e) (f) (g) (h) (i)

Description of property Date placed Cost or Method Life or Depreciation for Code Period or Amortization to

in service other basis of figuring rate this year section percentage this year

depreciation

1

1 Enter line 1, column (f) and column (i) totals ...................................... 1

Depreciation

Be sure to make adjustments for any basis differences when calculating depreciation.

2 California depreciation for assets placed in service before January 1, 2012 .............................................. 2 ________________

3 Total California depreciation. Add line 1(f) and line 2 ............................................................... 3 ________________

Amortization

Be sure to make adjustments for any basis differences when calculating amortization.

4 California amortization for intangibles placed in service before January 1, 2012 .......................................... 4 ________________

5 Total California amortization. Add line 1(i) and line 4 ............................................................... 5 ________________

6 Total depreciation and amortization. Add line 3 and line 5. Enter the total here and on Form 568, Schedule B, line 17a,

if from a trade or business, or on federal Form 8825, line 14, if from rental real estate activities

.............................. 6 ________________

7 IRC Section 179 expense deduction from line 12 of the worksheet in the instructions ....................7 ________________

8 Carryover of disallowed deduction to 2013 from line 13 of the worksheet in the instructions ..............8 ________________

-

Name as shown on return California Secretary of State (SOS) file no.

FEIN

General Information

In general, for taxable years beginning on or after January 1, 2010, California

law conforms to the Internal Revenue Code (IRC) as of January 1, 2009.

However, there are continuing differences between California and federal

law. When California conforms to federal tax law changes, we do not always

adopt all of the changes made at the federal level. For more information, go

to ftb.ca.gov and search for conformity. Additional information can be found

in FTB Pub. 1001, Supplemental Guidelines to California Adjustments, the

instructions for California Schedule CA (540 or 540NR), and the Business

Entity tax booklets.

The instructions provided with California tax forms are a summary of

California tax law and are only intended to aid taxpayers in preparing their

state income tax returns. We include information that is most useful to the

greatest number of taxpayers in the limited space available. It is not possible

to include all requirements of the California Revenue and Taxation Code

(R&TC) in the tax booklets. Taxpayers should not consider the tax booklets

as authoritative law.

A Purpose

Use form FTB 3885L, Depreciation and Amortization, to compute

depreciation and amortization allowed as a deduction on Form 568, Limited

Liability Company Return of Income. Attach form FTB 3885L to Form 568.

Depreciation is the annual deduction allowed to recover the cost or other

basis of business or income producing property with a determinable useful

life of more than one year. Land is not depreciable.

Amortization is an amount deducted to recover the cost of certain capital

expenses over a fixed period.

B Federal/State Calculation Differences

California law has not always conformed to federal law with regard

to depreciation methods, special credits, or accelerated write-offs.

Consequently, the recovery periods and the basis on which the depreciation

is calculated may be different from the amounts used for federal purposes.

Reportable differences may occur if all or part of your assets were placed in

service:

•

Before January 1, 1987: California disallowed depreciation under the

federal Accelerated Cost Recovery System (ACRS). Continue to calculate

California depreciation in the same manner as in prior years for those

assets.

• On or after January 1, 1987: California provides special credits and

accelerated write-offs that affect the California basis for qualifying assets.

California does not conform to all the changes to federal law enacted in

1993. Therefore, the California basis or recovery periods may be different

for some assets.

California law does not conform to the federal law for:

•

IRC Section 168(k) relating to the 50% bonus depreciation deduction for

assets acquired in tax years 2008 through 2012 and placed in service

before 2013 (or before 2014 for certain qualifying property). For property

acquired and placed in service after September 8, 2010, and before

2012 (before 2013 in the case of certain qualifying property), the bonus

depreciation deduction is 100%.

• The enhanced IRC Section 179 expensing election for assets placed in

service in 2010, 2011 or 2012 taxable year.

• The additional first-year depreciation of certain qualified property placed

in service after October 3, 2008, and the election to claim additional

research and minimum tax credits in lieu of claiming the bonus

depreciation.

Page 2 FTB 3885L Instructions 2012

Additional differences may occur for the following:

•

Luxury Automobile Depreciation: California generally conforms to the

federal 2003 increase (IRC Section 280F) for the limitation on luxury

automobile depreciation. In addition, SUVs and minivans built on a truck

chassis are included in the definition of trucks and vans when applying

the 6,000 pound gross weight limit.

