Fillable Printable Sample FBAR Form

Fillable Printable Sample FBAR Form

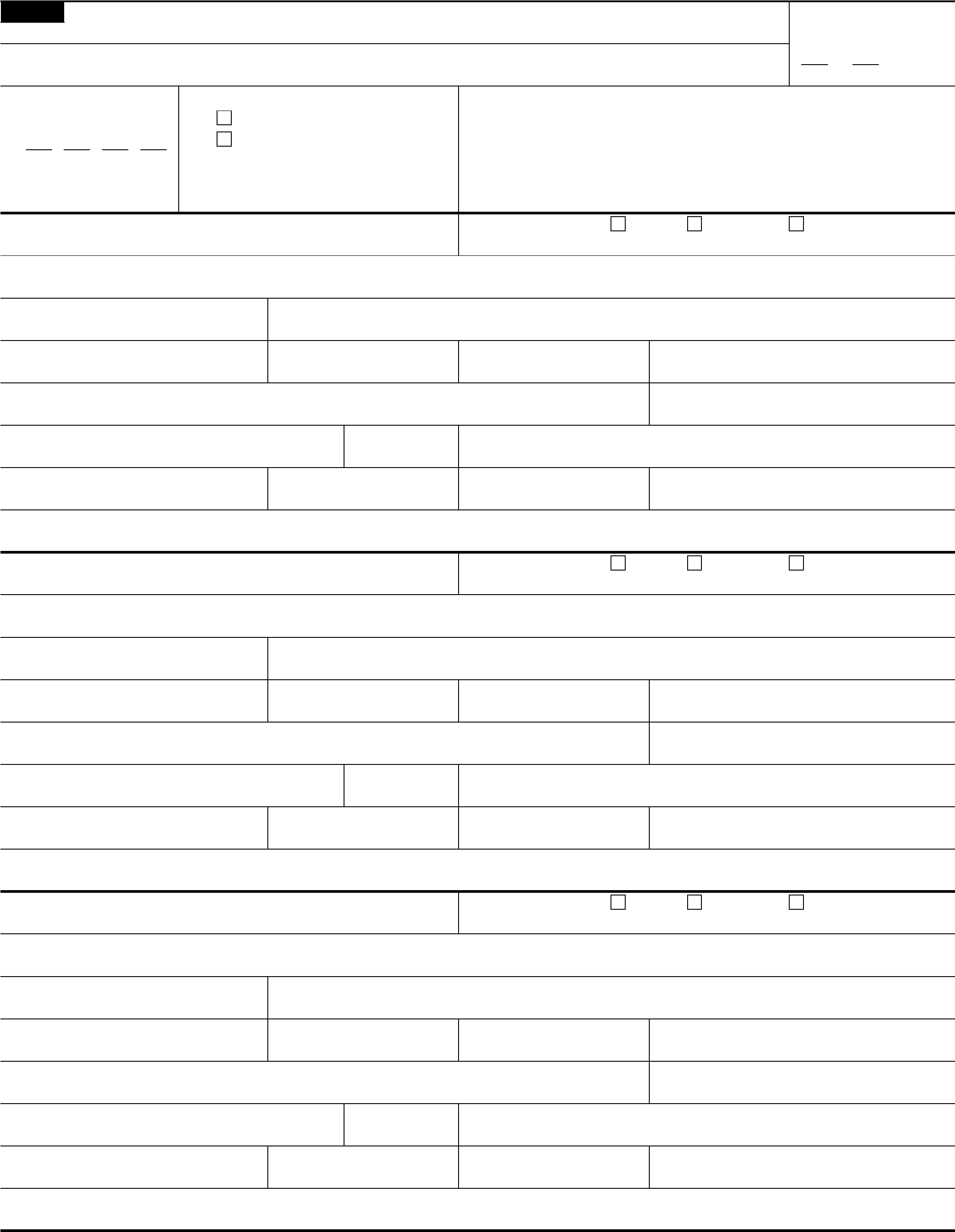

Sample FBAR Form

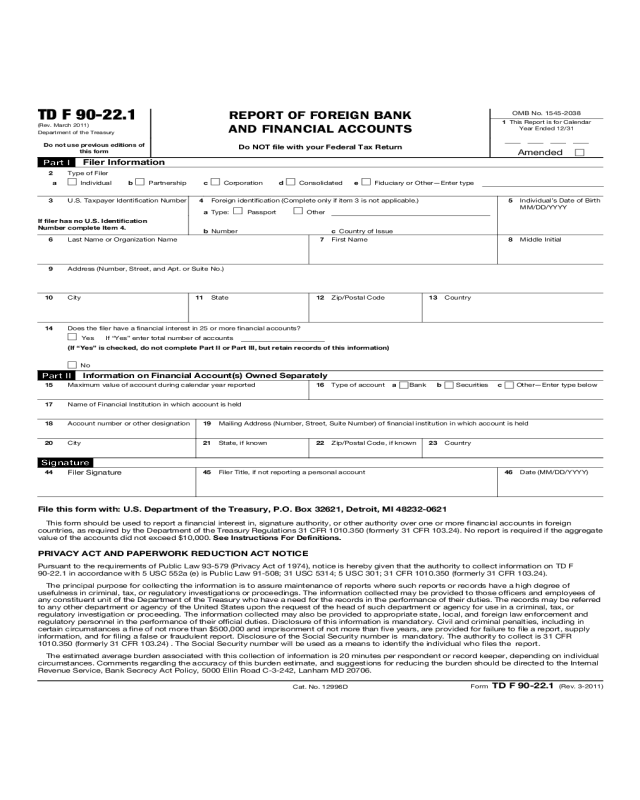

TD F 90-22.1

(Rev. March 2011)

Department of the Treasury

Do not use previous editions of

this form

REPORT OF FOREIGN BANK

AND FINANCIAL ACCOUNTS

Do NOT file with your Federal Tax Return

OMB No. 1545-2038

1 This Report is for Calendar

Year Ended 12/31

Amended

Part I

Filer Information

2 Type of Filer

a

Individual b Partnership c Corporation d Consolidated e Fiduciary or Other—Enter type

3 U.S. Taxpayer Identification Number

If filer has no U.S. Identification

Number complete Item 4.

