Fillable Printable Form 941Sb

Fillable Printable Form 941Sb

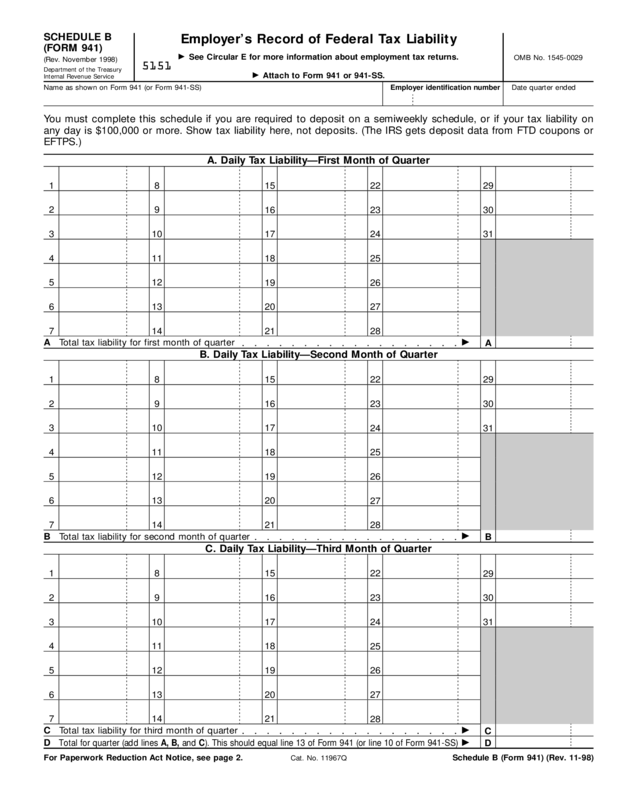

Form 941Sb

Cat. No. 11967Q

OMB No. 1545-0029

Employer’s Record of Federal Tax Liability

(Rev. November 1998)

©

See Circular E for more information about employment tax returns.

Department of the Treasury

Internal Revenue Service

©

Attach to Form 941 or 941-SS.

Name as shown on Form 941 (or Form 941-SS) Employer identification number Date quarter ended

You must complete this schedule if you are required to deposit on a semiweekly schedule, or if your tax liability on

any day is $100,000 or more. Show tax liability here, not deposits. (The IRS gets deposit data from FTD coupons or

EFTPS.)

A. Daily Tax Liability—First Month of Quarter

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

Total tax liability for first month of quarter

©

B. Daily Tax Liability—Second Month of Quarter

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

Total tax liability for second month of quarter

©

C. Daily Tax Liability—Third Month of Quarter

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

Total tax liability for third month of quarter

©

Total for quarter (add lines A, B, and C). This should equal line 13 of Form 941 (or line 10 of Form 941-SS)

©

SCHEDULE B

(FORM 941)

5151

A

B

C

D

A

B

C

D

Schedule B (Form 941) (Rev. 11-98)For Paperwork Reduction Act Notice, see page 2.

Page 2Schedule B (Form 941) (Rev. 11-98)

Paperwork Reduction Act Notice. We

ask for the infor mation on this form to

carry out the Internal Revenue laws of

the United States. You are required to

give us the infor mation. We need it to

ensure that you are complying with

these laws and to allow us to figure and

collect the right amount of tax.

The time needed to complete and file

this for m will vary depending on

individual circumstances. The estimated

average time is 2 hr., 53 min.

If you have comments concerning the

accuracy of this time estimate or

suggestions for making this for m

simpler, we would be happy to hear from

you. You can write to the Tax For ms

Committee, Western Area Distribution

Center, Rancho Cordova, CA

95743-0001. DO NOT send the tax for m

to this address. Instead, see Where to

file in the For m 941 or 941-SS

instructions.

General Instructions

Purpose of form. Use Schedule B

(For m 941) to report your tax liability

(income tax withheld plus both employee

and employer social security and

Medicare taxes minus any advance

ear ned income credit payments) on a

daily basis. For m 941-SS filers report

only employee and employer social

security and Medicare taxes. Do not

show Federal tax deposits. Deposit

infor mation is obtained from the deposit

coupons (For m 8109) or from the

Electronic Federal Tax Payment System

(EFTPS).

Who must file. Semiweekly schedule

depositors are required to complete and

attach Schedule B to Form 941. Monthly

schedule depositors who accumulate

$100,000 or more on any day must also

complete and attach Schedule B. If your

total tax liability for the quarter is less

than $1,000, you need not complete

Schedule B (Form 941). Schedule B also

must be used by semiweekly schedule

depositors who file Form 941-SS,

Employer’s Quarterly Federal Tax Retur n

(for American Samoa, Guam, the

Commonwealth of the Norther n Mariana

Islands, and the U.S. Virgin Islands).

