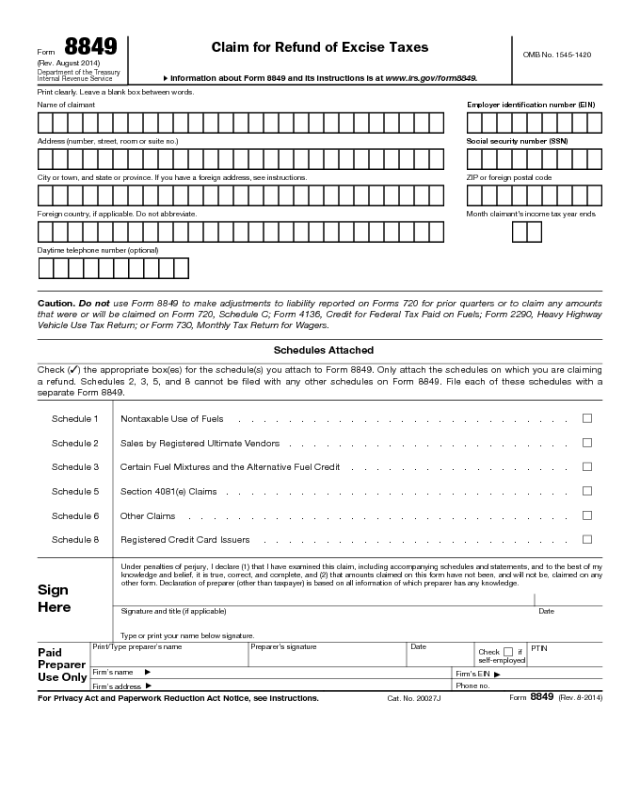

Form 8849

Form 8849

(Rev. August 2014)

Department of the Treasury

Internal Revenue Service

Claim for Refund of Excise Taxes

▶ Information about Form 8849 and its instructions is at www.irs.gov/form8849.

OMB No. 1545-1420

Print clearly. Leave a blank box between words.

Name of claimant Employer identification number (EIN)

Address (number, street, room or suite no.) Social security number (SSN)

City or town, and state or province. If you have a foreign address, see instructions. ZIP or foreign postal code

Foreign country, if applicable. Do not abbreviate. Month claimant’s income tax year ends

Daytime telephone number (optional)

Caution. Do not use Form 8849 to make adjustments to liability reported on Forms 720 for prior quarters or to claim any amounts

that were or will be claimed on Form 720, Schedule C; Form 4136, Credit for Federal Tax Paid on Fuels; Form 2290, Heavy Highway

Vehicle Use Tax Return; or Form 730, Monthly Tax Return for Wagers.

Schedules Attached

Check (✓) the appropriate box(es) for the schedule(s) you attach to Form 8849. Only attach the schedules on which you are claiming

a refund. Schedules 2, 3, 5, and 8 cannot be filed with any other schedules on Form 8849. File each of these schedules with a

separate Form 8849.

Schedule 1

Nontaxable Use of Fuels . . . . . . . . . . . . . . . . . . . . . . . . . . .

Schedule 2 Sales by Registered Ultimate Vendors . . . . . . . . . . . . . . . . . . . . . . .

Schedule 3 Certain Fuel Mixtures and the Alternative Fuel Credit . . . . . . . . . . . . . . . . . .

Schedule 5 Section 4081(e) Claims . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Schedule 6 Other Claims . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Schedule 8 Registered Credit Card Issuers . . . . . . . . . . . . . . . . . . . . . . . . .

Sign

Here

Under penalties of perjury, I declare (1) that I have examined this claim, including accompanying schedules and statements, and to the best of my

knowledge and belief, it is true, correct, and complete, and (2) that amounts claimed on this form have not been, and will not be, claimed on any

other form. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

Signature and title (if applicable)

Date

Type or print your name below signature.

Paid

Preparer

Use Only

Print/Type preparer’s name Preparer’s signature Date

Check if

self-employed

PTIN

Firm’s name

▶

Firm’s EIN ▶

Firm’s address

▶

Phone no.

For Privacy Act and Paperwork Reduction Act Notice, see instructions.