4 Foreign identification (Complete only if item 3 is not applicable.)

a Type:

Passport Other

b Number c Country of Issue

5

Individual’s Date of Birth

MM/DD/YYYY

6 Last Name or Organization Name 7 First Name 8 Middle Initial

9

Address (Number, Street, and Apt. or Suite No.)

10

City 11 State 12 Zip/Postal Code 13 Country

14 Does the filer have a financial interest in 25 or more financial accounts?

Yes If “Yes” enter total number of accounts

(If “Yes” is checked, do not complete Part II or Part III, but retain records of this information)

No

Part II

Information on Financial Account(s) Owned Separately

15 Maximum value of account during calendar year reported 16 Type of account a Bank b Securities c Other—Enter type below

17

Name of Financial Institution in which account is held

18

Account number or other designation 19 Mailing Address (Number, Street, Suite Number) of financial institution in which account is held

20

City 21 State, if known 22 Zip/Postal Code, if known 23 Country

Signature

44

Filer Signature

45 Filer Title, if not reporting a personal account 46 Date (MM/DD/YYYY)

File this form with: U.S. Department of the Treasury, P.O. Box 32621, Detroit, MI 48232-0621

This form should be used to report a financial interest in, signature authority, or other authority over one or more financial accounts in foreign

countries, as required by the Department of the Treasury Regulations 31 CFR 1010.350 (formerly 31 CFR 103.24). No report is required if the aggregate

value of the accounts did not exceed $10,000. See Instructions For Definitions.

PRIVACY ACT AND PAPERWORK REDUCTION ACT NOTICE

Pursuant to the requirements of Public Law 93-579 (Privacy Act of 1974), notice is hereby given that the authority to collect information on TD F

90-22.1 in accordance with 5 USC 552a (e) is Public Law 91-508; 31 USC 5314; 5 USC 301; 31 CFR 1010.350 (formerly 31 CFR 103.24).

The principal purpose for collecting the information is to assure maintenance of reports where such reports or records have a high degree of

usefulness in criminal, tax, or regulatory investigations or proceedings. The information collected may be provided to those officers and employees of

any constituent unit of the Department of the Treasury who have a need for the records in the performance of their duties. The records may be referred

to any other department or agency of the United States upon the request of the head of such department or agency for use in a criminal, tax, or

regulatory investigation or proceeding. The information collected may also be provided to appropriate state, local, and foreign law enforcement and

regulatory personnel in the performance of their official duties. Disclosure of this information is mandatory. Civil and criminal penalties, including in

certain circumstances a fine of not more than $500,000 and imprisonment of not more than five years, are provided for failure to file a report, supply

information, and for filing a false or fraudulent report. Disclosure of the Social Security number is mandatory. The authority to collect is 31 CFR

1010.350 (formerly 31 CFR 103.24) . The Social Security number will be used as a means to identify the individual who files the report.

The estimated average burden associated with this collection of information is 20 minutes per respondent or record keeper, depending on individual

circumstances. Comments regarding the accuracy of this burden estimate, and suggestions for reducing the burden should be directed to the Internal

Revenue Service, Bank Secrecy Act Policy, 5000 Ellin Road C-3-242, Lanham MD 20706.

Cat. No. 12996D

Form

TD F 90-22.1 (Rev. 3-2011)

