Fillable Printable Affidavit of Non-Ohio Residency/Domicile for Taxable Year 2014

Fillable Printable Affidavit of Non-Ohio Residency/Domicile for Taxable Year 2014

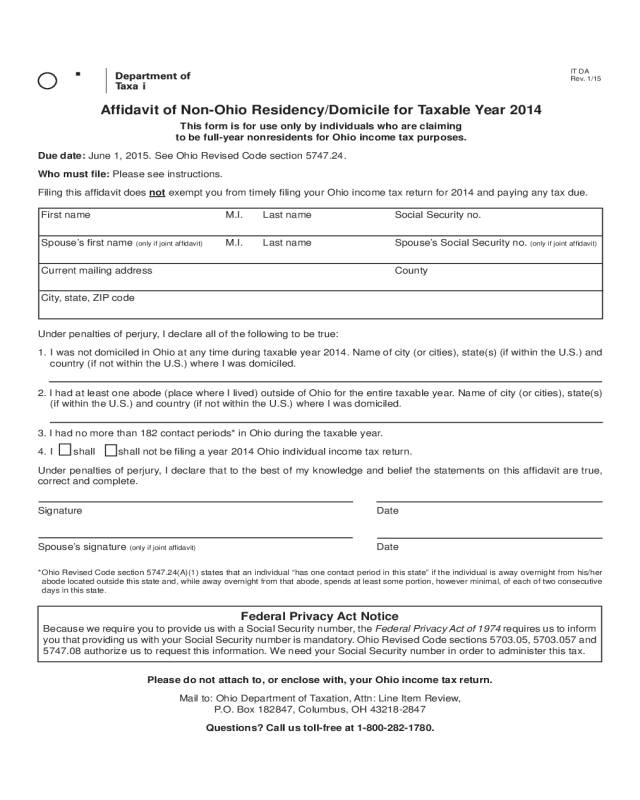

Affidavit of Non-Ohio Residency/Domicile for Taxable Year 2014

IT DA

Rev. 1/15

Affidavit of Non-Ohio Residency/Domicile for Taxable Year 2014

This form is for use only by individuals who are claiming

to be full-year nonresidents for Ohio income tax purposes.

Due date: June 1, 2015. See Ohio Revised Code section 5747.24.

Who must file: Please see instructions.

Filing this affi davit does not exempt you from timely filing your Ohio income tax return for 2014 and paying any tax due.

First name M.I. Last name Social Security no.

Spouse’s fi rst name

(only if joint affidavit) M.I. Last name Spouse’s Social Security no. (only if joint affidavit)

Current mailing address County

City, state, ZIP code

Under penalties of perjury, I declare all of the following to be true:

1. I was not domiciled in Ohio at any time during taxable year 2014. Name of city (or cities), state(s) (if within the U.S.) and

country (if not within the U.S.) where I was domiciled.

2. I had at least one abode (place where I lived) outside of Ohio for the entire taxable year. Name of city (or cities), state(s)

(if within the U.S.) and country (if not within the U.S.) where I was domiciled.

3. I had no more than 182 contact periods* in Ohio during the taxable year.

4. I

shall shall not be filing a year 2014 Ohio individual income tax return.

Under penalties of perjury, I declare that to the best of my knowledge and belief the statements on this affidavit are true,

correct and complete.

Signature Date

Spouse’s signature (only if joint affidavit) Date

*Ohio Revised Code section 5747.24(A)(1) states that an individual “has one contact period in this state” if the individual is away overnight from his/her

abode located outside this state and, while away overnight from that abode, spends at least some portion, however minimal, of each of two consecutive

days in this state.

Federal Privacy Act Notice

Because we require you to provide us with a Social Security number , the Federal Privacy Act of 1974 requires us to inform

you that providing us with your Social Security number is mandatory. Ohio Revised Code sections 5703.05, 5703.057 and

5747.08 authorize us to request this information. We need your Social Security number in order to administer this tax.

Please do not attach to, or enclose with, your Ohio income tax return.

