Fillable Printable Form Int-2 - 2014 Bank Franchise Tax Return

Fillable Printable Form Int-2 - 2014 Bank Franchise Tax Return

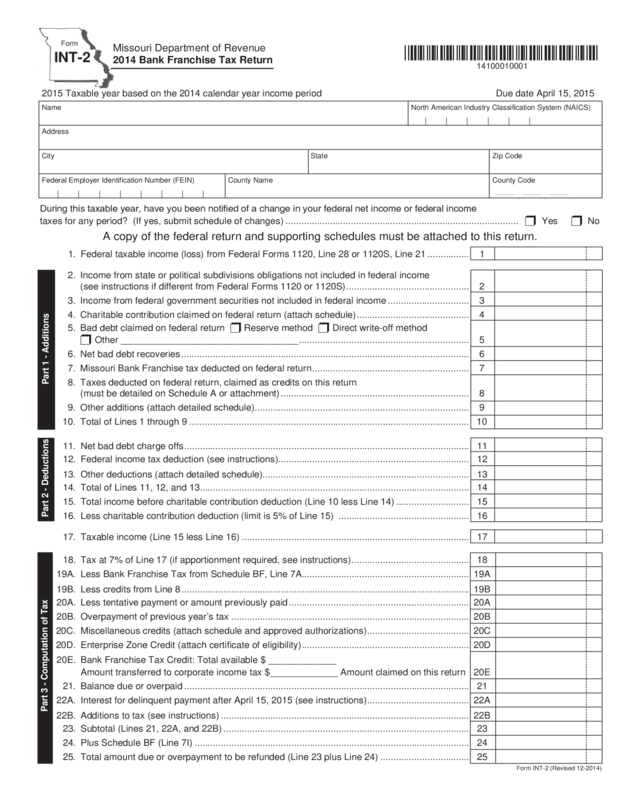

Form Int-2 - 2014 Bank Franchise Tax Return

Form

INT-2

Missouri Department of Revenue

2014 Bank Franchise Tax Return

18. Tax at 7% of Line 17 (if apportionment required, see instructions) ............................................. 18

19A. Less Bank Franchise Tax from Schedule BF, Line 7A................................................................ 19A

19B. Less credits from Line 8 .............................................................................................................. 19B

20A. Less tentative payment or amount previously paid ..................................................................... 20A

20B. Overpayment of previous year’s tax ........................................................................................... 20B

20C. Miscellaneous credits (attach schedule and approved authorizations) ....................................... 20C

20D. Enterprise Zone Credit (attach certificate of eligibility) ................................................................ 20D

20E. Bank Franchise Tax Credit: Total available $ _____________

Amount transferred to corporate income tax $_____________ Amount claimed on this return 20E

21. Balance due or overpaid ............................................................................................................. 21

22A. Interest for delinquent payment after April 15, 2015 (see instructions) ....................................... 22A

22B. Additions to tax (see instructions) ............................................................................................... 22B

23. Subtotal (Lines 21, 22A, and 22B) .............................................................................................. 23

24. Plus Schedule BF (Line 7I) ......................................................................................................... 24

25. Total amount due or overpayment to be refunded (Line 23 plus Line 24) .................................. 25

Part 3 - Computation of Tax

Form INT-2 (Revised 12-2014)

2. Income from state or political subdivisions obligations not included in federal income

(see instructions if different from Federal Forms 1120 or 1120S) ............................................... 2

3. Income from federal government securities not included in federal income ............................... 3

4. Charitable contribution claimed on federal return (attach schedule) ........................................... 4

5. Bad debt claimed on federal return r Reserve method r Direct write-off method

r Other __________________________________ ................................................................. 5

6. Net bad debt recoveries .............................................................................................................. 6

7. Missouri Bank Franchise tax deducted on federal return ............................................................ 7

8. Taxes deducted on federal return, claimed as credits on this return

(must be detailed on Schedule A or attachment) ........................................................................ 8

9. Other additions (attach detailed schedule).................................................................................. 9

10. Total of Lines 1 through 9 ........................................................................................................... 10

Part 1 - Additions

1. Federal taxable income (loss) from Federal Forms 1120, Line 28 or 1120S, Line 21 ................ 1

During this taxable year, have you been notied of a change in your federal net income or federal income

taxes for any period? (If yes, submit schedule of changes)

......................................................................................... r Yes r No

A copy of the federal return and supporting schedules must be attached to this return.