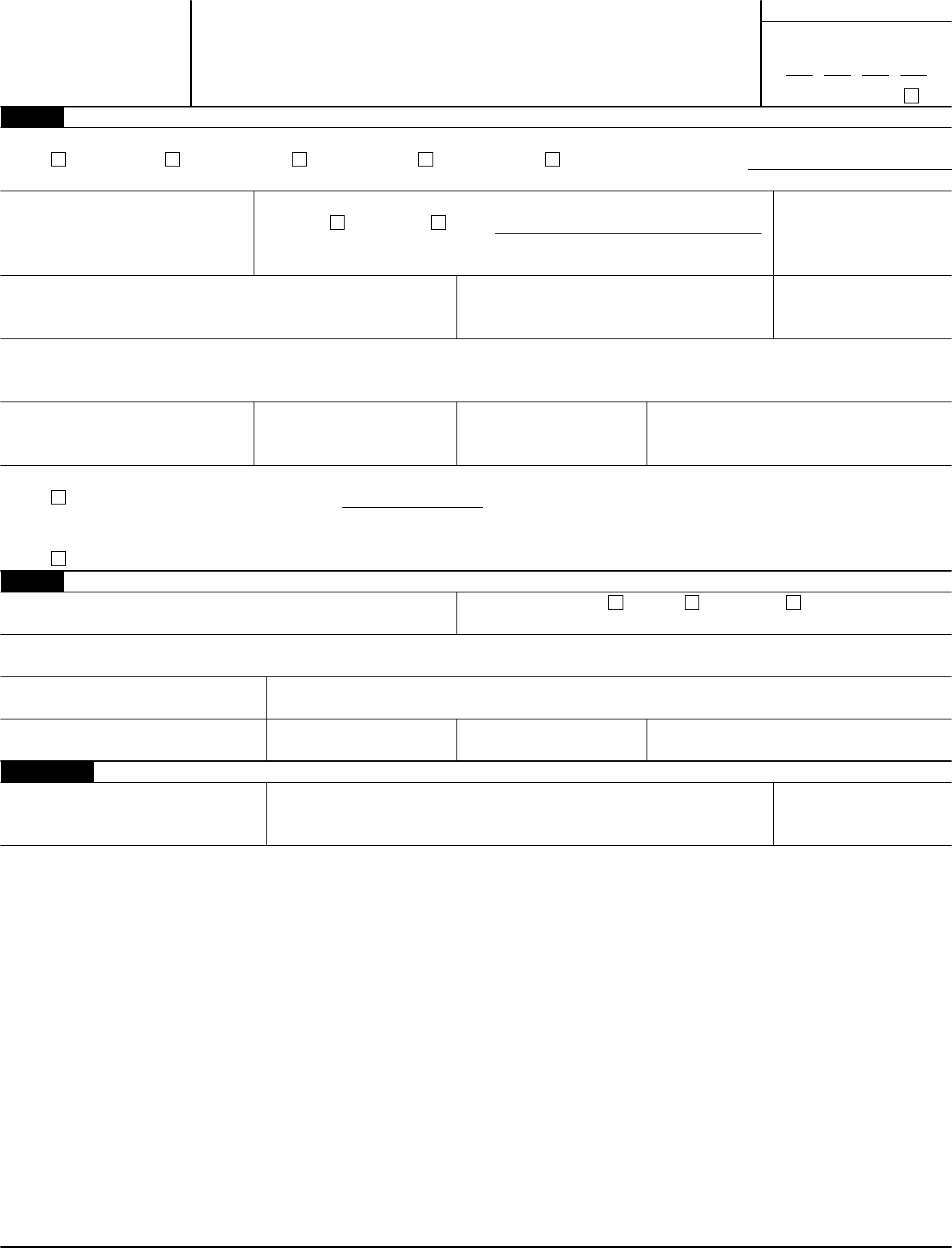

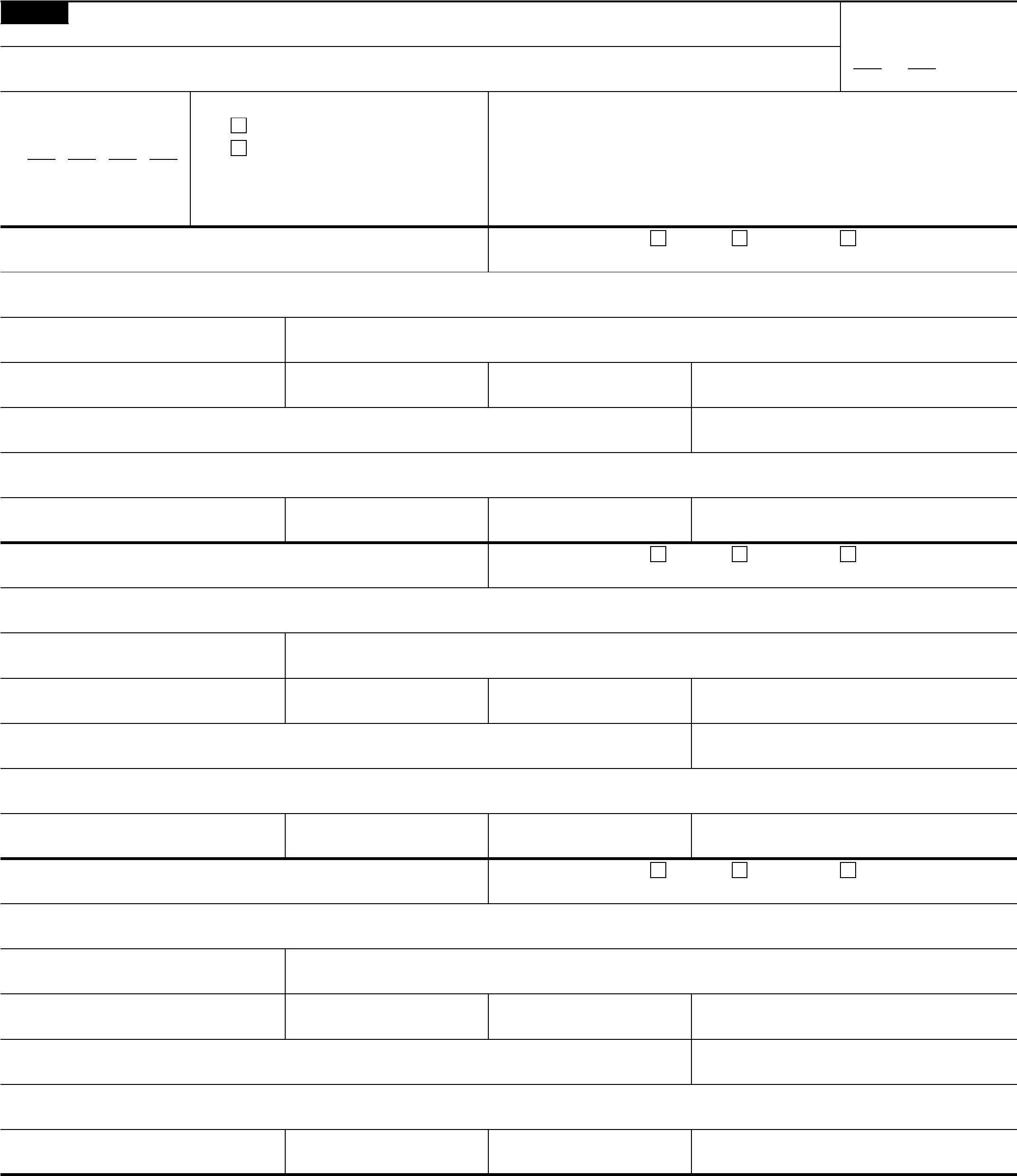

Part II

Continued—Information on Financial Account(s) Owned Separately

Form TD F 90-22.1

Page Number

of

Complete a Separate Block for Each Account Owned Separately

This side can be copied as many times as necessary in order to provide information on all accounts.

1

Filing for calendar

year

3–4

Check appropriate Identification Number

Taxpayer Identification Number

Foreign Identification Number

Enter identification number here:

6

Last Name or Organization Name

15

Maximum value of account during calendar year reported 16 Type of account a Bank b Securities c Other—Enter type below

17

Name of Financial Institution in which account is held

18

Account number or other designation 19 Mailing Address (Number, Street, Suite Number) of financial institution in which account is held

20

City 21 State, if known 22 Zip/Postal Code, if known 23 Country

15

Maximum value of account during calendar year reported 16 Type of account a Bank b Securities c Other—Enter type below

17

Name of Financial Institution in which account is held

18

Account number or other designation 19 Mailing Address (Number, Street, Suite Number) of financial institution in which account is held

20

City 21 State, if known 22 Zip/Postal Code, if known 23 Country

15

Maximum value of account during calendar year reported 16 Type of account a Bank b Securities c Other—Enter type below

17

Name of Financial Institution in which account is held

18

Account number or other designation 19 Mailing Address (Number, Street, Suite Number) of financial institution in which account is held

20

City 21 State, if known 22 Zip/Postal Code, if known 23 Country

15

Maximum value of account during calendar year reported 16 Type of account a Bank b Securities c Other—Enter type below

17

Name of Financial Institution in which account is held

18

Account number or other designation 19 Mailing Address (Number, Street, Suite Number) of financial institution in which account is held

20

City 21 State, if known 22 Zip/Postal Code, if known 23 Country

15

Maximum value of account during calendar year reported 16 Type of account a Bank b Securities c Other—Enter type below

17

Name of Financial Institution in which account is held

18

Account number or other designation 19 Mailing Address (Number, Street, Suite Number) of financial institution in which account is held

20

City 21 State, if known 22 Zip/Postal Code, if known 23 Country

15

Maximum value of account during calendar year reported 16 Type of account a Bank b Securities c Other—Enter type below

17

Name of Financial Institution in which account is held

18

Account number or other designation 19 Mailing Address (Number, Street, Suite Number) of financial institution in which account is held

20

City 21 State, if known 22 Zip/Postal Code, if known 23 Country

Form

TD F 90-22.1 (Rev. 3-2011)

Part III

Information on Financial Account(s) Owned Jointly

Form TD F 90-22.1

Page Number

of

Complete a Separate Block for Each Account Owned Jointly

This side can be copied as many times as necessary in order to provide information on all accounts.