Cat. No. 20027J

Form 8849 (Rev. 8-2014)

Form 8849 (Rev. 8-2014)

Page 2

Section references are to the Internal Revenue Code.

Future Developments

For the latest information about developments related to

Form 8849 and its instructions or separate schedules,

such as legislation enacted after they were published, go

to www.irs.gov/form8849.

What’s New

Changes are discussed under What’s New in the

instructions for each schedule.

Reminders

• You can electronically file Form 8849 through any

electronic return originator (ERO), transmitter, and/or

intermediate service provider (ISP) participating in the

IRS e-file program for excise taxes. For more information

on e-file and its availability, visit the IRS website at

www.irs.gov/efile.

• Qualified subchapter S subsidiaries (QSubs) and

eligible single-owner disregarded entities are treated as

separate entities for certain excise tax and reporting

purposes. QSubs and eligible single-owner disregarded

entities must pay and report certain excise taxes (other

than IRS Nos. 31, 51, and 117), register for certain excise

tax activities, and claim certain refunds, credits, and

payments under the entity’s employer identification

number (EIN). These actions cannot take place under the

owner’s taxpayer identification number (TIN). Some

QSubs and disregarded entities may already have an

EIN. However, if you are unsure, call the IRS business

and specialty tax line at 1-800-829-4933.

Generally, QSubs and eligible single-owner disregarded

entities will continue to be treated as disregarded entities

for other federal tax purposes (other than employment

taxes). Thus, taxpayers filing Form 4136, Credit for

Federal Tax Paid on Fuels, with Form 1040, Individual

Income Tax Return, can use the owner’s TIN. For specific

information, see Treasury Decision (T.D.) 9356. You can

find T.D. 9356 on page 675 of Internal Revenue Bulletin

2007-39 at www.irs.gov/pub/irs-irbs/irb07-39.pdf.

General Instructions

Purpose of Form

Use Form 8849 to claim a refund of excise taxes. Attach

Schedules 1, 2, 3, 5, and 8 to claim certain fuel related

refunds such as nontaxable uses (or sales) of fuels.

Attach Schedule 6 for claims not reportable on

Schedules 1, 2, 3, 5, and 8, including refunds of excise

taxes reported on:

• Form 720, Quarterly Federal Excise Tax Return;

• Form 730, Monthly Tax Return for Wagers;

• Form 11-C, Occupational Tax and Registration Return

for Wagering; and

• Form 2290, Heavy Highway Vehicle Use Tax Return.

Filers only need to complete and attach to Form 8849 the

applicable schedules.

Do not use Form 8849:

• To make adjustments to liability reported on Forms

720 filed for prior quarters; instead, use Form 720X,

Amended Quarterly Federal Excise Tax Return.

• To claim amounts that you took or will take as a credit

on Form 720, Schedule C; Form 730; Form 2290; or Form

4136.

Additional Information

Pub. 510, Excise Taxes, has information on fuel tax

credits, refunds, nontaxable uses, and the definitions of

terms such as ultimate vendor.

Pub. 225, Farmer’s Tax Guide, has information on

credits and refunds for the federal excise tax on fuels

applicable to farmers.

You may also call the IRS business and specialty tax

line at 1-800-829-4933 with your excise tax questions.

Where To File

• For Schedules 1 and 6, send Form 8849 to:

Department of the Treasury

Internal Revenue Service

Cincinnati, OH 45999-0002

• For Schedules 2, 3, 5, and 8, send Form 8849 to:

Internal Revenue Service

P.O. Box 312

Covington, KY 41012-0312

Caution. Private delivery services designated by the IRS

cannot deliver items to P.O. boxes. You must use the

U.S. Postal Service to mail any item to an IRS P.O. box

address. For details on designated private delivery

services, see Pub. 509, Tax Calendars.

Including the Refund in Income

Include any refund of excise taxes in your gross income if

you claimed the amount of the tax as an expense

deduction that reduced your income tax liability.

Cash method. If you use the cash method and file a

claim for refund, include the refund amount in your gross

income for the tax year in which you receive the refund.

Accrual method. If you use an accrual method, include

the amount of refund in gross income for the tax year in

which you used the fuels or sold the fuels if you are a

registered ultimate vendor or registered credit card issuer.