• Amortization of Certain Intangibles (IRC Section 197): Property

classified as Section 197 property under federal law is also Section 197

property for California purposes. There is no separate California election

required or allowed. However, for Section 197 property acquired before

January 1, 1994, the California adjusted basis as of January 1, 1994,

must be amortized over the remaining federal amortization period.

• Qualified Indian Reservation Property: California has not conformed

to the accelerated recovery periods available under the Alternative

Depreciation System (ADS) for such property.

• Grapevines subject to Phylloxera or Pierce’s Disease: For California

purposes, replacement grapevines may be depreciated using a recovery

period of five years instead of ten years.

This list is not intended to be all-inclusive of the federal and state differences.

For additional information, please refer to California’s R&TC.

Specific Line Instructions

Line 1 – California depreciation for assets and amortization for intangibles

placed in service during the current taxable year.

Complete column (a) through column (i) for each asset or group of assets

or property placed in service during the current taxable year. Enter the

column (f) totals on line 1(f). Enter the column (i) totals on line 1(i).

Line 2 – California depreciation for assets placed in service before

January 1, 2012.

Enter total California depreciation for assets placed in service prior to

January 1, 2012, taking into account any differences in asset basis or

differences in California and federal tax law.

Line 4 – California amortization for intangibles placed in service before

January 1, 2012.

Enter total California amortization for intangibles placed in service prior

to January 1, 2012, taking into account any differences in asset basis or

differences in California and federal tax law.

Assets with a Federal Basis Different from California Basis

Some assets placed in service on or after January 1, 1987, will have a

different adjusted basis for California purposes due to the credits claimed

or accelerated write-offs of the assets. Review the list of depreciation and

amortization items in the instructions for Schedule CA (540), California

Adjustments — Residents, and Schedule CA (540NR), California

Adjustments — Nonresidents or Part-Year Residents. If the LLC has any

other adjustments to make, get FTB Pub. 1001, Supplemental Guidelines to

California Adjustments, for more information.

Line 6 – Total Depreciation and Amortization

Add line 3 and line 5. Enter the total on line 6 and on Form 568, Schedule B,

line 17a.

If depreciation or amortization is from more than one trade or business

activity, or from more than one rental real estate activity, the LLC should

separately compute depreciation for each activity. Use the depreciation

computed on this form to identify the net income for each activity. Report

the net income from each activity on an attachment to Schedule K-1

(568), Member’s Share of Income, Deductions, Credits, etc., for purposes

of passive activity reporting requirements. Use California amounts

to determine the depreciation amount to enter on line 14 of federal

Form 8825, Rental Real Estate Income and Expenses of a Partnership or an

S Corporation.

Line 7

Enter the IRC Section 179 expense election amount from line 12 of the

following worksheet.

These limitations apply to the LLC and each member.

Election to Expense Certain Tangible Property (IRC Section 179) Worksheet

Follow the instructions on federal Form 4562, Depreciation and Amortization, for listed property.

1 Maximum dollar limitation ................................................................................. 1 $ 25,000

2 Total cost of IRC Section 179 property placed in service during the taxable year........................................ 2 __________________

3 Threshold cost of IRC Section 179 property placed in service during the taxable year ................................... 3 $200,000

4 Reduction in limitation. Subtract line 3 from line 2. If zero or less, enter -0- ........................................... 4 __________________

5 Dollar limitation for taxable year. Subtract line 4 from line 1. If zero or less, enter -0-.................................... 5 __________________

(a) (b) (c)

Description of property Cost Elected cost

6

7 Listed property. Use federal Form 4562, Part V, line 29. Make any adjustments for California law and basis differences .........7 __________________

8 Total elected cost of IRC Section 179 property. Add amounts in column (c), line 6 and line 7..............................8 __________________

9 Tentative deduction. Enter the smaller of line 5 or line 8 ..........................................................9 __________________

10 Carryover of disallowed deduction from 2011. See instructions for line 10 through line 13 on federal Form 4562 .............10 __________________

11 Income limitation. Enter the smaller of line 5 or the aggregate of the LLC’s items of income and expense described in

IRC Section 702(a) from any business actively conducted by the LLC, other than credits, tax-exempt IRC Section 179

expense deduction, and guaranteed payments under IRC Section 707(c) ............................................11 __________________

12 IRC Section 179 expense deduction. Add line 9 and line 10, but do not enter more than line 11. Enter on

Schedule K (568), line 12 and on form FTB 3885L, line 7 ........................................................12 __________________

13 Carryover of disallowed deduction to 2013. Add line 9 and line 10 and subtract line 12. Enter here and on line 8

of form FTB 3885L ......................................................................................13 __________________