1

Filing for calendar

year

3–4

Check appropriate Identification Number

Taxpayer Identification Number

Foreign Identification Number

Enter identification number here:

6

Last Name or Organization Name

15

Maximum value of account during calendar year reported 16 Type of account a Bank b Securities c Other—Enter type below

17

Name of Financial Institution in which account is held

18

Account number or other designation 19 Mailing Address (Number, Street, Suite Number) of financial institution in which account is held

20

City 21 State, if known 22 Zip/Postal Code, if known 23 Country

24

Number of joint owners for this account

25 Taxpayer Identification Number of principal joint owner, if known. See instructions.

26

Last Name or Organization Name of principal joint owner 27 First Name of principal joint owner, if known 28

Middle initial, if known

29 Address (Number, Street, Suite or Apartment) of principal joint owner, if known

30

City, if known 31 State, if known 32 Zip/Postal Code, if known 33 Country, if known

15

Maximum value of account during calendar year reported 16 Type of account a Bank b Securities c Other—Enter type below

17

Name of Financial Institution in which account is held

18

Account number or other designation 19 Mailing Address (Number, Street, Suite Number) of financial institution in which account is held

20

City 21 State, if known 22 Zip/Postal Code, if known 23 Country

24

Number of joint owners for this account

25 Taxpayer Identification Number of principal joint owner, if known. See instructions.

26

Last Name or Organization Name of principal joint owner 27 First Name of principal joint owner, if known 28

Middle initial, if known

29 Address (Number, Street, Suite or Apartment) of principal joint owner, if known

30

City, if known 31 State, if known 32 Zip/Postal Code, if known 33 Country, if known

15

Maximum value of account during calendar year reported 16 Type of account a Bank b Securities c Other—Enter type below

17

Name of Financial Institution in which account is held

18

Account number or other designation 19 Mailing Address (Number, Street, Suite Number) of financial institution in which account is held

20

City 21 State, if known 22 Zip/Postal Code, if known 23 Country

24

Number of joint owners for this account

25 Taxpayer Identification Number of principal joint owner, if known. See instructions.

26

Last Name or Organization Name of principal joint owner 27 First Name of principal joint owner, if known 28

Middle initial, if known

29 Address (Number, Street, Suite or Apartment) of principal joint owner, if known

30

City, if known 31 State, if known 32 Zip/Postal Code, if known 33 Country, if known

Form

TD F 90-22.1 (Rev. 3-2011)

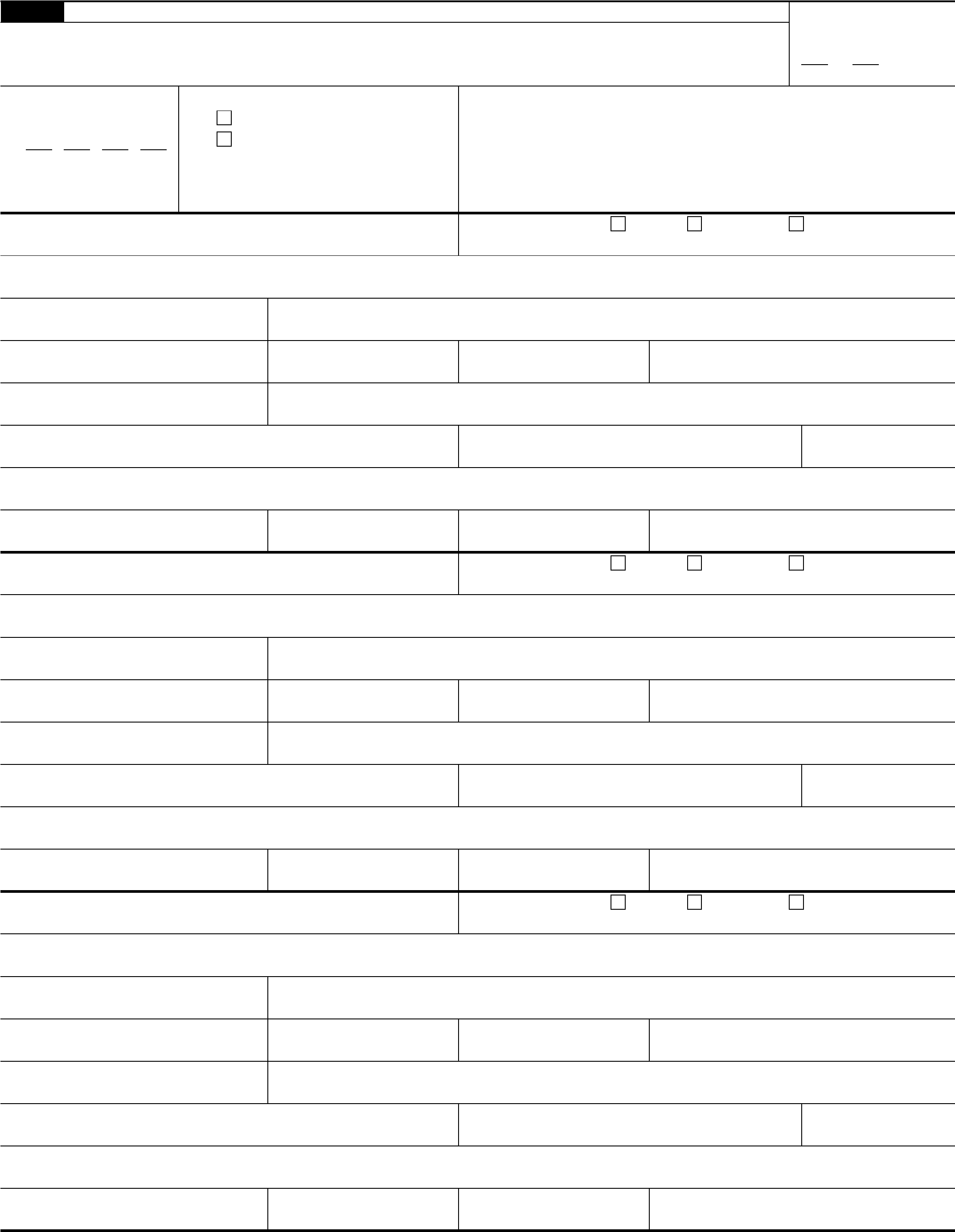

Part IV

Information on Financial Account(s) Where Filer has Signature Authority but No

Financial Interest in the Account(s)

