Fillable Printable Foreclosure Prevention Counseling

Fillable Printable Foreclosure Prevention Counseling

Foreclosure Prevention Counseling

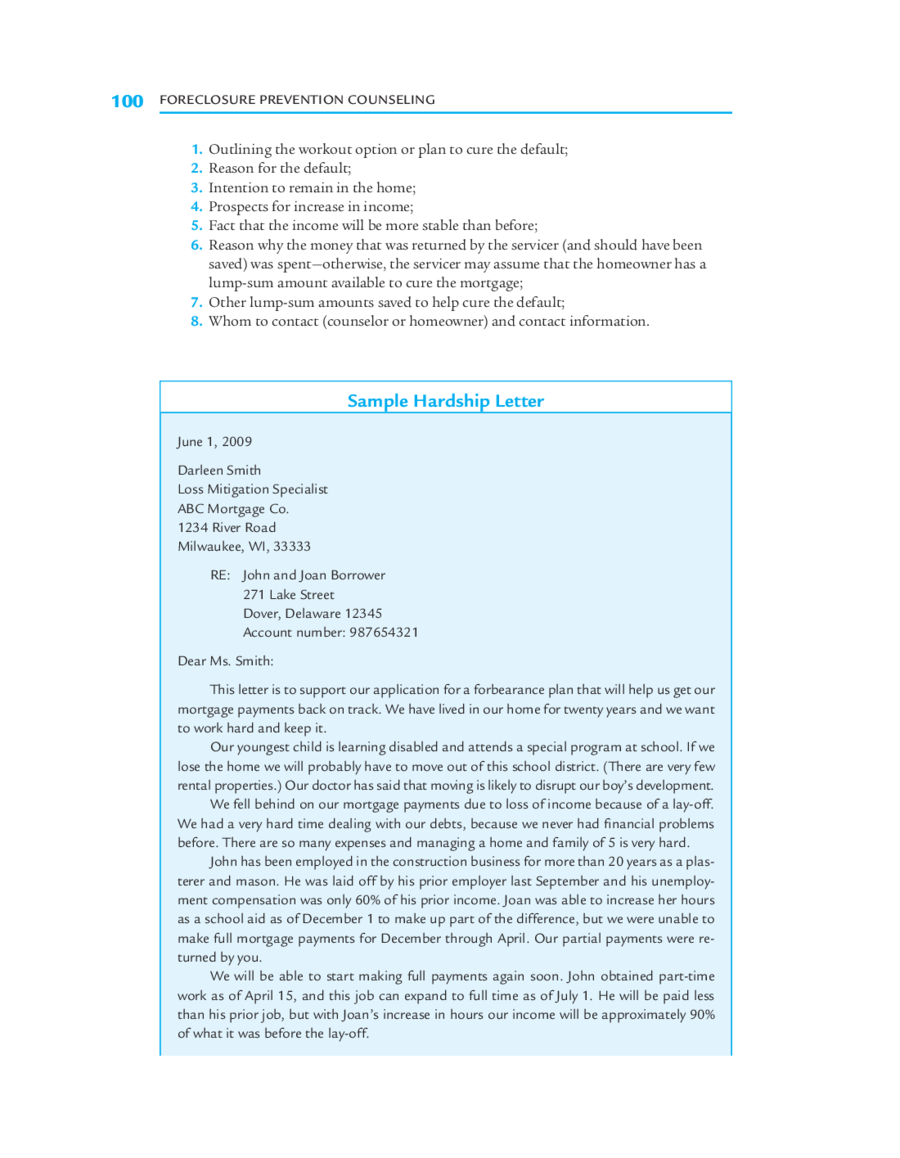

Sample Hardship Letter

June 1, 2009

Darleen Smith

Loss Mitigation Specialist

ABC Mortgage Co.

1234 River Road

Milwaukee, WI, 33333

RE:John and Joan Borrower

271 Lake Street

Dover, Delaware 12345

Account number: 987654321

Dear Ms. Smith:

This letter is to support our application for a forbearance plan that will help us get our

mortgage payments back on track. We have lived in our home for twenty years and we want

to work hard and keep it.