2015 Taxable year based on the 2014 calendar year income period Due date April 15, 2015

Name North American Industry Classification System (NAICS)

Address

City State Zip Code

Federal Employer Identification Number (FEIN) County Name County Code

| | | | | | | |

11. Net bad debt charge offs ............................................................................................................. 11

12. Federal income tax deduction (see instructions)......................................................................... 12

13. Other deductions (attach detailed schedule)............................................................................... 13

14. Total of Lines 11, 12, and 13....................................................................................................... 14

15. Total income before charitable contribution deduction (Line 10 less Line 14) ............................ 15

16. Less charitable contribution deduction (limit is 5% of Line 15) .................................................. 16

17. Taxable income (Line 15 less Line 16) ....................................................................................... 17

Part 2 - Deductions

*14100010001*

14100010001

| | | | | |

Reset Form

Print Form

Reset Form

Print Form

Description (Do not list tangible personal property tax on leased property) Amount

Total (Enter on Lines 8 and 19B, Page 1)

Schedule A - Taxes Claimed As Credits

Make check or money order payable to “Missouri Department of Revenue”. Mail completed form and attachments to the address below.

If you pay by check, you authorize the Department of Revenue to process the check electronically. Any returned check may be presented

again electronically.

Signature of Officer (Required) Title of Officer Phone Number Date (MM/DD/YYYY)

(___ ___ ___)___ ___ ___-___ ___ ___ ___ __ __ /__ __ /__ __ __ __

Preparer’s Signature (Including Internal Preparer) Preparer’s FEIN, SSN, or PTIN Phone Number Date (MM/DD/YYYY)

(___ ___ ___)___ ___ ___-___ ___ ___ ___ __ __ /__ __ /__ __ __ __

I authorize the Director of Revenue or delegate to discuss my return and attachments with the preparer or any

member of his or her firm, or if internally prepared, any member of the internal staff

.............................................. r Yes r No

Under penalties of perjury, I declare that the above information and any attached supplement is true, complete, and correct.

Declaration of preparer (other than taxpayer) is based on all information of which he or she has any knowledge.

Authorization and Signature

Mail to: Taxation Division Phone: (573) 751-2326

P.O. Box 898 TTY: (800) 735-2966

Jefferson City, MO 65105-0898 Fax: (573) 522-1721

E-mail: [email protected]

Visit http://dor.mo.gov/business/finance

for additional information.

Form INT-2 (Revised 12-2014)

*14100020001*

14100020001

Reset This Section Only

Enter your three digit county code of the principal place of your institution

from the list provided at the end of these instructions.

Part 1

Line 1 Enter the amount of taxable income or loss from Federal Form

1120, Line 28, before any net operating loss deduction or special

deduction is applied, or Federal Form 1120S, Line 21.

Taxpayers that are members of an affiliated group filing a consolidated

federal income tax return shall compute federal taxable income as if

a separate federal tax return had been filed by each member of the

affiliated group. A pro forma federal return or appropriate schedules

should then be attached together with a copy of pages 1 through 4 of the

consolidated federal income tax return.

Line 2

Enter all income received on state or political subdivision obli-

gations excluded from the federal return. This income is taxable on this

return. Explain if different from tax-exempt interest shown on the federal

return.

Line 3

Enter all income received on federal securities excluded from

the federal return (e.g., non-taxable portion Federal Reserve Bank

dividends). This income is taxable on this return.

Line 4

Enter the charitable contribution claimed on the federal return.

Line 5 Enter the bad debt claimed on the federal return or any

additions to a bad debt reserve claimed as a de duc tion on federal return.

(The reserve method is not a permissible method on this return.) In

the appropriate box, indicate the bad debt method used on the federal

return.

Line 6

Enter the excess, if any, of recoveries of bad debts previously

charged off over current year charge offs. Attach schedule of bad debt

computation.

Line 7

Enter any Missouri Bank Franchise Tax deducted on the federal

return. This is not an allowable deduction on this return.

Note: Cash basis banks should add the Missouri Bank Franchise Tax

paid in the preceding calendar year. Accrual basis banks should add the

Missouri Bank Franchise Tax accrued during the previous calendar year.