Form TD F 90-22.1

Page Number

of

Complete a Separate Block for Each Account

This side can be copied as many times as necessary in order to provide information on all accounts.

1

Filing for calendar

year

3–4

Check appropriate Identification Number

Taxpayer Identification Number

Foreign Identification Number

Enter identification number here:

6

Last Name or Organization Name

15

Maximum value of account during calendar year reported 16 Type of account a Bank b Securities c Other—Enter type below

17

Name of Financial Institution in which account is held

18

Account number or other designation 19 Mailing Address (Number, Street, Suite Number) of financial institution in which account is held

20

City 21 State, if known 22 Zip/Postal Code, if known 23 Country

34

Last Name or Organization Name of Account Owner

35

Taxpayer Identification Number of Account Owner

36

First Name

37

Middle initial 38 Address (Number, Street, and Apt. or Suite No.)

39

City 40 State 41 Zip/Postal Code 42 Country

43

Filer's Title with this Owner

15

Maximum value of account during calendar year reported 16 Type of account a Bank b Securities c Other—Enter type below

17

Name of Financial Institution in which account is held

18

Account number or other designation 19 Mailing Address (Number, Street, Suite Number) of financial institution in which account is held

20

City 21 State, if known 22 Zip/Postal Code, if known 23 Country

34

Last Name or Organization Name of Account Owner

35

Taxpayer Identification Number of Account Owner

36

First Name

37

Middle initial 38 Address (Number, Street, and Apt. or Suite No.)

39

City 40 State 41 Zip/Postal Code 42 Country

43

Filer's Title with this Owner

15

Maximum value of account during calendar year reported 16 Type of account a Bank b Securities c Other—Enter type below

17

Name of Financial Institution in which account is held

18

Account number or other designation 19 Mailing Address (Number, Street, Suite Number) of financial institution in which account is held

20

City 21 State, if known 22 Zip/Postal Code, if known 23 Country

34

Last Name or Organization Name of Account Owner

35

Taxpayer Identification Number of Account Owner

36

First Name

37

Middle initial 38 Address (Number, Street, and Apt. or Suite No.)

39

City 40 State 41 Zip/Postal Code 42 Country

43

Filer's Title with this Owner

Form

TD F 90-22.1 (Rev. 3-2011)

Part V

Information on Financial Account(s) Where the Filer is Filing a

Consolidated Report

Form TD F 90-22.1

Page Number

of

Complete a Separate Block for Each Account

This side can be copied as many times as necessary in order to provide information on all accounts.

1

Filing for calendar

year

3–4

Check appropriate Identification Number

Taxpayer Identification Number

Foreign Identification Number

Enter identification number here:

6

Last Name or Organization Name

15

Maximum value of account during calendar year reported 16 Type of account a Bank b Securities c Other—Enter type below

17

Name of Financial Institution in which account is held

18

Account number or other designation 19 Mailing Address (Number, Street, Suite Number) of financial institution in which account is held

20

City 21 State, if known 22 Zip/Postal Code, if known 23 Country

34

Corporate Name of Account Owner

35

Taxpayer Identification Number of Account Owner

38 Address (Number, Street, and Apt. or Suite No.)

39

City 40 State 41 Zip/Postal Code 42 Country

15

Maximum value of account during calendar year reported 16 Type of account a Bank b Securities c Other—Enter type below

17

Name of Financial Institution in which account is held

18

Account number or other designation 19 Mailing Address (Number, Street, Suite Number) of financial institution in which account is held

20

City 21 State, if known 22 Zip/Postal Code, if known 23 Country

34

Corporate Name of Account Owner

35

Taxpayer Identification Number of Account Owner

38 Address (Number, Street, and Apt. or Suite No.)

39

City 40 State 41 Zip/Postal Code 42 Country

15

Maximum value of account during calendar year reported 16 Type of account a Bank b Securities c Other—Enter type below

17

Name of Financial Institution in which account is held

18

Account number or other designation 19 Mailing Address (Number, Street, Suite Number) of financial institution in which account is held

20

City 21 State, if known 22 Zip/Postal Code, if known 23 Country

34

Corporate Name of Account Owner

35

Taxpayer Identification Number of Account Owner

38 Address (Number, Street, and Apt. or Suite No.)

39

City 40 State 41 Zip/Postal Code 42 Country

Form

TD F 90-22.1 (Rev. 3-2011)

Form TD F 90-22.1 (Rev. 3-2011)

Page 6

General Instructions

Form TD F 90-22.1, Report of Foreign Bank and Financial Accounts (the

“FBAR”), is used to report a financial interest in or signature authority

over a foreign financial account. The FBAR must be received by the

Department of the Treasury on or before June 30th of the year

immediately following the calendar year being reported. The June 30th

filing date may not be extended.

Who Must File an FBAR. A United States person that has a financial

interest in or signature authority over foreign financial accounts must file

an FBAR if the aggregate value of the foreign financial accounts

exceeds $10,000 at any time during the calendar year. See General

Definitions, to determine who is a United States person.

General Definitions

Financial Account. A financial account includes, but is not limited to, a

securities, brokerage, savings, demand, checking, deposit, time deposit,

or other account maintained with a financial institution (or other person

performing the services of a financial institution). A financial account

also includes a commodity futures or options account, an insurance

policy with a cash value (such as a whole life insurance policy), an

annuity policy with a cash value, and shares in a mutual fund or similar

pooled fund (i.e., a fund that is available to the general public with a

regular net asset value determination and regular redemptions).

