Fillable Printable Special Needs Trust Form - Georgia

Fillable Printable Special Needs Trust Form - Georgia

Special Needs Trust Form - Georgia

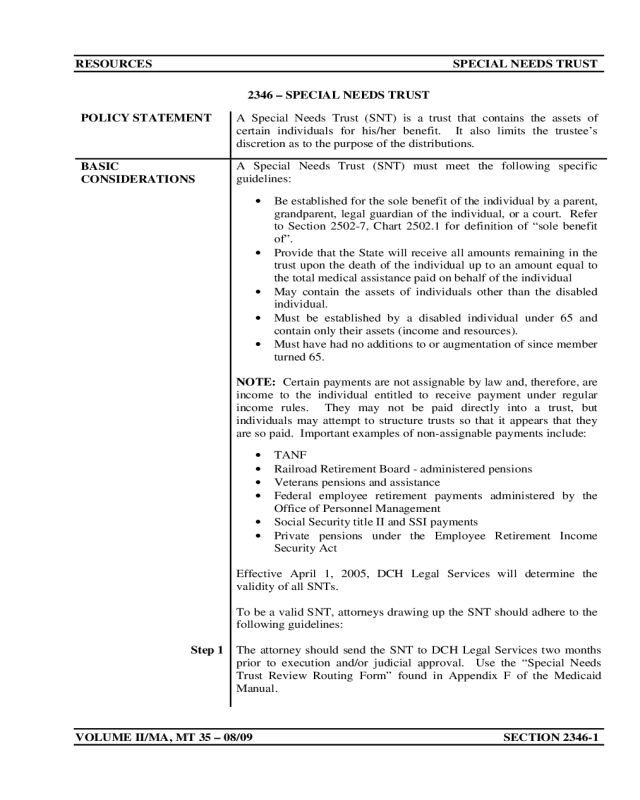

RESOURCES SPECIAL NEEDS TRUST

VOLUME II/MA, MT 35 – 08/09 SECTION 2346-1

2346 – SPECIAL NEEDS TRUST

POLICY STATEMENT

A Special Needs Trust (SNT) is a trust that contains the assets of

certain individuals for his/her benefit. It also limits the trustee’s

discretion as to the purpose of the distributions.

BASIC

CONSIDERATIONS

Step 1

A Special Needs Trust (SNT) must meet the following specific

guidelines:

• Be established for the sole benefit of the individual by a parent,

grandparent, legal guardian of the individual, or a court. Refer

to Section 2502-7, Chart 2502.1 for definition of “sole benefit

of”.

• Provide that the State will receive all amounts remaining in the

trust upon the death of the individual up to an amount equal to

the total medical assistance paid on behalf of the individual

• May contain the assets of individuals other than the disabled

individual.

• Must be established by a disabled individual under 65 and

contain only their assets (income and resources).

• Must have had no additions to or augmentation of since member

turned 65.

NOTE: Certain payments are not assignable by law and, therefore, are

income to the individual entitled to receive payment under regular

income rules. They may not be paid directly into a trust, but

individuals may attempt to structure trusts so that it appears that they

are so paid. Important examples of non-assignable payments include:

• TANF

• Railroad Retirement Board - administered pensions

• Veterans pensions and assistance

• Federal employee retirement payments administered by the

Office of Personnel Management

• Social Security title II and SSI payments

• Private pensions under the Employee Retirement Income

Security Act

Effective April 1, 2005, DCH Legal Services will determine the

validity of all SNTs.

To be a valid SNT, attorneys drawing up the SNT should adhere to the

following guidelines:

The attorney should send the SNT to DCH Legal Services two months

prior to execution and/or judicial approval. Use the “Special Needs

Trust Review Routing Form” found in Appendix F of the Medicaid

Manual.

RESOURCES SPECIAL NEEDS TRUST

VOLUME II/MA, MT 35 – 08/09 SECTION 2346-2

BASIC

CONSIDERATIONS

(cont.)

Step 2

Step 3

Step 4

Step 5

Step 6

Step 7

Step 8

Step 9

Step 10

Step 11

Step 12

Step 13

If the trust is to be funded with the proceeds of a settlement, a certified

copy of the settlement and the court order must be submitted with the

trust.

