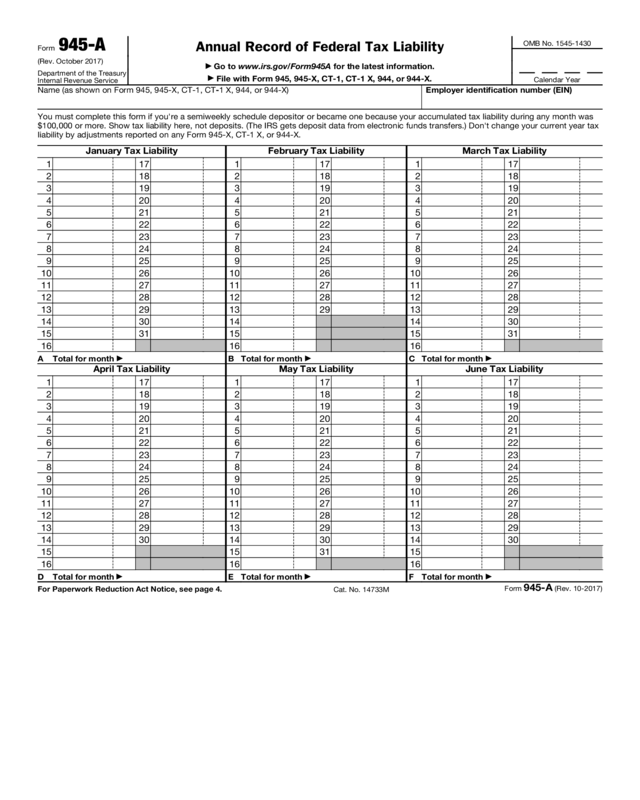

Fillable Printable Form 945-A (Rev. October 2017)

Fillable Printable Form 945-A (Rev. October 2017)

Form 945-A (Rev. October 2017)

Form 945-A

(Rev. October 2017)

Department of the Treasury

Internal Revenue Service

Annual Record of Federal Tax Liability

▶

Go to www.irs.gov/Form945A for the latest information.

▶

File with Form 945, 945-X, CT-1, CT-1 X, 944, or 944-X.

OMB No. 1545-1430

Calendar Year

Name (as shown on Form 945, 945-X, CT-1, CT-1 X, 944, or 944-X) Employer identification number (EIN)

You must complete this form if you're a semiweekly schedule depositor or became one because your accumulated tax liability during any month was

$100,000 or more. Show tax liability here, not deposits. (The IRS gets deposit data from electronic funds transfers.) Don't change your current year tax

liability by adjustments reported on any Form 945-X, CT-1 X, or 944-X.

January Tax Liability

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

A Total for month

▶

February Tax Liability

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

B Total for month

▶

March Tax Liability

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

C Total for month

▶

April Tax Liability

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

D Total for month

▶

May Tax Liability

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

E Total for month

▶

June Tax Liability

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

F Total for month

▶

For Paperwork Reduction Act Notice, see page 4.

Cat. No. 14733M

Form

945-A (Rev. 10-2017)

Form 945-A (Rev. 10-2017)