Foreign Financial Account. A foreign financial account is a financial

account located outside of the United States. For example, an account

maintained with a branch of a United States bank that is physically

located outside of the United States is a foreign financial account. An

account maintained with a branch of a foreign bank that is physically

located in the United States is not a foreign financial account.

Financial Interest. A United States person has a financial interest in a

foreign financial account for which:

(1) the United States person is the owner of record or holder of legal

title, regardless of whether the account is maintained for the benefit of

the United States person or for the benefit of another person; or

(2) the owner of record or holder of legal title is one of the following:

(a) An agent, nominee, attorney, or a person acting in some other

capacity on behalf of the United States person with respect to the

account;

(b) A corporation in which the United States person owns directly or

indirectly: (i) more than 50 percent of the total value of shares of

stock or (ii) more than 50 percent of the voting power of all shares

of stock;

(c) A partnership in which the United States person owns directly or

indirectly: (i) an interest in more than 50 percent of the partnership's

profits (e.g., distributive share of partnership income taking into

account any special allocation agreement) or (ii) an interest in more

than 50 percent of the partnership capital;

(d) A trust of which the United States person: (i) is the trust grantor

and (ii) has an ownership interest in the trust for United States

federal tax purposes. See 26 U.S.C. sections 671-679 to determine

if a grantor has an ownership interest in a trust;

(e) A trust in which the United States person has a greater than 50

percent present beneficial interest in the assets or income of the

trust for the calendar year; or

(f) Any other entity in which the United States person owns directly

or indirectly more than 50 percent of the voting power, total value of

equity interest or assets, or interest in profits.

Person. A person means an individual and legal entities including, but

not limited to, a limited liability company, corporation, partnership, trust,

and estate.

Signature Authority. Signature authority is the authority of an individual

(alone or in conjunction with another individual) to control the disposition

of assets held in a foreign financial account by direct communication

(whether in writing or otherwise) to the bank or other financial institution

that maintains the financial account. See Exceptions, Signature

Authority.

United States. For FBAR purposes, the United States includes the

States, the District of Columbia, all United States territories and

possessions (e.g., American Samoa, the Commonwealth of the Northern

Mariana Islands, the Commonwealth of Puerto Rico, Guam, and the

United States Virgin Islands), and the Indian lands as defined in the

Indian Gaming Regulatory Act. References to the laws of the United

States include the laws of the United States federal government and the

laws of all places listed in this definition.

United States Person. United States person means United States

citizens; United States residents; entities, including but not limited to,

corporations, partnerships, or limited liability companies created or

organized in the United States or under the laws of the United States;

and trusts or estates formed under the laws of the United States.

Note. The federal tax treatment of an entity does not determine whether

the entity has an FBAR filing requirement. For example, an entity that is

disregarded for purposes of Title 26 of the United States Code must file

an FBAR, if otherwise required to do so. Similarly, a trust for which the

trust income, deductions, or credits are taken into account by another

person for purposes of Title 26 of the United States Code must file an

FBAR, if otherwise required to do so.

United States Resident. A United States resident is an alien residing in

the United States. To determine if the filer is a resident of the United

States apply the residency tests in 26 U.S.C. section 7701(b). When

applying the residency tests, use the definition of United States in these

instructions.

Exceptions

Certain Accounts Jointly Owned by Spouses. The spouse of an

individual who files an FBAR is not required to file a separate FBAR if

the following conditions are met: (1) all the financial accounts that the

non-filing spouse is required to report are jointly owned with the filing

spouse; (2) the filing spouse reports the jointly owned accounts on a

timely filed FBAR; and (3) both spouses sign the FBAR in Item 44. See

Explanations for Specific Items, Part III, Items 25-33. Otherwise, both

spouses are required to file separate FBARs, and each spouse must

report the entire value of the jointly owned accounts.

Consolidated FBAR. If a United States person that is an entity is

named in a consolidated FBAR filed by a greater than 50 percent owner,

such entity is not required to file a separate FBAR. See Explanations for

Specific Items, Part V.

Correspondent/Nostro Account. Correspondent or nostro accounts

(which are maintained by banks and used solely for bank-to-bank

settlements) are not required to be reported.

Governmental Entity. A foreign financial account of any governmental

entity of the United States (as defined above) is not required to be

reported by any person. For purposes of this form, governmental entity

includes a college or university that is an agency of, an instrumentality

of, owned by, or operated by a governmental entity. For purposes of this

form, governmental entity also includes an employee retirement or

welfare benefit plan of a governmental entity.

International Financial Institution. A foreign financial account of any

international financial institution (if the United States government is a

member) is not required to be reported by any person.

IRA Owners and Beneficiaries. An owner or beneficiary of an IRA is

not required to report a foreign financial account held in the IRA.

Participants in and Beneficiaries of Tax-Qualified Retirement Plans.

A participant in or beneficiary of a retirement plan described in Internal

Revenue Code section 401(a), 403(a), or 403(b) is not required to report

a foreign financial account held by or on behalf of the retirement plan.

Signature Authority. Individuals who have signature authority over, but

no financial interest in, a foreign financial account are not required to

report the account in the following situations:

(1) An officer or employee of a bank that is examined by the Office of

the Comptroller of the Currency, the Board of Governors of the Federal

Reserve System, the Federal Deposit Insurance Corporation, the Office

of Thrift Supervision, or the National Credit Union Administration is not

required to report signature authority over a foreign financial account

owned or maintained by the bank.

(2) An officer or employee of a financial institution that is registered

with and examined by the Securities and Exchange Commission or

Commodity Futures Trading Commission is not required to report

signature authority over a foreign financial account owned or maintained

by the financial institution.

Form TD F 90-22.1 (Rev. 3-2011)

Page 7

(3) An officer or employee of an Authorized Service Provider is not

required to report signature authority over a foreign financial account

that is owned or maintained by an investment company that is

registered with the Securities and Exchange Commission. Authorized

Service Provider means an entity that is registered with and examined

by the Securities and Exchange Commission and provides services to

an investment company registered under the Investment Company Act

of 1940.

(4) An officer or employee of an entity that has a class of equity

securities listed (or American depository receipts listed) on any United

States national securities exchange is not required to report signature

authority over a foreign financial account of such entity.

