Fillable Printable 2017 Form 592-F - Foreign Partner Or Member Annual Return

Fillable Printable 2017 Form 592-F - Foreign Partner Or Member Annual Return

2017 Form 592-F - Foreign Partner Or Member Annual Return

Sign

Here

Preparer’s

Use Only

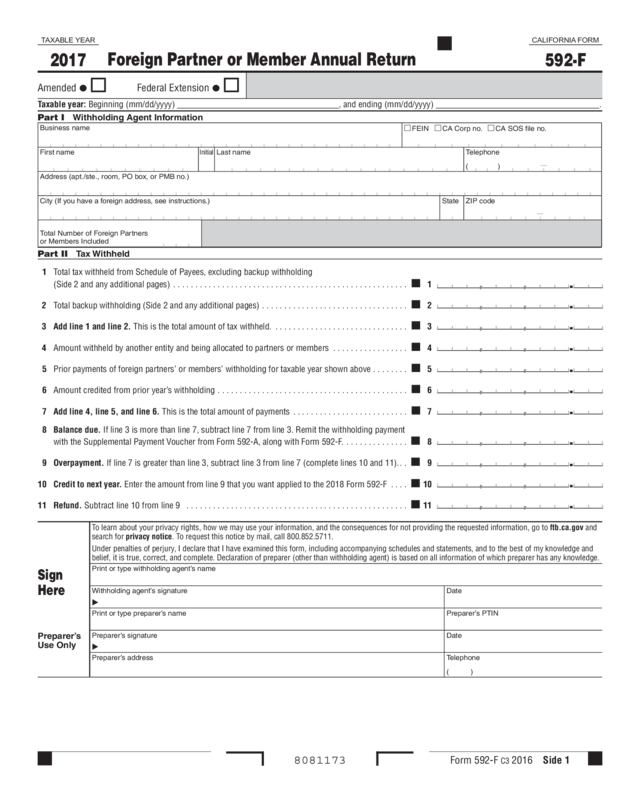

To learn about your privacy rights, how we may use your information, and the consequences for not providing the requested information, go to ftb.ca.gov and

search for privacy notice. To request this notice by mail, call 800.852.5711.

Under penalties of perjury, I declare that I have examined this form, including accompanying schedules and statements, and to the best of my knowledge and

belief, it is true, correct, and complete. Declaration of preparer (other than withholding agent) is based on all information of which preparer has any knowledge.

Print or type withholding agent’s name

Withholding agent’s signature Date

Print or type preparer’s name Preparer’s PTIN

Preparer’s signature Date

Preparer’s address Telephone

( )

Form 592-F C3 2016 Side 1

Foreign Partner or Member Annual Return

CALIFORNIA FORM

592-F

8081173

TAXABLE YEAR

2017

Taxable year: Beginning (mm/dd/yyyy) , and ending (mm/dd/yyyy) .

Part I

Withholding Agent Information

Business name

FEIN CA Corp no. CA SOS file no.

First name

Initial

Last name Telephone

( )

Address (apt./ste., room, PO box, or PMB no.)

City (If you have a foreign address, see instructions.) State ZIP code

Total Number of Foreign Partners

or Members Included

Part II Tax Withheld

1 Total tax withheld from Schedule of Payees, excluding backup withholding

(Side 2 and any additional pages) ..................................................... 1

2 Total backup withholding (Side 2 and any additional pages) ................................. 2

3 Add line 1 and line 2. This is the total amount of tax withheld. .............................. 3

4 Amount withheld by another entity and being allocated to partners or members ................. 4

5 Prior payments of foreign partners’ or members’ withholding for taxable year shown above . ....... 5

6 Amount credited from prior year’s withholding ........................................... 6

7 Add line 4, line 5, and line 6. This is the total amount of payments .......................... 7

8 Balance due. If line 3 is more than line 7, subtract line 7 from line 3. Remit the withholding payment

with the Supplemental Payment Voucher from Form 592-A, along with Form 592-F. .............. 8

9 Overpayment. If line 7 is greater than line 3, subtract line 3 from line 7 (complete lines 10 and 11)... 9

10 Credit to next year. Enter the amount from line 9 that you want applied to the 2018 Form 592-F .... 10

11 Refund. Subtract line 10 from line 9 .................................................. 11

.

