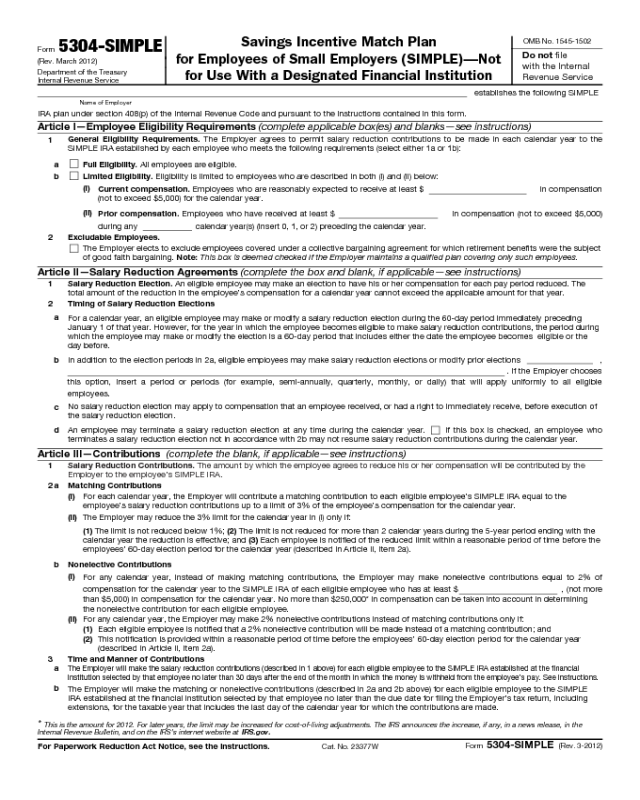

Form 5304-SIMPLE (Rev. 3-2012)

Page 5

the reduction in the employee’s

compensation cannot exceed the

applicable amount for any calendar year.

The applicable amount is $11,500 for 2012.

After 2012, the $11,500 amount may be

increased for cost-of-living adjustments. In

the case of an eligible employee who is 50

or older by the end of the calendar year,

the above limitation is increased by $2,500

for 2012. After 2012, the $2,500 amount

may be increased for cost-of-living

adjustments.

Timing of Salary Reduction

Elections

For any calendar year, an eligible employee

may make or modify a salary reduction

election during the 60-day period

immediately preceding January 1 of that

year. However, for the year in which the

employee becomes eligible to make salary

reduction contributions, the period during

which the employee may make or modify

the election is a 60-day period that

includes either the date the employee

becomes eligible or the day before.

You can extend the 60-day election

periods to provide additional opportunities

for eligible employees to make or modify

salary reduction elections using the blank

in Article II, item 2b. For example, you can

provide that eligible employees may make

new salary reduction elections or modify

prior elections for any calendar quarter

during the 30 days before that quarter.

You may use the Model Salary Reduction

Agreement on page 3 to enable eligible

employees to make or modify salary

reduction elections.

Employees must be permitted to

terminate their salary reduction elections at

any time. They may resume salary

reduction contributions for the year if

permitted under Article II, item 2b.

However, by checking the box in Article II,

item 2d, you may prohibit an employee

who terminates a salary reduction election

outside the normal election cycle from

resuming salary reduction contributions

during the remainder of the calendar year.

Contributions (Article III)

Only contributions described below may be

made to this SIMPLE IRA plan. No

additional contributions may be made.

Salary Reduction Contributions

As indicated in Article III, item 1, salary

reduction contributions consist of the

amount by which the employee agrees to

reduce his or her compensation. You must

contribute the salary reduction

contributions to the financial institution

selected by each eligible employee.

Matching Contributions

In general, you must contribute a matching

contribution to each eligible employee’s

SIMPLE IRA equal to the employee’s salary

reduction contributions. This matching

contribution cannot exceed 3% of the

employee’s compensation. See Definition

of Compensation, below.

You may reduce this 3% limit to a lower

percentage, but not lower than 1%. You

cannot lower the 3% limit for more than 2

calendar years out of the 5-year period

ending with the calendar year the reduction

is effective.

Note. If any year in the 5-year period

described above is a year before you first

established any SIMPLE IRA plan, you will

be treated as making a 3% matching

contribution for that year for purposes of

determining when you may reduce the

employer matching contribution.

To elect this option, you must notify the

employees of the reduced limit within a

reasonable period of time before the

applicable 60-day election periods for the

year. See Timing of Salary Reduction

Elections above.

Nonelective Contributions

Instead of making a matching contribution,

you may, for any year, make a nonelective

contribution equal to 2% of compensation

for each eligible employee who has at least

$5,000 in compensation for the year.

Nonelective contributions may not be

based on more than $250,000* of

compensation.

To elect to make nonelective

contributions, you must notify employees

within a reasonable period of time before

the applicable 60-day election periods for

such year. See Timing of Salary Reduction

Elections above.

Note. Insert “$5,000” in Article III, item

2b(i) to impose the $5,000 compensation

requirement. You may expand the group of

employees who are eligible for nonelective

contributions by inserting a compensation

amount lower than $5,000.

Effective Date (Article VII)

Insert in Article VII the date you want the

provisions of the SIMPLE IRA plan to

become effective. You must insert January

1 of the applicable year unless this is the

first year for which you are adopting any

SIMPLE IRA plan. If this is the first year for

which you are adopting a SIMPLE IRA

plan, you may insert any date between

January 1 and October 1, inclusive of the

applicable year.

Additional Information

Timing of Salary Reduction

Contributions

The employer must make the salary

reduction contributions to the financial

institution selected by each eligible

employee for his or her SIMPLE IRA no

later than the 30th day of the month

following the month in which the amounts

would otherwise have been payable to the

employee in cash.

The Department of Labor has indicated

that most SIMPLE IRA plans are also

subject to Title I of the Employee

Retirement Income Security Act of 1974

(ERISA). Under Department of Labor

regulations at 29 CFR 2510.3-102, salary

reduction contributions must be made to

each participant’s SIMPLE IRA as of the

earliest date on which those contributions

can reasonably be segregated from the

employer’s general assets, but in no event

later than the 30-day deadline described

previously.

Definition of Compensation

“Compensation” means the amount

described in section 6051(a)(3) (wages,

tips, and other compensation from the

employer subject to federal income tax

withholding under section 3401(a)), and

amounts paid for domestic service in a

private home, local college club, or local

chapter of a college fraternity or sorority.

Usually, this is the amount shown in box 1

of Form W-2, Wage and Tax Statement.

For further information, see Pub. 15,

(Circular E), Employer’s Tax Guide.

Compensation also includes the salary

reduction contributions made under this

plan, and, if applicable, compensation

deferred under a section 457 plan. In

determining an employee’s compensation

for prior years, the employee’s elective

deferrals under a section 401(k) plan, a

SARSEP, or a section 403(b) annuity

contract are also included in the

employee’s compensation.

For self-employed individuals,

compensation means the net earnings

from self-employment determined under

section 1402(a), without regard to section

1402(c)(6), prior to subtracting any

contributions made pursuant to this

SIMPLE IRA plan on behalf of the

individual.

Employee Notification

You must notify each eligible employee

prior to the employee’s 60-day election

period described above that he or she can

make or change salary reduction elections

and select the financial institution that will

serve as the trustee, custodian, or

*This is the amount for 2012. For later years, the limit may be increased for cost-of-living adjustments. The IRS announces the increase, if any,

in a news release, in the Internal Revenue Bulletin, and on the IRS’s website at IRS.gov.