Page 2

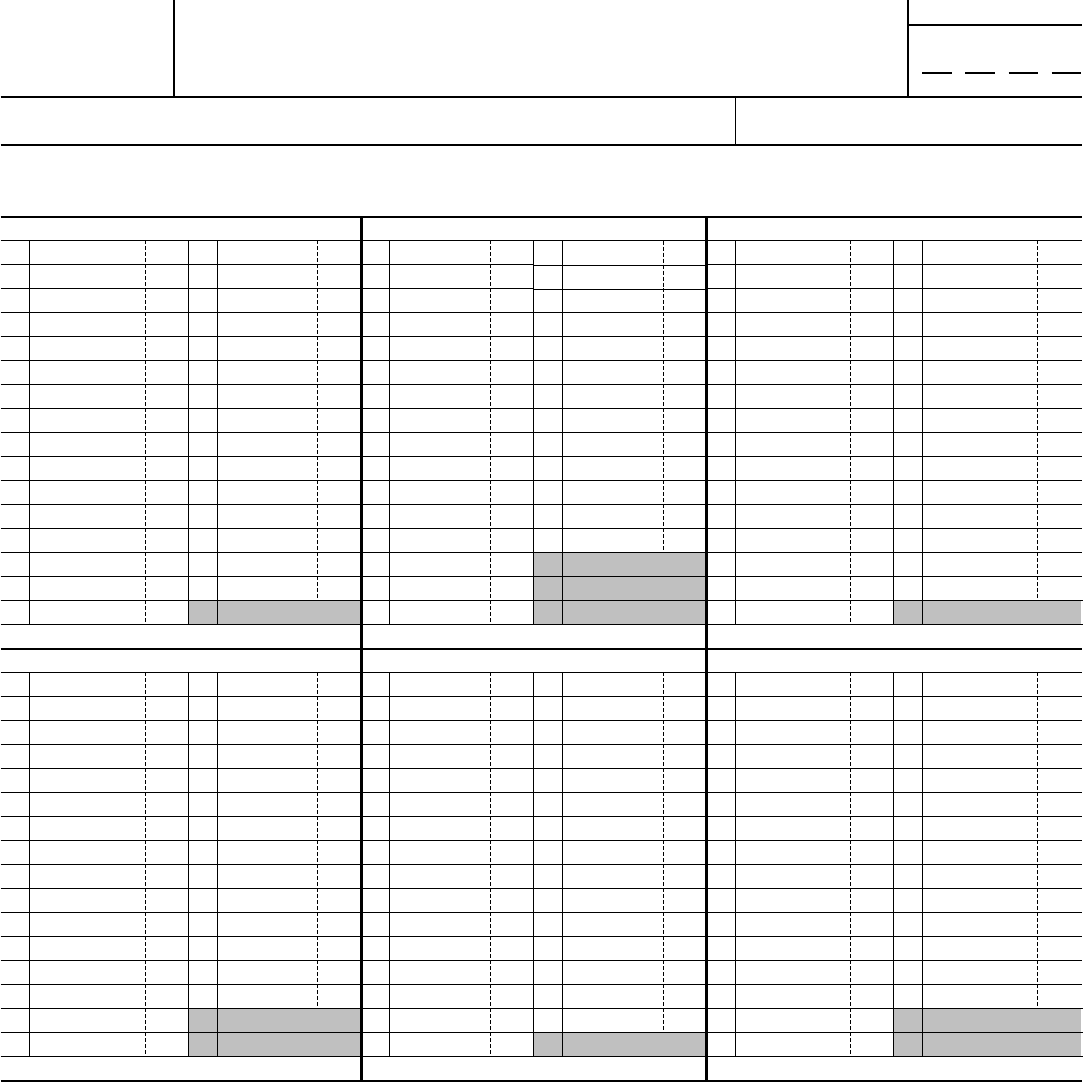

July Tax Liability

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

G Total for month

▶

August Tax Liability

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

H Total for month

▶

September Tax Liability

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

I Total for month

▶

October Tax Liability

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

J Total for month

▶

November Tax Liability

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

K Total for month

▶

December Tax Liability

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

L Total for month

▶

M Total tax liability for the year (add lines A through L). This should equal line 3 on Form 945 (line 15

on Form CT-1, line 9 on Form 944). . . . . . . . . . . . . . . . . . . . . .

▶

Form 945-A (Rev. 10-2017)

Form 945-A (Rev. 10-2017)

Page 3

Future Developments

For the latest information about developments related to Form

945-A and its instructions, such as legislation enacted after they

were published, go to www.irs.gov/Form945A.