,

,

.

,

,

.

,

,

.

,

,

.

,

,

.

,

,

.

,

,

.

,

,

.

,

,

.

,

,

.

,

,

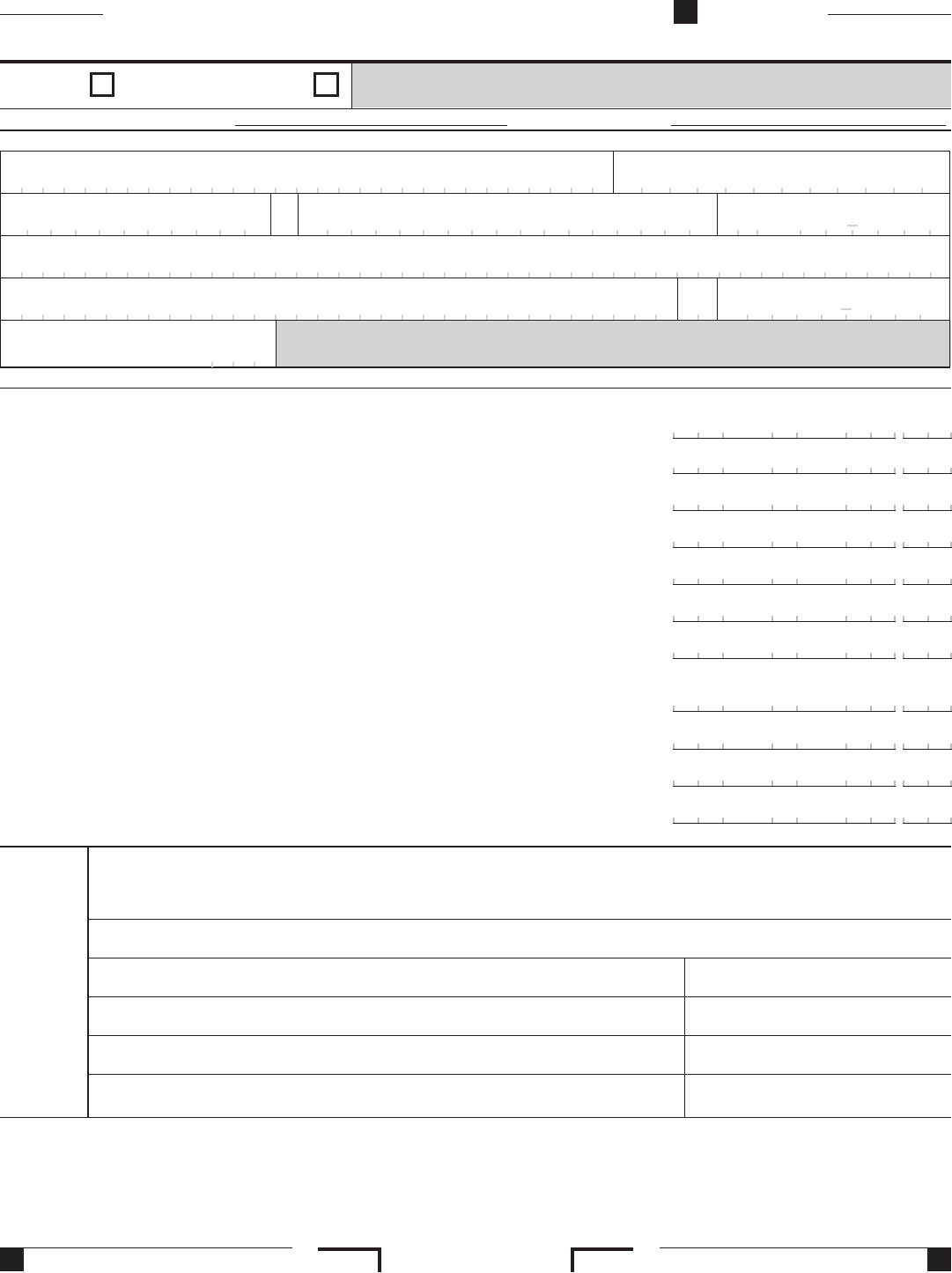

Amended I Federal Extension I

Side 2 Form 592-F C3 2016 8082173

.