Specific Instructions

Enter the monthly totals on lines A, B,

and C. Add these monthly subtotals and

enter the total tax liability for the quarter

on line D. The amount on line D should

equal For m 941, line 13; or Form

941-SS, line 10.

Completing the Employer’s Record of

Federal Tax Liability. If you are required

to report your tax liabilities on Schedule

B (For m 941) as discussed above, file

the schedule with Forms 941 or 941-SS.

Do not complete columns (a) through (d)

of the Monthly Summary of Federal Tax

Liability (line 17 on For m 941 or

941-SS). However, be sure to mark the

Schedule B checkbox above line 17.

Example B. Employer B is a semiweekly

schedule depositor. It has paydays every

other Friday. It accumulated a $20,000

employment tax liability on each of the

following pay dates: 1/8/99; 1/22/99;

2/5/99; 2/19/99; 3/5/99; and 3/19/99.

Since Employer B is a semiweekly

schedule depositor, it is required to

record its tax liabilities on Schedule B

(For m 941). Employer B must record the

$20,000 liabilities on lines 8 and 22 of

part A (First Month of Quarter); lines 5

and 19 of part B (Second Month of

Quarter); and lines 5 and 19 of part C

(Third Month of Quarter).

Example C. Employer C is a new

business and is a monthly schedule

depositor for 1999. Employer C has

paydays every Friday and accumulated a

$2,000 employment tax liability on

1/8/99 and a $110,000 tax liability on

1/15/99 and each of the following

Fridays during 1999. Under the deposit

rules, an employer becomes a

semiweekly schedule depositor when a

$100,000 or more tax liability is

accumulated on any day within a

deposit period (see section 11 of

Circular E or section 9 of Circular SS for

details). Because Employer C

accumulated $112,000 on 1/15/99, it

became a semiweekly schedule

depositor on that date and must

complete Schedule B (For m 941) and file

it with For m 941 or 941-SS. It should

record the $2,000 liability on line 8 of

section A and $110,000 on the lines for

the remaining pay dates. Employer C

does not complete the Monthly

Summary of Federal Tax Liability (line 17

of For m 941 or 941-SS) even though it

was a monthly schedule depositor until

1/15/99.

Each numbered space on the

schedule corresponds to dates during

the quarter. Report your tax liabilities on

this schedule corresponding to the dates

wages are paid, not to when payroll

liabilities are accrued. For example, if

your payroll period ends December 31,

1998, and the wages for that period are

paid on January 5, 1999, the

employment tax liability for those wages

should be reported on Schedule B for

the first quarter of 1999 on line 5,

section A (First Month of Quarter).

Example A. Employer A, who is a

semiweekly schedule depositor, pays

wages once each month on the last day

of the month. On December 20, 1999,

Employer A also paid year-end employee

bonuses (subject to employment tax and

income tax withholding). Because

Employer A is a semiweekly schedule

depositor, it is required to record

employment tax and withholding

liabilities on Schedule B (For m 941).

Employer A should report tax liabilities

for the 4th quarter (October–December)

on line 31, section A (First Month of

Quarter); line 30, section B (Second

Month of Quarter); and lines 20 and 31,

section C (Third Month of Quarter).

Important. Schedule B (Form 941) is

used by the IRS to deter mine if you

have timely deposited your employment

and withholding tax liabilities. Unless

Schedule B is properly completed and

filed with For m 941 or 941-SS, the IRS

will not be able to process your retur n

and will have to contact you for the

missing infor mation.

Adjustments. Semiweekly schedule

depositors must take into account on

Schedule B adjustments to correct

errors on prior retur ns (reported on lines

4 and 9 of For m 941 or on line 9 of

Form 941-SS). If the adjustment was to

correct an underreported liability in a

prior quarter, report the adjustment on

the entry space corresponding to the

date the error was discovered.

If the adjustment corrects an

overreported liability, use the

adjustment amount as a credit to offset

subsequent liabilities until it is used up.

For example, Employer D discovered on

1/15/99 that it overreported social

security tax on a prior quarter return by

$10,000. It paid wages on 1/8/99,

1/15/99, 1/22/99, and 1/29/99 and had a

$5,000 tax liability for each of those pay

dates. Employer D must report a $5,000

liability on line 8, section A of Schedule

B. The adjustment for the $10,000

overreported liability is used to offset the

1/15/99 and 1/22/99 liabilities, so these

two $5,000 liabilities are not deposited

or reported on Schedule B. The $5,000

liability for 1/29/99 must be reported on

line 29, section A of Schedule B. See

section 13 of Circular E for details on

reporting adjustments to correct errors

on prior period returns.

You are not required to provide the

infor mation requested on a for m that is

subject to the Paperwork Reduction Act

unless the for m displays a valid OMB

control number. Books or records

relating to a form or its instructions must

be retained as long as their contents

may become material in the

administration of any Internal Revenue

law. Generally, tax returns and return

infor mation are confidential, as required

by Code section 6103.