What's New

Adjusting tax liability for the qualified small business payroll tax

credit for increasing research activities (Form 944 only). For

2017 and subsequent years, you must account for any qualified

small business payroll tax credit for increasing research activities

that you reported on Form 944, line 8, when reporting your liabilities

on Form 945-A. The total liability for the year must equal Form 944,

line 9. Failure to account for the amount reported on Form 944, line

8, may cause Form 945-A to report more than the total taxes after

adjustments and credits reported on Form 944, line 9.

The qualified small business payroll tax credit for increasing

research activities applies to the employer share of social security

tax on wages paid in the quarter that begins after the income tax

return electing the credit has been filed. In completing Form 945-A,

you take into account the payroll tax credit against your liability for

the employer share of social security tax starting with the first

payroll payment of the quarter that includes payments of wages to

your employees that are subject to social security tax. Don't reduce

your daily tax liability reported on Form 945-A below zero. For more

information, see the line 13 instructions in the Instructions for

Form 944.

Reminders

Reporting prior period adjustments. Prior period adjustments are

reported on Form 945-X, Adjusted Annual Return of Withheld

Federal Income Tax or Claim for Refund; Form CT-1 X, Adjusted

Employer's Annual Railroad Retirement Tax Return or Claim for

Refund; or Form 944-X, Adjusted Employer's ANNUAL Federal Tax

Return or Claim for Refund; and aren't taken into account when

figuring the tax liability for the current year.

When you file Form 945-A with your Form 945, CT-1, or 944,

don't change your current year tax liability by adjustments reported

on any Form 945-X, CT-1 X, or 944-X.

Amended Form 945-A. If you have been assessed a

failure-to-deposit (FTD) penalty, you may be able to file an amended

Form 945-A. For more information, see Correcting Previously

Reported Tax Liability, later.

General Instructions

Purpose of form. Use Form 945-A to report your federal tax liability

(based on the dates payments were made or wages were paid) for

the following tax returns.

• Forms 945 and 945-X for federal income tax withholding on

nonpayroll payments. Nonpayroll withholding includes backup

withholding and federal income tax withholding on pensions,

annuities, IRAs, Indian gaming profits, gambling winnings, military

retirement, certain government payments on which the recipient

elected voluntary income tax withholding, and dividends and other

distributions by an Alaska Native Corporation on which the recipient

elected voluntary income tax withholding.

• Forms CT-1 and CT-1 X for both employee and employer Tier 1

and Tier 2 taxes.

• Forms 944 and 944-X for federal income tax withheld plus both

employee and employer social security and Medicare taxes.

Forms 944(SP) and 944-X (SP). If you're a semiweekly schedule

depositor who files Formulario 944(SP), Declaración Federal ANUAL

de Impuestos del Patrono o Empleador, you should use Formulario

943A-PR, Registro de la Obligación Contributiva Federal del

Patrono Agrícola, to report your tax liability. You should also file

Form 943A-PR if you file Form 944-X (SP) and you need to amend a

previously filed Form 943A-PR.

Who must file. Semiweekly schedule depositors must complete

and file Form 945-A with their tax return. Don't file Form 945-A if

your net tax liability for the return period is less than $2,500. Don't

file this form if you're a monthly schedule depositor unless you

accumulated a tax liability of $100,000 during any month of the

year. Monthly schedule depositors who accumulate $100,000 or

more of tax liability on any day of a calendar month become

semiweekly schedule depositors on the next day and remain so for

at least the remainder of the year and for the next year, and must

also complete and file Form 945-A for the entire year.

The deposit rules, including the $100,000 Next-Day Deposit Rule,

are explained in section 11 of Pub. 15, Employer's Tax Guide, and

in the instructions for your tax return.

Caution: The IRS uses Form 945-A to match the tax liability you

reported on the returns indicated earlier with your deposits. The IRS

also uses Form 945-A to determine if you have deposited your tax

liabilities on time. Unless Form 945-A is properly completed and

filed (if applicable) with your tax return, the IRS may propose an

“averaged” FTD penalty. See Deposit Penalties in section 11 of Pub.