Line 8

Enter here and on Line 19B any taxes claimed as credits on

this return. All taxes paid to the State of Missouri or any political subdivi-

sion thereof are eligible except taxes on real estate, unemployment taxes,

bank tax, and taxes on tangible personal property owned by the taxpayer

and held for lease or rental to others. Show detail on Page 2, Schedule

A. All state and local sales and use taxes paid by banks as purchasers to

sellers, vendors, or the State of Missouri on purchases of tangible personal

property and services enumerated in Chapter 144, RSMo, may be

claimed as a credit. Capitalized sales and use taxes paid by banks as

purchasers are creditable. Documentation to support the capitalized

sales and use tax credit must be available upon request.

Certain criteria must be met in order for a tax credit to be allowable

pursuant to

Regulation 12 CSR 10-10.150, Tax Credits on Bank Tax

Return, as follows:

(1) The following criteria shall be used to establish whether or not a

tax credit may be claimed against the Bank Franchise Tax,

imposed by Sections 148.010 to 148.110, RSMo, computed

pursuant to Section 148.030.3, RSMo:

(A) The payment must have been made to the state of Missouri or

a political subdivision located in the state of Missouri.

(B) Payment must have resulted from a tax liability imposed by

a government agency, as defined in subsection (1)(A), and

cannot be a regulatory fee collected solely for the purpose of

paying the cost of administering the taxing jurisdiction’s laws.

(C) The following should be used as a general guideline to

de termine if an exaction, required by subsection (1)(A), is an

allowable tax credit or a non-creditable fee:

1. If the proceeds, paid as defined in subsection (1)(A), are

collected for deposit into the general revenue account of the

taxing jurisdiction, to raise revenue for said entity, then it is a

tax and is an allowable tax credit.

2. If the proceeds, paid as defined in subsection (1)(A), are

collected primarily to cover the costs of the regulation of an

activity, and which are then deposited with the regulatory

agency, then it is a non-cre dit able fee.

(2) At all times the burden of establishing whether an exaction is an

allowable tax credit or a non-creditable fee shall be on the taxpayer.

An accrual basis taxpayer that is a member of an affiliated group filing

a consolidated Missouri income tax return shall allocate a portion of the

consolidated Missouri income tax liability for the year by multiplying such

liability by a fraction, the numerator of which is the separate Missouri

taxable income of such member, and the denominator of which is the

sum of the separate Missouri taxable incomes of all members having

Missouri taxable income for the applicable year.

A cash basis taxpayer that is a member of an affiliated group filing a

consolidated Missouri income tax return shall allocate each component

of the consolidated Missouri income tax paid (or refunded) during the

year by multiplying each component by a fraction, the numerator of

which is the separate Missouri taxable income of such member for the

The 2014 Bank Franchise Tax Return (Form INT-2) form must be

completed and filed by April 15, 2015. An extension of time to file this

return can be requested through the Application for Extension of Time to

File (Form 7004). An extension of time to file the return does not extend the

time for payment of the tax. An extension of time may not exceed 180 days

from the due date (April 15) pursuant to Regulation 12 CSR 10-10.110.

Note: Any payment submitted after the due date of April 15 is subject to

interest at the rate determined by Section 32.065, RSMo which can be

obtained from the Department’s website at http://dor.mo.gov/intrates.php.

If any return is not filed by the due date, a penalty of 5% per month, not

to exceed 25%, is calculated on the amount due.

This return must be filed by every bank and every trust company organized

under any general or special law of this state and every national banking

association located in this state and any branch or office physically located

in this state of any commercial bank or trust company.

The Financial Institution Tax Schedule B (Form 2331) must be

completed and submitted with each Form INT-2. For proper completion,

please refer to Regulation 12 CSR 10-10.020. If any bank operates

more than one office or branch in Missouri, the bank shall file one return

giving the address of each office or branch with the total dollar amounts

of accounts or deposits of each office on Form 2331.

All returns are filed based upon a calendar year business activity basis.

Section 148.010 – 148.112, RSMo

This information is for guidance only and does not state the complete law.

Missouri Department of Revenue

General Instructions - 2014 Bank Franchise Tax Return

Instructions

*14000000001*

14000000001

applicable year, and the denominator of which is the sum of the separate

Missouri taxable incomes of all members having Missouri income for the

applicable year.