,

,

Withholding Agent Name: ______________________________________ Withholding Agent TIN:__________________

Schedule of Payees (Enter business or individual name, not both.) PRINT CLEARLY

Business name

FEIN CA Corp no. CA SOS file no.

First name

Initial

Last name

SSN or ITIN

Address (apt./ste., room, PO box, or PMB no.)

City (If you have a foreign address, see instructions.) State ZIP code

Total income

If backup withholding, check the box.

Amount of tax withheld

Business name

FEIN CA Corp no. CA SOS file no.

First name

Initial

Last name

SSN or ITIN

Address (apt./ste., room, PO box, or PMB no.)

City (If you have a foreign address, see instructions.) State ZIP code

Total income

If backup withholding, check the box.

Amount of tax withheld

Business name

FEIN CA Corp no. CA SOS file no.

First name

Initial

Last name

SSN or ITIN

Address (apt./ste., room, PO box, or PMB no.)

City (If you have a foreign address, see instructions.) State ZIP code

Total income

If backup withholding, check the box.

Amount of tax withheld

Business name

FEIN CA Corp no. CA SOS file no.

First name

Initial

Last name

SSN or ITIN

Address (apt./ste., room, PO box, or PMB no.)

City (If you have a foreign address, see instructions.) State ZIP code

Total income

If backup withholding, check the box.

Amount of tax withheld

.

,

,

.

,

,

,

,

.

,

,

.

,

,

.

,

,

.

,

,

.

✔

Form 592-F Instructions 2016 Page 1

2017 Instructions for Form 592-F

Foreign Partner or Member Annual Return

What’s New

Due Date Change – Beginning on or after

January 1, 2016, for withholding on foreign

partners or members, the due date to file Form

592-F has changed from the 15th day of the 4th

month following the close of the partnership’s

or LLC’s taxable year to the 15th day of the 3rd

month following the close of the partnership’s or

LLC’s taxable year. See General Information B,

When and Where to File, for more information.

General Information

At the end of the taxable year, partnerships and

limited liability companies (LLCs) complete

Form 592-F, Foreign Partner or Member Annual

Return, to report the total withholding for the

year and to allocate the income and related

withholding to the foreign partners or members.

When filing Form 592-F with the Franchise Tax

Board (FTB), the withholding agent is not required

to submit to the FTB Form 592-B, Resident and

Nonresident Withholding Tax Statement, for each

partner or member. However, withholding agents

must provide the partners or members with

copies of Form 592-B.

For California withholding purposes:

y Nonresident includes all of the following:

y Individuals who are not residents of

California.

y Corporations not qualified through the

California Secretary of State (CA SOS)

to do business in California or having no

permanent place of business in California.

y Partnerships or LLCs with no permanent

place of business in California.

y Any trust without a resident grantor,

beneficiary, or trustee, or estates where

the decedent was not a California resident.

y Foreign refers to non-U.S.

Withholding on foreign partners or members

is remitted to the FTB using Form 592-A,

Payment Voucher for Foreign Partner or Member

Withholding. For more information on the

withholding requirements or to remit withholding

payments during the year, get Form 592-A.

A foreign partner may request to reduce or

eliminate withholding of California tax on

effectively connected taxable income from

California sources allocable to a foreign partner

(Federal Treasury Regulation 1.1446-6).