15 for more information.

When to file. File Form 945-A with your Form 945, CT-1, or 944

every year when Form 945, CT-1, or 944 is due. See the instructions

to these forms for their due dates.

Specific Instructions

Enter your business information. Carefully enter your employer

identification number (EIN) and name at the top of the form. Make

sure that they exactly match the name of your business and the EIN

that the IRS assigned to your business and also agree with the

name and EIN shown on the attached Form 945, 945-X, CT-1,

CT-1 X, 944, or 944-X.

Calendar year. Enter the calendar year of the Form 945, 945-X,

CT-1, CT-1 X, 944, or 944-X to which Form 945-A is attached.

Form 945 filers. Don't complete entries A through M of the Monthly

Summary of Federal Tax Liability (Form 945, line 7). Be sure to mark

the semiweekly schedule depositor checkbox above line 7 on

Form 945.

Form CT-1 filers. Don't complete the Monthly Summary of Railroad

Retirement Tax Liability (Part II of Form CT-1).

Form 944 filers. On Form 944, check the box for “Line 9 is $2,500

or more” at line 13, and leave blank lines 13a–13m.

Enter your tax liability by month. Each numbered space on

Form 945-A corresponds to a date during the year. Enter your tax

liabilities in the spaces that correspond to the dates you paid wages

to your employees or made nonpayroll payments, not the date

liabilities were accrued or deposits were made. The total tax liability

for the year (line M) must equal net taxes on Form 945 (line 3), Form

CT-1 (line 15), or Form 944 (line 9). Enter the monthly totals on lines

A, B, C, D, E, F, G, H, I, J, K, and L. Enter the total for the year on

line M.

For example, if you're a Form 945 filer, and you became liable for

a pension distribution on December 31, 2016, but didn't make the

distribution until January 7, 2017, you would:

• Go to January on Form 945-A filed with your 2017 return, and

• Enter your tax liability on line 7 because line 7 represents the

seventh day of the month.

Example 1. Cedar Co., which has a semiweekly deposit

schedule, makes periodic payments on gambling winnings on the

15th day of each month. On December 24, 2017, in addition to its

periodic payments, it withheld from a payment on gambling

winnings under the backup withholding rules. Since Cedar Co. is a

semiweekly schedule depositor, it must record these nonpayroll

withholding liabilities on Form 945-A. It must report tax liabilities on

line 15 for each month and line 24 for December.

Cedar Co. enters the monthly totals on lines A through L. It adds

these monthly subtotals and enters the total tax liability for the year

on line M. The amount on line M should equal Form 945, line 3.

Form 945-A (Rev. 10-2017)

Page 4

Example 2. Fir Co. is a semiweekly schedule depositor. During

January, it withheld federal income tax on pension distributions as

follows: $52,000 on January 10; $35,000 on January 24. Since Fir

Co. is a semiweekly schedule depositor, it must record its federal

income tax withholding liabilities on Form 945-A. It must record

$52,000 on line 10 and $35,000 on line 24 for January.

Example 3. Elm Co. is a new business and monthly schedule

depositor for 2017. During January, it withheld federal income tax

on nonpayroll payments as follows: $2,000 on January 10; $99,000

on January 24. The deposit rules require that a monthly schedule

depositor begin depositing on a semiweekly deposit schedule when

a $100,000 or more tax liability is accumulated on any day within a

month (see section 11 of Pub. 15 for details). Since Elm Co.

accumulated $101,000 ($2,000 + $99,000) on January 24, 2017, it

became a semiweekly schedule depositor on January 25, 2017. Elm

Co. must complete Form 945-A and file it with Form 945. It must

record $2,000 on line 10 and $99,000 on line 24 for January. No

entries should be made on Form 945, line 7, even though Elm Co.

was a monthly schedule depositor until January 25.