In the computation of separate Missouri taxable income, each member of

a group filing a consolidated Missouri income tax return shall start with its

separate federal taxable income as computed pursuant to the method

applicable to the group under Treasury Regulation 1.1552-1. The

amount of the federal income tax deduction of each member under

Section 143.171.1, RSMo, shall be that portion of the actual federal

consolidated income tax liability of the group as is required to be

allocated to such member under Internal Revenue Code Section 1552

without regard to any additional allocations under Treasury Regulation

1.1502-33(d).

The following are not allowable credits:

• Sales tax paid to check printer(s) on checks the bank sold to its

customers

• Annual registration fee as this is not a tax

Attach schedule of taxes deducted on Line 17, federal Form 1120 or

federal Form 1120S, Line 12, for verification purposes.

Line 9

Enter deductions claimed on the federal return which are not

allowable on this return and income not included on the federal return

which is required to be included on this return. (Attach schedule.) The

environmental tax under Section 59A of the Internal Revenue Code must

be added back to income. Any gain from the complete liquidation of

another corporation that is not recognized because of Section 332 of the

Internal Revenue Code must be added to income.

Line 10

Enter the total of Lines 1 through 9.

Part 2

Line 11 Enter the excess, if any, of bad debt charge offs over current

year recoveries. Attach schedule of bad debt computation.

Line 12

Enter the relevant income period deduction for federal income

taxes. The relevant income period deduction is the amount actually

accrued (if an accrual basis taxpayer) or paid (if a cash basis taxpayer)

during the income period.

A taxpayer that is a member of an affiliated group of corporations

which filed a consolidated federal income tax return shall determine its

deduction for, or its gross income in respect of federal income taxes paid

or accrued during the income period to the United States as if it and all

other members of the affiliated group of which it was a member had filed

separate federal income tax returns for all relevant income periods.

Line 13

Enter the total amount of any deduction claimed on this return

and not included on the federal return. These deductions must be

itemized on a schedule attached to this return.

Banks that are required to recapture bad debt reserve to income

pursuant to 26 USC § 585 should include the dollar amount recaptured

to income on Line 13.

Line 14

Enter the total of Lines 11 through 13.

Line 15 Subtract Line 14 from Line 10 and enter amount. If “loss”,

indicate by brackets “( )” and enter “none” on Line 18.

Line 16

Enter the charitable contribution deduction claimed on this

return. The contribution deduction is limited to 5% of taxable income

before the contribution deduction. Contribution carryover from prior

year’s allow ance on federal return is not allowable on this return. Attach

charitable contribution schedule for verification purposes.

Line 17

Subtract Line 16 from Line 15 and enter amount.

Part 3

Line 18 Multiply the taxable income amount on Line 17 by 7% and

enter amount. If Line 10 includes income from business activity both

within and without the State of Missouri from offices or branches located

in such state, the taxpayer may be eligible to apportion the tax. These

taxpayers shall complete Apportionment Schedule Bank Franchise Tax

(Form 4347) and attach to this return.

Line 19A Enter the Bank Franchise Tax from Line 7A Schedule BF.

Line 19B Enter the amount from Line 8.

Line 20A Enter the amount of tentative payment (if applicable).

Line 20B Enter overpayment of previous year’s tax.

Line 20C

Enter the amount of tax credits claimed from the list on

the following page.

Attach a schedule listing the amounts for each tax credit and a copy of the

approved authorization to the return. See Section 148.064.1, RSMo, for

ordering of tax credits. Tax credits can only be used once.

Line 20D Enter the approved Enterprise Zone Credit claimed. To

be eligible for this credit, you must use the percentages from the

second paragraph of the Department of Economic Development (DED)

certification letter and attach a copy to the INT-2.

Compute the allowable Enterprise Zone Credit using the greater of the

following methods. The same method must be used for both taxes.

1. Seven percent (7%) calculation for Line 20D:

• Line 17 (taxable income) X DED percentage of income X 7%

or

• Line 18 (tax) less Lines 19A and 19B X DED percentage of tax

2. Schedule BF calculation for Line 7B:

• Line 6A or 6B (assets) X DED percentage of income X .00013

or

• Line 7A (tax liability) X DED percentage of tax

Line 20E The Bank Franchise Tax Credit is equal to 1/60th of one

percent (.000167) of the amount entered on Line 6A or 6B of Schedule

BF, if Line 6A or 6B exceeds one million dollars. Compute the total

available Bank Franchise Tax Credit and enter in the space provided.

Enter the amount claimed on this return on Line 20E. Any unused credit

may be applied to the corporate income tax liability. Enter the amount to

be transferred to corporate income tax in the space provided.