The foreign partner must first file federal

Form 8804-C, Certificate of Partner-Level Items

to Reduce Section 1446 Withholding, with the

partnership. Then the foreign partner must

sign and send Form 589, Nonresident Reduced

Withholding Request, to the FTB along with a

signed copy of federal Form 8804-C. The FTB will

review the request within 21 business days. If the

request is approved, the partnership should remit

the reduced withholding amount to the FTB along

with Form 592-A.

Backup Withholding – With certain limited

exceptions, payers that are required to withhold

and remit backup withholding to the Internal

Revenue Service (IRS) are also required to

withhold and remit to the FTB on income sourced

to California. The California backup withholding

rate is 7% of the payment. For California

purposes, dividends, interests, and any financial

institutions release of loan funds made in the

normal course of business are exempt from

backup withholding. For more information, go to

ftb.ca.gov and search for backup withholding.

If a payee has backup withholding, the payee

must contact the FTB to provide a valid

Taxpayer Identification Number (TIN) before

filing a tax return. The following are acceptable

TINs: social security number (SSN); individual

taxpayer identification number (ITIN); federal

employer identification number (FEIN); California

corporation number (CA Corp no.); or CA SOS file

number. Failure to provide a valid TIN will result in

the denial of the backup withholding credit.

Submitting Payments – Use the Supplemental

Payment Voucher from Form 592-A if you

have a final withholding payment to remit with

Form 592-F.

Penalty Increase – Beginning on or after

January 1, 2016, the penalties related to failure

to file information returns increased. See

General Information F, Interest and Penalties,

or get FTB 1150, Withhold at Source Penalty

Information, for more information.

A Purpose

Use Form 592-F to report the total withholding

for the year on foreign partners or members

under California Revenue and Taxation Code

Section 18666. Form 592-F is also used by

pass-through entities to pass-through withholding

credit to their foreign partners or members.

Do not use Form 592-F if:

y You are reporting withholding on domestic

nonresident partners or members. Use

Form 592, Resident and Nonresident

Withholding Statement.

y You are the buyer or real estate escrow

person withholding on the sale of real estate.

Use Form 593, Real Estate Withholding Tax

Statement, to report real estate withholding.

B When and Where to File

For withholding on foreign partners or members,

file Form 592-F, on or before the 15th day of the

3rd month following the close of the partnership’s

or LLC’s taxable year. If all the partners or

members are foreign, Form 592-F must be filed

on or before the 15th day of the 6th month after

the close of the partnership’s or LLC’s taxable year.

Mail Form 592-F, the Supplemental Payment

Voucher from Form 592-A, and payment to:

WITHHOLDING SERVICES AND

COMPLIANCE

FRANCHISE TAX BOARD

PO BOX 942867

SACRAMENTO CA 94267-0651

Important: If Form 592-F was filed electronically,

submit only your payment due and Form 592-A.

Record Keeping – The withholding agent retains

this form for a minimum of five years and must

provide it to the FTB upon request.

10-Day Notification – California follows federal

law, which requires that withholding agents notify

foreign payees within 10 days of any tax withheld.

For California withholding purposes, withholding

agents should make a similar notification to

nonresident payees. No particular form is required

for this notification, and it is commonly done on

the statement accompanying the distribution or

payment. However, the withholding agent may

choose to report the tax withheld to the payee on

a Form 592-B.

C Amending Form 592-F

If an error is discovered after Form 592-F has

been filed, an amended Form 592-F must be filed

to correct the error. Only withholding agents can

file amended forms.

Important: If you are amending a previously

submitted Form 592-F and need assistance,

call the Withholding Services and Compliance

telephone service at: 888.792.4900 or

916.845.4900.

To amend Form 592-F previously filed on the

correct taxable year form, but reporting incorrect

information:

y Complete a new Form 592-F with the correct

information. Use the same year form as

the original form and include all original

payees. Do not use negative numbers when

completing Form 592-F.

y Check the “Amended” box at the top of the form.

y Attach a letter to the back of the form

explaining what changes were made and why.

y Do not attach the original Form 592-F.