Our youngest child is learning disabled and attends a special program at school. If we

lose the home we will probably have to move out of this school district. (There are very few

rental properties.) Our doctor has said that moving is likely to disrupt our boy’s development.

We fell behind on our mortgage payments due to loss of income because of a lay-off.

We had a very hard time dealing with our debts, because we never had financial problems

before. There are so many expenses and managing a home and family of 5 is very hard.

John has been employed in the construction business for more than 20 years as a plas-

terer and mason. He was laid off by his prior employer last September and his unemploy-

ment compensation was only 60% of his prior income. Joan was able to increase her hours

as a school aid as of December 1 to make up part of the difference, but we were unable to

make full mortgage payments for December through April. Our partial payments were re-

turned by you.

We will be able to start making full payments again soon. John obtained part-time

work as of April 15, and this job can expand to full time as of July 1. He will be paid less

than his prior job, but with Joan’s increase in hours our income will be approximately 90%

of what it was before the lay-off.

FORECLOSURE PREVENTION COUNSELING

100

1.Outlining the workout option or plan to cure the default;

2.Reason for the default;

3.Intention to remain in the home;

4.Prospects for increase in income;

5.Fact that the income will be more stable than before;

6.Reason why the money that was returned by the servicer (and should have been

sa

ved) was spent—otherwise, the servicer may assume that the homeowner has a

lump-sum amount available to cure the mortgage;

7.Other lump-sum amounts saved to help cure the default;

8.Whom to contact (counselor or homeowner) and contact information.

FPC05.qxp:083-108_FPC05 5/11/09 3:13 PM Page 100

TIPS FOR COUNSELORS ESTABLISHING A WORKOUT PLAN

1. Time is of the essence in working out a foreclosure. Make sure you know what the

timeline is for the foreclosure process in your state and where in the timeline the borrower

you are assisting is.

2. Keep track of deadlines. Negotiating a workout may take months. Servicers may neglect

to tell the f

oreclosure attorney that they are talking to you. Do not let deadlines pass without

an agreement in writing as to an extension.

3. Confirm with the servicer any extension of deadlines in writing. Do not rely on oral

assurances that ev

erything is taken care of.

4. Protect the client’s data.As part of the workout process, you may need to quickly pro-

vide inf

ormation to servicers. It is important to remember that traditional e-mail can be inter-

cepted by unscrupulous scammers or spyware or read by any system through which it passes.

This includes attachments of sensitive information, such as tax returns, pay stubs, etc. While

this possibility may seem remote, you should protect your client (and yourself) by using

secure networks and e-mailing techniques. One method to accomplish this is protecting at-

tachments with passwords and providing the “key” within an encrypted e-mail (the recipi-

ent, of course, must know how to “unencrypt.”) Facsimiles are secure, as is first-class mail.

Ch. 5

■

GETTING A DEAL: THE MECHANICS OF ARRANGING A WORKOUT

101

One other good thing is that John’s new job is indoor work, which will be steady, and

his new employer is a construction company that has been in business for thirty-five years.

Unlike some of John’s past jobs, he is not going to be laid off for the winter. John is a good

worker and we know he will stick.

We had saved about $2,700 toward the mortgage as of March 1. This is the money

you had returned to us. We had hoped to use this money as part of a plan to get caught up

on our payments. However, we discovered last month that our 1999 Nissan Maxima could

no longer be fixed. Since John’s new job is in Wilmington, he needs a car and we have spent

about $2,000 of the money we had saved as a down payment for a used (2003) Ford truck.

We still have the other $700 and we expect to put aside $800 (the amount of our regular

payment) each month starting August 1.

Our financial information is enclosed with this letter. If we can have a forbearance

plan that involves payments of no more than $800 per month, we know we can make it. You

will see that we have minimized all our expenses and it is most important to us to keep this

home. Please put yourself in our position and try to help. We thank you very much for any

effort you can make.

Please contact our foreclosure prevention counselor, Jane Dean, at 312-555-1213, to

discuss this further.

Sincerely,

John Borrower

Joan Borrower

FPC05.qxp:083-108_FPC05 5/11/09 3:13 PM Page 101