Fillable Printable Cost / Benefit Analysis - Community Facility Partner Capital Grant Program

Fillable Printable Cost / Benefit Analysis - Community Facility Partner Capital Grant Program

Cost / Benefit Analysis - Community Facility Partner Capital Grant Program

Cost / Benefit Analysis

To be included with CFPCG application as an attachment

This is a sample of a Cost / Benefit Analysis – other formats may be submitted.

Purpose of the Cost / Benefit Analysis:

The reason for writing the Cost / Benefit Analysis is to provide an evaluation of the costs and

benefits associated with the project that are easily understood and compare the initial and on-going

expenditures to the expected financial and non-financial benefits.

Checklist for Cost/Benefit Analysis Section

1.Have all quantitative costs and benefits been identified?

2.Have all qualitative costs and benefits been identified?

3.Is the time frame appropriate considering the expected life span of the project?

4.Can any of the non-financial items be converted to financial items?

5.Are all the assumptions clearly identified?

6.Have all common/general assumptions been applied consistently to each alternative?

7.Have assumptions been reviewed to identify the sensitivity of their estimate on the impact of

the results?

8.Have benchmarks, other organization’s experience, industry data been used to validate

costs / benefits?

A. Quantitative Analysis – Financial Cost & Benefit:

Description:

Full Cost Analysis:

Where possible, all costs and expected benefits resulting from this opportunity should be analyzed.

This methodology provides a total cost picture and is much more informative than an incremental

approach. Any detailed worksheets should be attached as an appendix.

Timeframe:

Identify an appropriate project timeframe over which both the cost and benefits will be analyzed.

Timeframe should be appropriate to the expected lifecycle of the project, from incurring costs to

achieving the anticipated benefits.

Costs:

Identify all relevant costs incurred by all stakeholders over the chosen project timeframe:

Direct costs (fixed and variable);

Indirect costs;

Initial costs;

On-going costs including a Annual Capital Reserve Fund of 2% of the capital costs; and,

Capital costs.

Consideration should be given to:

When the costs will be incurred;

Who will incur the costs; and,

Certainty of costs.

Benefits:

Identify all quantifiable benefits related to all stakeholders, over the chosen project timeframe.

Consideration should be given to:

When the benefits will be achieved;

Who will be the recipient of the benefits; and,

Certainty of benefits.

The cost / benefit analysis considers whether net marginal benefits are greater than net marginal

costs.

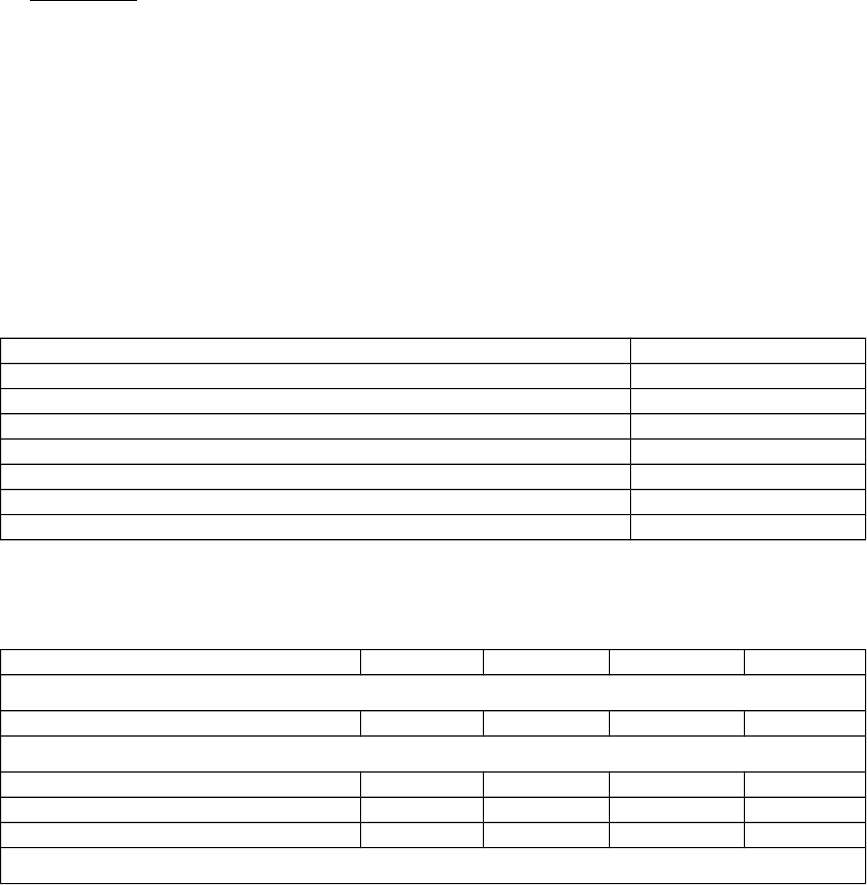

Sample of a Summary Cost Benefit Template:

Summary of Quantitative Cost/Benefit

Present Value of Total Benefits: $

Present Value of Total Costs: $

Net Present Value of Project $

Sample Costing Template:

Quantitative Analysis – Viable Year 0 Year 1 Year 2 Year 3

Benefits:

Revenue $ $ $ $

Costs:

Analysis $ $ $ $

Design $ $ $ $

Implementation $ $ $ $

Ongoing Operational Costs:

Human Resources $ $ $ $

Administration $ $ $ $

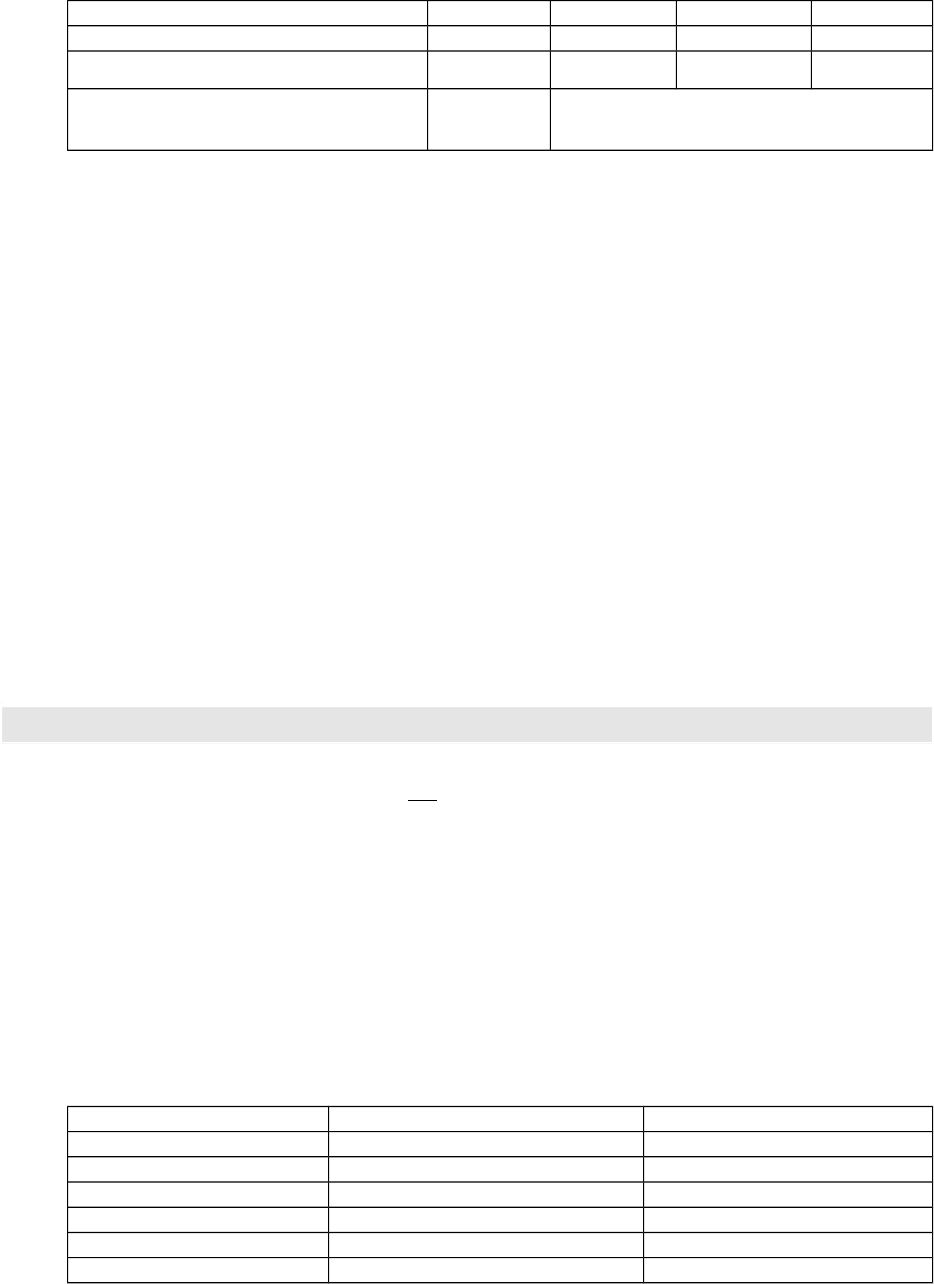

Net Benefit or Cost of Viable $ $ $ $

Net Present Value

(xx% Discount Rate) $

Analysis:

A “Net Present Value” calculation is used to account for the fact that $1 today is not worth the

same as $1 five years from now, due to inflation and interest rates. The use of a “Net

Present Value” calculation should be used to take into account the time value of money, for

regardless of whether the full or incremental cost approach is used.

If there are some assumptions that have a significant impact on the cost or benefit, a

sensitivity analysis should be presented. Contingency allowances or interest rate premiums

should be used to account for differences in certainty / risk. The cost / benefit analysis

should be reviewed for reasonableness through the use of benchmarks, other organization’s

experience, industry data, etc. This would include the use of a public sector comparator for

public-private partnership projects.

B. Qualitative Analysis – Non-Financial Benefits & Costs:

Some of the costs and benefits may not be quantifiable (difficult to attach a dollar value). For

example, non-quantifiable benefits may be: increased customer satisfaction or increased

staff morale. Non-quantifiable costs may be: reduced corporate image or adverse public

perception. Where reasonable, these should be translated into quantifiable benefits (i.e.,

increased staff morale, may lead to high productivity, which may lead to less over-time).

However, the non-quantifiable cost / benefits that cannot be translated into quantifiable

cost/benefits should be summarized in the following manner:

For each Viable Alternative

Qualitative Summary Description Stakeholder(s) Impacted

Benefits:

Benefit 1 Description of benefit 1

Benefit 2 Description of benefit 2

Costs:

Cost 1 Description of Cost 1

Cost 2 Description of Cost 2

Cost 2 Description of Cost 2

C. Assumptions

All assumptions used to determine, both quantitative and qualitative, costs and benefits

should be clearly documented. This would include general assumptions as well as

assumptions specific to each alternative.