Notice of the time and place of any hearing regarding a Court approval

of the settlement and SNT should be served upon the DCH at least 15

business days before the hearing.

The DCH will not recognize the validity of any SNT until all liens in

favor of the DCH shall be first satisfied in full.

All SNTs are subject to a yearly audit by DCH or its agents. DCH may

also audit prior years of the trust.

No payment can be made from the trust except for the benefit of the

beneficiary and may not exceed the amount that can be determined to

reasonably meet the special needs of the beneficiary. Refer to Section

2502-7, Chart 2502.1 for definition of “sole benefit of”.

The SNT shall specifically identify, in an attached schedule, the initial

source of the trust, all assets of the trust, all assets purchased with trust

funds and all wages or payment for caregiver or other services. The

trustee must update the schedule yearly. Schedules must be submitted

to DFCS and to DCH Legal Services.

The SNT shall specifically state the age of the trust beneficiary and

affirm that the trust beneficiary is disabled within the definition of 42

U.S. C. Section 1382c(a)(3), and whether the trust beneficiary is

competent or incompetent at the time the trust is established.

The SNT shall specifically state that its purpose is to permit the use of

SNT assets to supplement, and not to supplant, impair or diminish

benefits or assistance of any Federal, State or other governmental entity

for which the beneficiary may otherwise be eligible or for which the

beneficiary is competent at the time the trust is established.

The DCH shall be given a minimum of 30 days notice if there is a

change in the trus tee.

The DCH must be given notice within 5 days of the death of the

beneficiary.

Beneficiaries are required to comply with SSI income rules. See 20

CFR 416.

Failure to comply with policy will result in the SNT being counted as

an asset or transfer of resources.

RESOURCES SPECIAL NEEDS TRUST

VOLUME II/MA, MT 35 – 08/09 SECTION 2346-3

PROCEDURES

Step 1

Step 2

Step 3

Step 4

Step 5

Follow the procedures below for processing applications/reviews

containing SNTs:

For applications pending on or after April 1, 2005, send a copy of the

SNT to DCH Legal Services Section, along with proof of disability,

prior to approval of the case. Use the routing form in Appendix F,

entitled “Special Needs Trust Review Routing Form”. Some attorneys

may submit SNTs to DCH prior to the application at DFCS. Obtain

copies of the submission to DCH and its determination. If not, submit

SNT upon receipt during application process. Submit the same

documents that are required above.

For active cases where a previously unknown SNT is discovered, send

a copy of the SNT to DCH Legal Services Section, along with proof of

disability, prior to completion of the annual review or special review.

Submit two months prior to review if possible. Use the routing form in

Appendix F, entitled “Special Needs Trust Review Routing Form”.

Do not finalize the application or review until DCH Legal has either

approved or denied the validity of the trust.

If the trust is irrevocable and cannot be used by the A/R for his/her

support and maintenance, it is not a resource. If the A/R does not have

the legal authority to revoke the trust or direct the use of the trust assets,

the trust prin cipal is not the A/R’s resource.

Treat disbursements from the trust as follows:

• Cash paid directly to the A/R is unearned income.

• Food, clothing or shelter received as a result of a disbursement from

the trust is income in the form of in-kind support and maintenance.

Use the presumed maximum value (PMV) rule. See Section 2430

,

Living Arrangement and In-Kind Support and Maintenance for ABD

Medicaid.”

• Disbursements by the trustee to a third party that result in the A/R

receiving items that are NOT food, clothing or shelter are not

considered income (example personal sitters, handicapped van, etc.).

• If the trust principal is a countable resource to the A/R,

disbursements from the trust principal received by the A/R are not

income, but a conversion of a resource. However, the trust earnings

(interest) are counted as unearned income.

If you find there have been additions to or augmentations of the trust

since the member reached age 65, then count as an asset or transfer of

asset.

RESOURCES SPECIAL NEEDS TRUST

VOLUME II/MA, MT 35 – 08/09 SECTION 2346-4

PROCEDURES

(cont.)

Step 6

Should you discover during an annual or special review that the

requirements of the trust are not being followed, consult your Medicaid

Program Specialist for instructions.