Form 8849 (Rev. 8-2014)

Page 3

Specific Instructions

Name and Address

Print the information in the spaces provided. Begin

printing in the first box on the left. Leave a blank box

between each name and word. If there are not enough

boxes, print as many letters as there are boxes. Use

hyphens for compound names; use one box for each

hyphen.

P.O. box. If your post office does not deliver mail to your

street address and you have a P.O. box, show your box

number instead of your street address.

Foreign address. Follow the country’s practice for

entering the postal code.

EIN and SSN

Enter your EIN in the boxes provided. If you are not

required to have an EIN, enter your SSN. An incorrect or

missing number will delay processing your claim.

Month Income Tax Year Ends

Enter the month your income tax year ends. For

example, if your income tax year ends in December,

enter “12” in the boxes. If your year ends in March, enter

“03.”

Signature

Form 8849 must be signed by a person with authority to

sign this form for the claimant.

Note. Your refund will be delayed or Form 8849 will be

returned to you if you do not follow the required

procedures or do not provide all the required information.

See the instructions for each schedule.

Complete each schedule and attach all information

requested for each claim you make, generally including

the following:

• EIN (or SSN) on each attached schedule,

• Period of the claim,

• Item number (when requested) from the Type of Use

Table below,

• Rate (as needed; see the separate schedule

instructions),

• Number of gallons, and

• Amount of refund.

If you need more space for any line on a schedule (for

example, you have more than one type of use) prepare a

separate sheet with the same information. Include your

name and EIN (or SSN) on each sheet you attach.

Type of Use Table

The following table lists the nontaxable uses of fuels. You

must enter the number from the table in the Type of Use

column as required on Schedules 1 and 2.

No. Type of Use

1 On a farm for farming purposes

2

Off-highway business use (for business use other than in

a highway vehicle registered or required to be registered

for highway use) (other than use in mobile machinery)

3 Export

4 In a boat engaged in commercial fishing

5 In certain intercity and local buses

6 In a qualified local bus

7 In a bus transporting students and employees of

schools (school buses)

8 For diesel fuel and kerosene (other than kerosene used

in aviation) used other than as a fuel in the propulsion

engine of a train or diesel-powered highway vehicle

(but not off-highway business use)

9 In foreign trade

10 Certain helicopter and fixed-wing aircraft uses

11 Exclusive use by a qualified blood collector

organization

12 In a highway vehicle owned by the United States that

is not used on a highway

13 Exclusive use by a nonprofit educational

organization

14 Exclusive use by a state, political subdivision of a

state, or the District of Columbia

15 In an aircraft or vehicle owned by an aircraft

museum

16 In military aircraft

Types of Use 13 and 14. Generally, claims for sales of

diesel fuel, kerosene, kerosene for use in aviation,

gasoline, or aviation gasoline for the exclusive use of a

state or local government (and nonprofit educational

organization for gasoline or aviation gasoline) must be

made following the order below.

1. By the registered credit card issuer if the state or

local government (or nonprofit educational organization if

applicable) used a credit card and the credit card issuer

meets the requirements discussed in the Schedule 8

(Form 8849) instructions.

2. By the registered ultimate vendor if the ultimate

purchaser did not use a credit card and the ultimate

vendor meets the requirements discussed in the

Schedule 2 (Form 8849) instructions.

3. By the ultimate purchaser if the ultimate purchaser

used a credit card and neither the registered credit card

issuer nor the registered ultimate vendor is eligible to

make the claim.

For additional requirements, see Pub. 510.

Form 8849 (Rev. 8-2014)

Page 4

Additional Information for Schedules 1, 2,

and 3

Annual Claims

If a claim was not made for any gallons during the

income tax year on Form 8849, an annual claim may be

made. Generally, an annual claim is made on Form 4136

for the income tax year during which the fuel was:

• Used by the ultimate purchaser;

• Sold by the registered ultimate vendor;

• Purchased with a credit card issued by a registered

credit card issuer (except for gasoline and aviation

gasoline);

• Used to produce biodiesel or renewable diesel

mixtures, and alternative fuel mixtures; or

• Used in mobile machinery.