(5) An officer or employee of a United States subsidiary is not required

to report signature authority over a foreign financial account of the

subsidiary if its United States parent has a class of equity securities

listed on any United States national securities exchange and the

subsidiary is included in a consolidated FBAR report of the United

States parent.

(6) An officer or employee of an entity that has a class of equity

securities registered (or American depository receipts in respect of

equity securities registered) under section 12(g) of the Securities

Exchange Act is not required to report signature authority over a foreign

financial account of such entity.

Trust Beneficiaries. A trust beneficiary with a financial interest

described in section (2)(e) of the financial interest definition is not

required to report the trust's foreign financial accounts on an FBAR if

the trust, trustee of the trust, or agent of the trust: (1) is a United States

person and (2) files an FBAR disclosing the trust's foreign financial

accounts.

United States Military Banking Facility. A financial account maintained

with a financial institution located on a United States military installation

is not required to be reported, even if that military installation is outside

of the United States.

Filing Information

When and Where to File. The FBAR is an annual report and must be

received by the Department of the Treasury on or before June 30th of

the year following the calendar year being reported. Do Not file with

federal income tax return.

File by mailing to:

Department of the Treasury

Post Office Box 32621

Detroit, MI 48232-0621

If an express delivery service is used, file by mailing to:

IRS Enterprise Computing Center

ATTN: CTR Operations Mailroom, 4th Floor

985 Michigan Avenue

Detroit, MI 48226

The FBAR may be hand delivered to any local office of the Internal

Revenue Service for forwarding to the Department of the Treasury,

Detroit, MI. The FBAR may also be delivered to the Internal Revenue

Service's tax attaches located in United States embassies and

consulates for forwarding to the Department of the Treasury, Detroit, MI.

The FBAR is not considered filed until it is received by the Department

of the Treasury in Detroit, MI.

No Extension of Time to File. There is no extension of time available

for filing an FBAR. Extensions of time to file federal tax returns do NOT

extend the time for filing an FBAR. If a delinquent FBAR is filed, attach a

statement explaining the reason for the late filing.

Amending a Previously Filed FBAR. To amend a filed FBAR, check the

“Amended” box in the upper right hand corner of the first page of the

FBAR, make the needed additions or corrections, attach a statement

explaining the additions or corrections, and staple a copy of the original

FBAR to the amendment. An amendment should not be made until at

least 90 calendar days after the original FBAR is filed. Follow the

instructions in “When and Where to File” to file an amendment.

Record Keeping Requirements. Persons required to file an FBAR must

retain records that contain the name in which each account is

maintained, the number or other designation of the account, the name

and address of the foreign financial institution that maintains the

account, the type of account, and the maximum account value of each

account during the reporting period. The records must be retained for a

period of 5 years from June 30th of the year following the calendar year

reported and must be available for inspection as provided by law.

Retaining a copy of the filed FBAR can help to satisfy the record

keeping requirements.

An officer or employee who files an FBAR to report signature authority

over an employer's foreign financial account is not required to

personally retain records regarding these accounts.

Questions. For questions regarding the FBAR, contact the Detroit

Computing Center Hotline at 1-800-800-2877, option 2.

Explanations for Specific Items

Part I — Filer Information

Item 1. The FBAR is an annual report. Enter the calendar year being

reported. If amending a previously filed FBAR, check the “Amended”

box.

Item 2. Check the box that describes the filer. Check only one box.

Individuals reporting only signature authority, check box “a”. If filing a

consolidated FBAR, check box “d”. To determine if a consolidated

FBAR can be filed, see Part V. If the type of filer is not listed in boxes “a”

through “c”, check box “e”, and enter the type of filer. Persons that

should check box “e” include, but are not limited to, trusts, estates,

limited liability companies, and tax-exempt entities (even if the entity is

organized as a corporation). A disregarded entity must check box “e”,

and enter the type of entity followed by “(D.E.)”. For example, a limited

liability company that is disregarded for United States federal tax

purposes would enter “limited liability company (D.E.)”.

Item 3. Provide the filer's United States taxpayer identification number.

Generally, this is the filer's United States social security number (SSN),

United States individual taxpayer identification number (ITIN), or

employer identification number (EIN). Throughout the FBAR, numbers

should be entered with no spaces, dashes, or other punctuation. If the

filer does NOT have a United States taxpayer identification number,

complete Item 4.

Item 4. Complete Item 4 only if the filer does NOT have a United States

taxpayer identification number. Item 4 requires the filer to provide

information from an official foreign government document to verify the

filer's nationality or residence. Enter the document number followed by

the country of issuance, check the appropriate type of document, and if

“other” is checked, provide the type of document.

Item 5. If the filer is an individual, enter the filer's date of birth, using the

month, day, and year convention.

Items 9, 10, 11, 12, and 13. Enter the filer's address. An individual

residing in the United States must enter the street address of the

individual's United States residence, not a post office box. An individual

residing outside the United States must enter the individual's United

States mailing address. If the individual does not have a United States

mailing address, the individual must enter a foreign residence address.

An entity must enter its United States mailing address. If the entity does

not have a United States mailing address, the entity must enter its

foreign mailing address.

Item 14. If the filer has a financial interest in 25 or more foreign financial

accounts, check “Yes” and enter the number of accounts. Do not

complete Part II or Part III of the FBAR. If filing a consolidated FBAR,

only complete Part V, Items 34-42, for each United States entity

included in the consolidated FBAR.

Note. If the filer has signature authority over 25 or more foreign financial

accounts, only complete Part IV, Items 34-43, for each person for which

the filer has signature authority, and check “No” in Part I, Item 14.

Filers must comply with applicable recording keeping requirements.

See Record Keeping Requirements.

Part II — Information on Financial Account(s) Owned

Separately

Enter information in the applicable parts of the form only. Number the

pages used, and mail only those pages. If there is not enough space to

provide all account information, copy and complete additional pages of

the required Part as necessary. Do not use any attachments unless

otherwise specified in the instructions.

Form TD F 90-22.1 (Rev. 3-2011)

Page 8

Item 15. Determining Maximum Account Value.

Step 1. Determine the maximum value of each account (in the currency

of that account) during the calendar year being reported. The maximum

value of an account is a reasonable approximation of the greatest value

of currency or nonmonetary assets in the account during the calendar

year. Periodic account statements may be relied on to determine the

maximum value of the account, provided that the statements fairly

reflect the maximum account value during the calendar year. For Item

15, if the filer had a financial interest in more than one account, each

account must be valued separately.