Correcting Previously Reported Tax Liability

Semiweekly schedule depositors. If you have been assessed an

FTD penalty and you made an error on Form 945-A and the

correction won't change the total liability you reported on Form

945-A, you may be able to reduce your penalty by filing an

amended Form 945-A.

Example. You reported a tax liability of $3,000 on January 1.

However, the liability was actually for March. Prepare an amended

Form 945-A showing the $3,000 liability on March 1. Also, you must

enter the liabilities previously reported for the year that didn't

change. Write “Amended” at the top of Form 945-A. The IRS will

refigure the penalty and notify you of any change in the penalty.

Monthly schedule depositors. You can file Form 945-A if you have

been assessed an FTD penalty and you made an error on the

monthly tax liability section of Form 945. When completing Form

945-A for this situation, only enter the monthly totals. The daily

entries aren't required.

Where to file. File your amended Form 945-A, or, for monthly

schedule depositors, your original Form 945-A at the address

provided in the penalty notice you received. If you're filing an

amended Form 945-A, you don't have to submit your original

Form 945-A.

Forms 945-X, CT-1 X, and 944-X

You may need to file an amended Form 945-A with Forms 945-X,

CT-1 X, or 944-X to avoid or reduce an FTD penalty.

Tax decrease. If you're filing Form 945-X, CT-1 X, or 944-X, you

can file an amended Form 945-A with the form if both of the

following apply.

1. You have a tax decrease.

2. You were assessed an FTD penalty.

File your amended Form 945-A with Form 945-X, CT-1 X, or

944-X. The total liability reported on your amended Form 945-A

must equal the corrected amount of tax reported on Form 945-X,

CT-1 X, or 944-X. If your penalty is decreased, the IRS will include

the penalty decrease with your tax decrease.

Tax increase—Form 945-X, CT-1 X, or 944-X filed timely. If

you're filing a timely Form 945-X, CT-1 X, or 944-X showing a tax

increase, don't file an amended Form 945-A, unless you were

assessed an FTD penalty caused by an incorrect, incomplete, or

missing Form 945-A. Don't include the tax increase reported on

Form 945-X, CT-1 X, or 944-X on an amended Form 945-A you file.

Tax increase—Form 945-X, CT-1 X, or 944-X filed late. If you

owe tax and are filing late, that is, after the due date of the return for

the filing period in which you discovered the error, you must file the

form with an amended Form 945-A. Otherwise, the IRS may assess

an “averaged” FTD penalty.

The total tax reported on line M of Form 945-A must match the

corrected tax (Form 945, line 3; Form 944, line 9 (line 7 for years

before 2017); Form CT-1, line 15); combined with any correction

reported on Form 945-X, line 5; Form 944-X, line 17; or Form

CT-1 X, line 19; for the year, less any previous abatements and

interest-free tax assessments.

Note: Form 944-X, line 17, which is referenced above, will change

to line 18 on the February 2018 revision of Form 944-X.

Paperwork Reduction Act Notice. We ask for the information on

this form to carry out the Internal Revenue laws of the United

States. You're required to give us the information. We need it to

ensure that you're complying with these laws and to allow us to

figure and collect the right amount of tax.

You're not required to provide the information requested on a

form that is subject to the Paperwork Reduction Act unless the form

displays a valid OMB control number. Books or records relating to a

form or its instructions must be retained as long as their contents

may become material in the administration of any Internal Revenue

law. Generally, tax returns and return information are confidential,

as required by Code section 6103.

The time needed to complete and file this form will vary

depending on individual circumstances. The estimated average

time is:

Recordkeeping . . . . . . . . . . . . 6 hr., 27 min.

Learning about the

law or the form . . . . . . . . . . . . . . 6 min.

Preparing and sending

the form to the IRS . . . . . . . . . . . . . 12 min.

If you have comments concerning the accuracy of these time

estimates or suggestions for making this form simpler, we would be

happy to hear from you. You can write to the IRS at the address

listed in the Privacy Act Notice for your tax return.