The following claimants must use Form 8849 (Schedule

1) for annual claims.

1. The United States.

2. A state, political subdivision of a state, or the District

of Columbia (but see Types of Use 13 and 14, earlier).

3. Organizations exempt from income tax under section

501(a) (provided that the organization is not required to

file Form 990-T, Exempt Organization Business Income

Tax Return, for that taxable year).

For claimants included in 1–3 above, the annual Form

8849 for fuel used during the taxable year must be filed

within the 3 years following the close of the taxable year.

For these claimants, the taxable year is based on the

calendar year or fiscal year it regularly uses to keep its

books.

Although not an annual claim, the above claimants

should use Schedule 3 (Form 8849) to claim the

alternative fuel credit.

Note. Gasoline used by the above claimants on a farm

for farming purposes (type of use 1) is an allowable use

on Schedule 1 (Form 8849), line 1.

Paid Preparer Use Only

A paid preparer must sign Form 8849 and provide the

information in the Paid Preparer Use Only section at the

end of the form if the preparer was paid to prepare the

form and is not an employee of the filing entity. The

preparer must give you a copy of the form in addition to

the copy to be filed with the IRS.

If you are a paid preparer, enter your Preparer Tax

Identification Number (PTIN) in the space provided.

Include your complete address. If you work for a firm, you

also must enter the firm's name and the EIN of the firm.

However, you cannot use the PTIN of the tax preparation

firm in place of your PTIN.

You can apply for a PTIN online or by filing Form W-12,

IRS Paid Preparer Tax Identification Number (PTIN)

Application and Renewal. For more information about

applying for a PTIN online, visit the IRS website at

www.irs.gov/ptin.

Privacy Act and Paperwork Reduction Act Notice. We

ask for the information on the form and schedules to carry

out the Internal Revenue laws of the United States. We need

it to figure and collect the right amount of tax. Subtitle F,

Procedure and Administration, of the Internal Revenue Code

allows refunds of taxes imposed under Subtitle D,

Miscellaneous Excise Taxes. The form and schedules are

used to determine the amount of the refund that is due to

you. Section 6109 requires you to provide your taxpayer

identification number (SSN or EIN). Routine uses of tax

information include giving it to the Department of Justice for

civil and criminal litigation, and cities, states, and the District

of Columbia for use in administering their tax laws. We may

also disclose this information to other countries under a tax

treaty, to federal and state agencies to enforce federal

nontax criminal laws, or to federal law enforcement

agencies and intelligence agencies to combat terrorism.

You are not required to claim a refund; however, if you

do so you must provide the information requested on this

form. If you fail to provide all requested information in a

timely manner, we may be unable to process this claim. If

you provide false or fraudulent information, you may be

liable for penalties.

You are not required to provide the information

requested on a form that is subject to the Paperwork

Reduction Act unless the form displays a valid OMB

control number. Books or records relating to a form or its

instructions must be retained as long as their contents

may become material in the administration of any Internal

Revenue law. Generally, tax returns and return

information are confidential, as required by section 6103.

The time needed to complete and file the form and

schedules will vary depending on individual

circumstances. The estimated average times are:

Record-

keeping

Learning

about the law

or the form

Preparing, copying,

assembling, and

sending the form

to the IRS

Form 8849 3 hr., 21 min. 24 min. 28 min.

Schedule 1 20 hr., 19 min. 6 min. 25 min.

Schedule 2 11 hr., 43 min. 11 min.

Schedule 3 7 hr., 10 min. 6 min. 13 min.

Schedule 5 3 hr., 35 min. 6 min. 9 min.

Schedule 6 2 hr., 9 min. 24 min. 27 min.

Schedule 8 5 hr., 15 min. 5 min.

If you have comments concerning the accuracy of

these time estimates or suggestions for making the form

and schedules simpler, we would be happy to hear from

you. You can send your comments from

www.irs.gov/formspubs. Click on “More Information” and

then on “Give us feedback.” You can also write to:

Internal Revenue Service

Tax Forms and Publications

1111 Constitution Ave. NW, IR-6526

Washington, DC 20224

Do not send Form 8849 to this address. Instead, see

Where To File, earlier.