Step 2. In the case of non-United States currency, convert the

maximum account value for each account into United States dollars.

Convert foreign currency by using the Treasury's Financial Management

Service rate (this rate may be found at www.fms.treas.gov) from the last

day of the calendar year. If no Treasury Financial Management Service

rate is available, use another verifiable exchange rate and provide the

source of that rate. In valuing currency of a country that uses multiple

exchange rates, use the rate that would apply if the currency in the

account were converted into United States dollars on the last day of the

calendar year.

If the aggregate of the maximum account values exceeds $10,000, an

FBAR must be filed. An FBAR is not required to be filed if the person did

not have $10,000 of aggregate value in foreign financial accounts at any

time during the calendar year.

For United States persons with a financial interest in or signature

authority over fewer than 25 accounts that are unable to determine if the

aggregate maximum account values of the accounts exceeded $10,000

at any time during the calendar year, complete Part II, III, IV, or V, as

appropriate, for each of these accounts and enter “value unknown” in

Item 15.

Item 16. Indicate the type of account. Check only one box. If “Other” is

selected, describe the account.

Item 17. Provide the name of the financial institution with which the

account is held.

Item 18. Provide the account number that the financial institution uses

to designate the account.

Items 19-23. Provide the complete mailing address of the financial

institution where the account is located. If the foreign address does not

include a state (e.g., province) or postal code, leave the box(es) blank.

Part III — Information on Financial Account(s) Owned

Jointly

Enter information in the applicable parts of the form only. Number the

pages used, and mail only those pages. If there is not enough space to

provide all account information, copy and complete additional pages of

the required Part as necessary. Do not use any attachments unless

otherwise specified in the instructions.

For Items 15-23, see Part II. Each joint owner must report the entire

value of the account as determined under Item 15.

Item 24. Enter the number of joint owners for the account. If the exact

number is not known, provide an estimate. Do not count the filer when

determining the number of joint owners.

Items 25-33. Use the identifying information of the principal joint owner

(excluding the filer) to complete Items 25-33. Leave blank items for

which no information is available. If the filer's spouse has an interest in a

jointly owned account, the filer's spouse is the principal joint owner.

Enter “(spouse)” on line 26 after the last name of the joint spousal

owner. See Exceptions, Certain Accounts Jointly Owned by Spouses, to

determine if the filer's spouse is required to independently report the

jointly owned accounts.

Part IV — Information on Financial Account(s) Where

Filer has Signature Authority but No Financial Interest

in the Account(s)

Enter information in the applicable parts of the form only. Number the

pages used, and mail only those pages. If there is not enough space to

provide all account information, copy and complete additional pages of

the required Part as necessary. Do not use any attachments unless

otherwise specified in the instructions.

25 or More Foreign Financial Accounts. Filers with signature authority

over 25 or more foreign financial accounts must complete only Items

34-43 for each person on whose behalf the filer has signature authority.

Modified Reporting for United States Persons Residing and

Employed Outside of the United States. A United States person who

(1) resides outside of the United States, (2) is an officer or employee of

an employer who is physically located outside of the United States, and

(3) has signature authority over a foreign financial account that is owned

or maintained by the individual's employer should only complete Part I

and Part IV, Items 34-43 of the FBAR. Part IV, Items 34-43 should only

be completed one time with information about the individual's employer.

For Items 15-23, see Part II.

Items 34-42. Provide the name, address, and identifying number of the

owner of the foreign financial account for which the individual has

signature authority over but no financial interest in the account. If there

is more than one owner of the account for which the individual has

signature authority, provide the information in Items 34-42 for the

principal joint owner (excluding the filer). If account information is

completed for more than one account of the same owner, identify the

owner only once and write “Same Owner” in Item 34 for the succeeding

accounts with the same owner.

Item 43. Enter filer's title for the position that provides signature

authority (e.g., treasurer).

Part V — Information on Financial Account(s) Where

Corporate Filer Is Filing a Consolidated Report

Enter information in the applicable parts of the form only. Number the

pages used, and mail only those pages. If there is not enough space to

provide all account information, copy and complete additional pages of

the required Part as necessary. Do not use any attachments unless

otherwise specified in the instructions.

Who Can File a Consolidated FBAR. An entity that is a United States

person that owns directly or indirectly a greater than 50 percent interest

in another entity that is required to file an FBAR is permitted to file a

consolidated FBAR on behalf of itself and such other entity. Check box

“d” in Part I, Item 2 and complete Part V. If filing a consolidated FBAR

and reporting 25 or more foreign financial accounts, complete only

Items 34-42 for each entity included in the consolidated FBAR.

For Items 15-23, see Part II.

Items 34-42. Provide the name, United States taxpayer identification

number, and address of the owner of the foreign financial account as

shown on the books of the financial institution. If account information is

completed for more than one account of the same owner, identify the

owner only once and write “Same Owner” in Item 34 for the succeeding

accounts of the same owner.

Signatures

Items 44-46. The FBAR must be signed by the filer named in Part I. If

the FBAR is being filed on behalf of a partnership, corporation, limited

liability company, trust, estate, or other entity, it must be signed by an

authorized individual. Enter the authorized individual's title in Item 45.

An individual must leave “Filer's Title” blank, unless the individual is

filing an FBAR due to the individual's signature authority. If an individual

is filing because the individual has signature authority over a foreign

financial account, the individual should enter the title upon which his or

her authority is based in Item 45.

A spouse included as a joint owner, who does not file a separate

FBAR in accordance with the instructions in Part III, must also sign the

FBAR (in Item 44) for the jointly owned accounts. See the instructions

for Part III.

Penalties

A person who is required to file an FBAR and fails to properly file may

be subject to a civil penalty not to exceed $10,000. If there is reasonable

cause for the failure and the balance in the account is properly reported,

no penalty will be imposed. A person who willfully fails to report an

account or account identifying information may be subject to a civil

monetary penalty equal to the greater of $100,000 or 50 percent of the

balance in the account at the time of the violation. See 31 U.S.C. section

5321(a)(5). Willful violations may also be subject to criminal penalties

under 31 U.S.C. section 5322(a), 31 U.S.C. section 5322(b), or 18 U.S.C.

section 1001.