Line 21 Subtract Lines 19A and 19B from Line 18. Amount shall not be

less than zero. Subtract Lines 20A through 20E from result above and

enter amount.

Line 22A

Calculate interest for period which tax payment is delinquent.

Interest is calculated from the due date of April 15 through the date of

payment at the annual interest rate which can be obtained from the

Department’s website at: http://dor.mo.gov/intrates.php.

Line 22B

Compute additions to tax, if applicable, and enter on Line 22B.

1. For failure to pay by the due date — multiply Line 21 by 5%; or

2. For failure to file your return by the due date — multiply Line 21

by 5% for each month late, not to exceed 25%.

Line 23 Enter the total of Lines 21, 22A, and 22B.

Line 24 Enter the amount shown on Line 7I Schedule BF.

Line 25 Enter the total of Lines 23 and 24. If a balance due, submit this amount.

*14000000001*

14000000001

Taxation Division Phone: (573) 751-2326

P.O. Box 898 Fax: (573) 522-1721

Jefferson City, MO 65105-0898 TTY: (800) 735-2966

E-mail: [email protected]

Visit http://dor.mo.gov/business/finance/

for additional information.

Affordable Housing Assistance

Agricultural Products Utilization

Alternative Fuel Infrastructure

Bond Enhancement

Brownfield “Jobs and Investment”

Business Use Incentives for

Large-scale Development (BUILD)

Community Bank Investment

Demolition

Development

Development Reserve

Developmental Disability Care Provider

Distressed Areas Land Assemblage

Export Finance

Family Development Account

Family Farms Act

Film Production

Historic Preservation

Infrastructure Development

Innovation Campus

Maternity Home

Missouri Low Income Housing

Missouri Quality Jobs

Missouri Works

Neighborhood Assistance

New Enhanced Enterprise Zone

New Enterprise Creation

New Generation Cooperative

New Market

Pregnancy Resource

Rebuilding Communities

Rebuilding Communities and

Neighborhood Preservation Act

Remediation

Residential Treatment Agency

Shelter for Victims of Domestic

Violence

Small Business Incubator

Small Business Investment

Special Needs Adoption

Sporting Contribution

Sporting Event

Transportation Development

Youth Opportunities

Available Tax Credits

Code County Code County Code County Code County Code County

001 Adair 047 Clay 093 Iron 139 Montgomery 185 St Clair

003 Andrew 049 Clinton 095 Jackson 141 Morgan 187 St Francois

005 Atchison 051 Cole 097 Jasper 143 New Madrid 189 St Louis County

007 Audrain 053 Cooper 099 Jefferson 145 Newton 193 Ste Genevieve

009 Barry 055 Crawford 101 Johnson 147 Nodaway 195 Saline

011 Barton 057 Dade 103 Knox 149 Oregon 197 Schuyler

013 Bates 059 Dallas 105 Laclede 151 Osage 199 Scotland

015 Benton 061 Daviess 107 Lafayette 153 Ozark 201 Scott

017 Bollinger 063 Dekalb 109 Lawrence 155 Pemiscot 203 Shannon

019 Boone 065 Dent 111 Lewis 157 Perry 205 Shelby

021 Buchanan 067 Douglas 113 Lincoln 159 Pettis 207 Stoddard

023 Butler 069 Dunklin 115 Linn 161 Phelps 209 Stone

025 Caldwell 071 Franklin 117 Livingston 163 Pike 211 Sullivan

027 Callaway 073 Gasconade 119 Mcdonald 165 Platte 213 Taney

029 Camden 075 Gentry 121 Macon 167 Polk 215 Texas

031 Cape Girardeau 077 Greene 123 Madison 169 Pulaski 217 Vernon

033 Carroll 079 Grundy 125 Maries 171 Putnam 219 Warren

035 Carter 081 Harrison 127 Marion 173 Ralls 221 Washington

037 Cass 083 Henry 129 Mercer 175 Randolph 223 Wayne

039 Cedar 085 Hickory 131 Miller 177 Ray 225 Webster

041 Chariton 087 Holt 133 Mississippi 179 Reynolds 227 Worth

043 Christian 089 Howard 135 Moniteau 181 Ripley 229 Wright

045 Clark 091 Howell 137 Monroe 183 St Charles 510 St Louis City

County Codes

*14000000001*

14000000001