To amend a Form 592-F previously filed using an

incorrect taxable year form:

y Complete a new Form 592-F with the

withholding information using the correct year

form. Do not check the “Amended” box on the

top left corner of the form.

y Complete a second Form 592-F using the

same year form as originally filed. Check the

“Amended” box in the top left corner of the

form. Enter $0.00 as the amount withheld.

Mail the amended form(s) and letter(s) to the

address listed under General Information B, When

and Where to File.

D Federal Extension

Check the “Federal Extension” box at the top

of the form if you filed for an extension to file

federal Form 8804, Annual Return for Partnership

Withholding Tax (Section 1446).

Caution: An extension to file is not an extension

to pay. The final withholding payment is due on

or before the original due date for Form 592-F

regardless of an extension to file.

E Electronic Filing

Requirements

When the number of payees on Form 592-F is

250 or more, Form 592-F must be filed with the

FTB electronically, using the FTB’s Secure Web

Internet File Transfer (SWIFT), instead of paper.

However, withholding agents must continue to

provide payees with copies of Form 592-B.

For electronic filing, submit your file using the

SWIFT process as outlined in FTB Pub. 923,

SWIFT Guide for Resident, Nonresident, and Real

Estate Withholding.

Page 2 Form 592-F Instructions 2016

For the required file format and record layout

for electronic filing, get FTB Pub. 1023S,

Resident and Nonresident Withholding Electronic

Submission Requirements.

If you are the preparer for more than one

withholding agent, provide a separate electronic

file for each withholding agent.

Electronic signatures shall be considered as valid

as the originals.

F Interest and Penalties

Interest on late payments is computed from the due

date of the withholding to the date paid. Failure to

withhold may result in the withholding agent being

personally liable for the amount of tax that was

required to be withheld, plus interest and penalties,

unless the failure was due to reasonable cause.

A penalty will be assessed for failure to file

complete, correct, and timely information returns

(Form 592-F Schedule of Payees) with the FTB.

The penalty is calculated per payee:

y $30 if filed 1 to 30 days after the due date.

y $60 if filed 31 days to 6 months after the due

date.

y $100 if filed more than 6 months after the due

date.

For more information, get FTB 1150, Withhold at

Source Penalty Information.

Specific Instructions

If completing Form 592-F by hand, enter all

information requested using black or blue ink.

Taxable Year

y Enter the beginning and ending dates for the

partnership’s or LLC’s taxable year.

y Make sure the year in the upper left corner

of the form matches the ending date of the

taxable year.

Private Mail Box (PMB) – Include the PMB in

the address field. Write “PMB” first, then the box

number. Example: 111 Main Street PMB 123.

Foreign Address – Follow the country’s practice

for entering the city, county, province, state,

country, and postal code, as applicable, in

the appropriate boxes. Do not abbreviate the

country’s name.

Part I Withholding Agent

Information

Enter withholding agent information, check the

appropriate box and enter the TIN. If your entity

was withheld upon by another entity because

you are a foreign (non-U.S.) partner or member

of that entity and you are passing through the

withholding credit to your foreign (non U.S.)

partners, members or beneficiaries, enter your

entity’s name, TIN, and address in the business

name area.

Do not enter the name or TIN of the entity which

originally withheld payments from you.

Enter the total number of foreign partners or

members included on the Schedule of Payees.

Part II Tax Withheld

Line 1 – Enter the total withholding, excluding

backup withholding, from the Schedule of Payees

on Side 2 and from any additional pages of the

Schedule of Payees.

Line 2 – Enter the total backup withholding

from the Schedule of Payees on Side 2 and any

additional pages of the Schedule of Payees.

Line 3 – Add line 1 and line 2. This is the total

amount of tax withheld.

Line 4 – Enter the amount withheld by another

entity and being allocated to your foreign partners

or members. If any of the amount withheld by the

other entity is to be used against the tax owed by

your entity, do not include that amount in line 4.

Attach a note to Form 592-F explaining how much

of the credit will be used to offset your tax due.