Mail to: Ohio Department of Taxation, Attn: Line Item Review,

P.O. Box 182847, Columbus, OH 43218-2847

Questions? Call us toll-free at 1-800-282-1780.

IT DA Instructions

Who Should File This Affidavit?

You must file this yearly affidavit if you meet either of the

following criteria:

During the previous taxable year (2013) you filed an Ohio

income tax return as a resident or part-year resident, and

for the current taxable year (2014) you are claiming to be

a nonresident/nondomiciliary.

For the current taxable year (2014) you have no intent to

file an Ohio income tax return and you have (i) an abode

in Ohio, (ii) a contact period in Ohio and/or (iii) nexus with

Ohio to the extent that the tax commissioner would have

cause to question your nonfiling.

If you meet either of the criteria set forth above, but you do

not file this affidavit by June 1, 2015, under Ohio law you are

presumed to be a full-year domiciliary.

Why Should I File This Affidavit?

R.C.section 5747.24 requires that, in order to preserve the

presumption of full-year non-Ohio residency, the taxpayer

must file this affidavit by the 15th day of the fourth month

following the last day of the taxable year. However, R.C.

section 5703.35 allows the tax commissioner to extend for

45 days the due date for any report. As such, you must file

this tax return by June 1, 2015. The tax commissioner has

no authority to extend beyond June 1, 2015 the due date for

filing the year 2014 affidavit.

What Is the Due Date for Filing This Affidavit?

The postmark date must be no later than June 1, 2015.

Do I Need To File This Affidavit if I Have Not Earned or

Received Any Income in Ohio?

Even if you have no income that you earned or received in

Ohio, you must timely file this affidavit by June 1, 2015 if

you want to preserve the presumption of full-year non-Ohio

residency.

If I Timely File Ohio Form ITDA, Do I Also Have To File

Ohio Form IT 10, Information Notice of No Tax Due?

By filing Ohio form IT 10, you are indicating that you have no

Ohio income tax liability. If you have not earned or received

any income in Ohio, you may want to consider filing both this

affidavit and Ohio form IT 10. Please do not mail the affidavit

and notice together since there is a dif ferent address for the

affidavit and for the notice.

Where Do I Mail This Affidavit?

Please mail this affidavit to the Ohio Department of Taxation,

Attn: Correspondence and Line Item Review, P.O. Box

182847, Columbus, OH 43218-2847. The postmark date

must be no later than June 1, 2015. Please do not attach

this affidavit to, or enclose with, your Ohio individual income

tax return.

Whom Do I Contact if I Have Additional Questions

About This Affidavit?

For faster service you can visit our Web site at tax.ohio.gov,

click on “Contact” and electronically send us your question(s)

or you can call 1-800-282-1780.

What Is the “Bright Line” Test Under Ohio Revised

Code Section 5747.24?

This portion of Ohio law provides for a “bright line” test under

which an individual is presumed to be a full-year nonresident

if all of the following circumstances are present:

The individual has at least one abode outside Ohio for the

entire year (the law does not defi ne “abode”),

The individual has no more than 182 contact periods in

Ohio, and

The individual timely submits to the Ohio Department of

Taxation this affidavit, and the affidavit is not false.

What Is a “Contact Period” in Ohio?

An individual has one contact period in this state if the

individual is away overnight from the individual’s abode

located outside the state and while away overnight from

that abode spends at least some portion, however minimal,

of each of two consecutive days in this state. Note that the

individual does not have to spend the night in Ohio.

For example: An individual who claims to be domiciled in

Florida has an abode in Florida for the entire year . On Jan. 2

of the taxable year the individual flies from Florida to Toledo.

Later on Jan. 2 the individual drives to Michigan and spends

the night in Michigan. On Jan. 3 the individual drives from

Michigan back to Ohio. Late in the day on Jan. 3 the individual

flies from Toledo back to the individual’s abode in Florida.

The individual has one contact period in Ohio because the

individual spent some portion of two consecutive days (Jan. 2

and Jan. 3) in Ohio and was away overnight (from sometime

on Jan. 2 until sometime on Jan. 3) from the individual’s

abode in Florida.