All additional amounts withheld by another entity

must be allocated to your partners or members

and may not be refunded on Form 592-F.

Line 5 – Enter prior payments for the taxable year

shown above from Forms 592-A.

Line 6 – Enter the amount of foreign partner

or member credit carried over from the prior

withholding year.

Line 8 – If line 3 is more than line 7, subtract

line 7 from line 3. Remit the withholding payment

using the Supplemental Payment Voucher from

Form 592-A, along with Form 592-F.

Line 9 – If line 7 is more than line 3, subtract

line 3 from line 7 (complete lines 10 and 11).

Line 10 – Enter the amount of your overpayment

on line 9 that you want to credit to the 2018

Form 592-F.

Schedule of Payees Instructions

Enter all the applicable information for each payee

you report as having nonresident or backup

withholding to ensure each payee’s withholding

payment is applied timely and properly.

Do not include payees who have zero withholding

unless you are amending Form 592-F to exclude a

payee originally reported in error.

Do not leave a blank payee box unless you are at

the end of the Schedule of Payees.

You must use the Schedule of Payees on Side 2

of Form 592-F to report all payees.

If you withheld tax on multiple payees for the

taxable year, complete and include additional

copies of the Schedule of Payees from Side 2 of

Form 592-F, as necessary. Include the withholding

agent’s name and TIN at the top of each additional

page.

Do not attach your own schedules to this form.

We only accept and process additional payees

reported on the Schedule of Payees from Side 2

of Form 592-F.

Business or Individual Name, TIN, and Address

Enter only business or individual information

for each payee, not both, check the appropriate

box and enter the TIN. Do not enter the business

name of your entity as a payee.

If the payee is a grantor trust, enter the grantor’s

individual name and TIN. Do not enter the name

of the trust or trustee information. (For tax

purposes, grantor trusts are transparent. The

individual grantor must report the income and

claim the withholding on the individual’s California

tax returns.)

If the payee is a non-grantor trust, enter the

name of the trust and the trust’s FEIN. Do not

enter trustee information

. If the non-grantor

trust has applied for a FEIN and it has not yet

been received, or they have not applied for a

FEIN, leave the identification number field blank.

After the FEIN is received, contact the FTB at

888.792.4900.

Total Income – Enter the total income subject to

withholding.

Backup Withholding – If the payee is subject

to backup withholding, check this box. Attach

the withholding statement that enables you to

determine the specific payment to each recipient

as required by the IRS.

Amount of Tax Withheld – Enter the amount of

tax withheld. Determine the California source

taxable income allocable for the partner or

member, then multiply by the applicable tax rate:

Income amount X Maximum tax rate for the

partner or member.

Tax Rates

12.3% Non-corporate maximum tax rate

8.84% Corporate maximum tax rate

10.84% Bank and financial institution maximum

tax rate

Additional Information

Website: For more information go to

ftb.ca.gov and search for nonwage.

MyFTB offers secure online tax

account information and services.

For more information and to

register, go to ftb.ca.gov and search

for myftb.

Telephone: 888.792.4900 or 916.845.4900,

Withholding Services and

Compliance phone service

Fax: 916.845.9512

Mail: WITHHOLDING SERVICES AND

COMPLIANCE MS F182

FRANCHISE TAX BOARD

PO BOX 942867

SACRAMENTO CA 94267-0651

For questions unrelated to withholding, or to

download, view, and print California tax forms and

publications, or to access the TTY/TDD numbers,

see the information below.

Internet and Telephone Assistance

Website: ftb.ca.gov

Telephone: 800.852.5711 from within the

United States

916.845.6500 from outside the

United States

TTY/TDD: 800.822.6268 for persons with

hearing or speech impairments

Asistencia Por Internet y Teléfono

Sitio web: ftb.ca.gov

Teléfono: 800.852.5711 dentro de los

Estados Unidos

916.845.6500 fuera de los

Estados Unidos

TTY/TDD: 800.822.6268 para personas con

discapacidades auditivas o del

habla